Deep Dive: Salesforce ($CRM) - Is the "SaaSpocalypse" An Opportunity?

The market is having a full-blown existential crisis over the future of software. But when you look under the hood at Salesforce's cash turbine, the math tells a totally different story.

New to The Atomic Moat? This analysis of Salesforce ($CRM) is a prime example of how we dissect high-quality compounders. If you want these deep dives sent to your inbox, join 1,500+ other investors below.

Folks, the market loves to panic first and do the math later. Right now, Wall Street is having a full-blown existential crisis over enterprise software.

The reigning narrative? AI is going to eat the SaaS application layer alive. The fear is that autonomous AI agents will simply “DIY” complex workflows. Why pay for expensive per-seat licenses when a smart chatbot can do the job for free?

Right now, the market is throwing the baby out with the bathwater. We’re watching highly durable, cash-minting businesses get priced like melting ice cubes simply because they happen to sell software.

But indiscriminate panic is exactly where the best opportunities hide. And that led me straight to the granddaddy of the industry: Salesforce.

I wanted to look under the hood and strip away the noise. Is the Salesforce fortress actually cracking under the weight of AI disruption, or is Wall Street just hallucinating a structural decline for a company that is still printing billions in cash?

Let’s dig in and find out.

If You’re In a Rush

Let’s break this down to the studs before we get into the weeds:

What they do: Salesforce sells enterprise “systems of record” for customer work—sales, service, data, and automation. They make their money mostly as subscription & support revenue.

Why it’s hated: The market is currently flirting with the terrifying idea that AI agents will simply “DIY” the application layer. Wall Street thinks SaaS is going to get commoditized, which means multiples compress even if the underlying fundamentals actually improve.

What fixes it: Proving that “agentic” demand is additive—not cannibalizing. We need to see that bookings, backlog, and cash conversion stay rock-solid while the AI stack shifts.

Atomic Position: No position, but on my watchlist.

The Setup

The stock is sitting at $189.72 per share today (Feb 14th 2026). That is a long, painful drop from the $358 top it hit back in December 2024.

Stop & Think: When a stock gets cut in half but the business keeps churning out cash, you have to ask yourself: is the business broken, or is Mr. Market irrational?

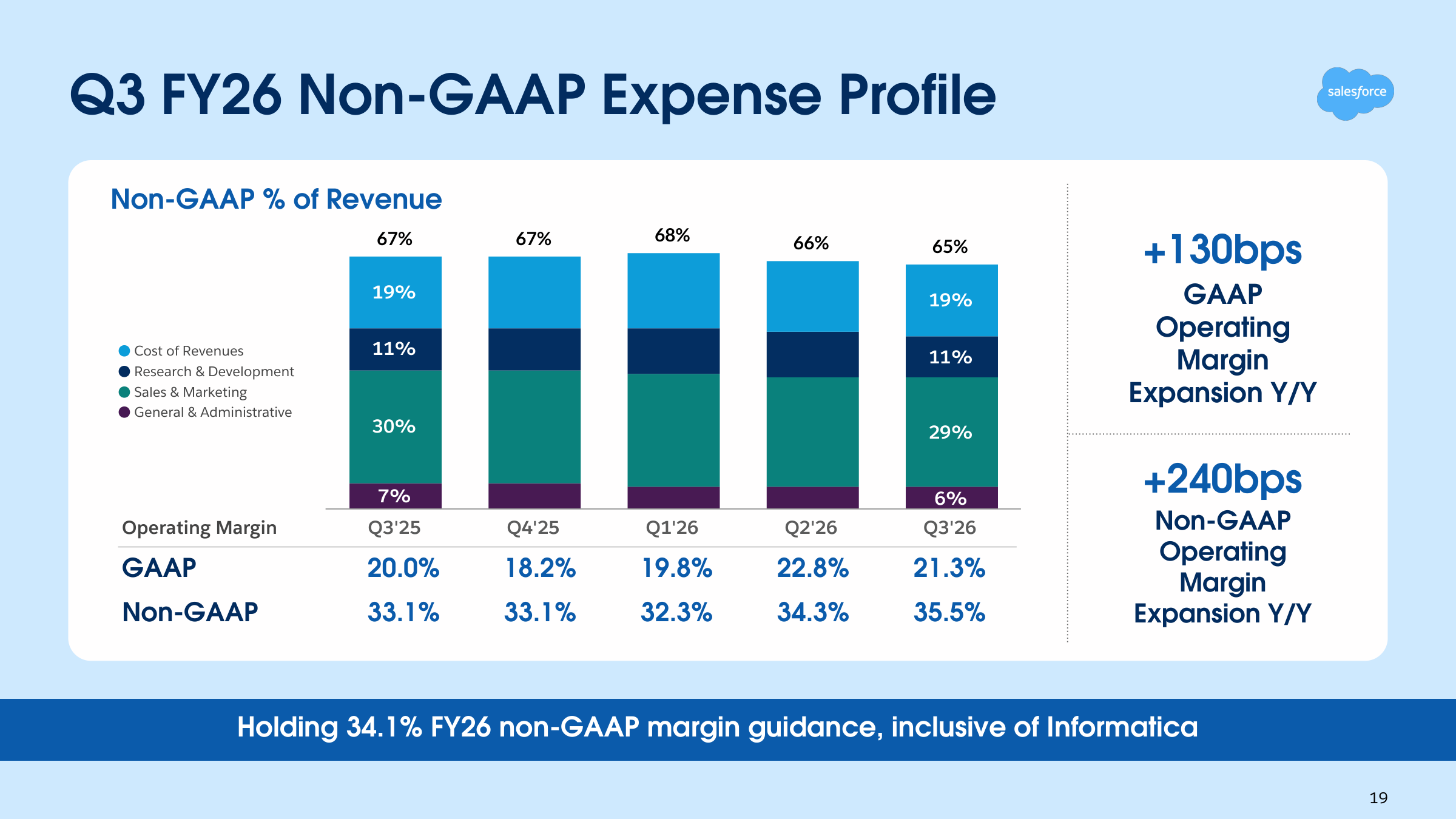

On the inside, the scoreboard looks a heck of a lot sturdier than the price action suggests. In Q3 FY26, Salesforce reported $10.259B revenue and a 21.3% GAAP operating margin, alongside a very healthy 35.5% non-GAAP operating margin.

On the outside, however, sentiment is being governed by a very specific, very loud fear. The fear is that generative AI is “injurious to the SaaS-based application layer,” and that enterprise customers will simply DIY their way around legacy vendors.

Variant Perception

Let’s look at the three sides of this narrative coin:

Market: “AI agents kill app-layer value capture; incumbents become expensive UI wrappers.”

Bull: “Agents make systems-of-record more valuable; Salesforce monetizes trust + data + workflow + governance.” (By the way, this is the company’s “agentic enterprise” framing).

Bear: “AI attach is theater; growth stays single digits; buybacks become the only growth story left.”

This deep dive is about whether Salesforce can convert the AI narrative from a radioactive leak (driving multiple compression) into a controlled reactor (driving forward demand + monetization + cash).

Atomic Take: Salesforce looks operationally healthier than its stock chart implies. But I’ll be blunt: it’s still trading under the massive “SaaS gets disintermediated” cloud until forward indicators force Wall Street to re-rate it.

Falsifier: Q4 FY26 cRPO growth misses the company’s ~15% Y/Y guide (Q4 FY26, %, company guide) — if they miss that, it would validate the bear thesis that “demand isn’t inflecting.”

How the Business Actually Makes Money

Salesforce is, at its core, a massive subscription engine with a services sidecar bolted onto it. Subscription and support revenue is $9.726B, versus professional services and other bringing in just $0.533B.

Mechanically, their compounding loop is beautifully straightforward. I love businesses like this:

Land a workflow that becomes the default answer to “how the company does customer work.”

Expand across products (and across departments) until the customer has hardwired their processes and permissions deep into your platform. It’s like pouring roots into concrete.

Renew, because ripping out the system-of-record is the enterprise equivalent of open-heart surgery performed by a committee. Nobody wants to do it.

Quick note: Salesforce uses a fiscal year, so ‘Q3 FY26’ is the quarter ended Oct 31, 2025. Think of it like the Premier League: the 2025–26 season includes matches played in both 2025 and 2026. Same idea here, where ‘FY26’ includes quarters played in 2025. Companies do this because a fiscal year that lines up with their business cycle makes budgeting and performance comparisons cleaner. And for Salesforce, it keeps the big end-of-year sales/renewal season from being split awkwardly across two reporting years.

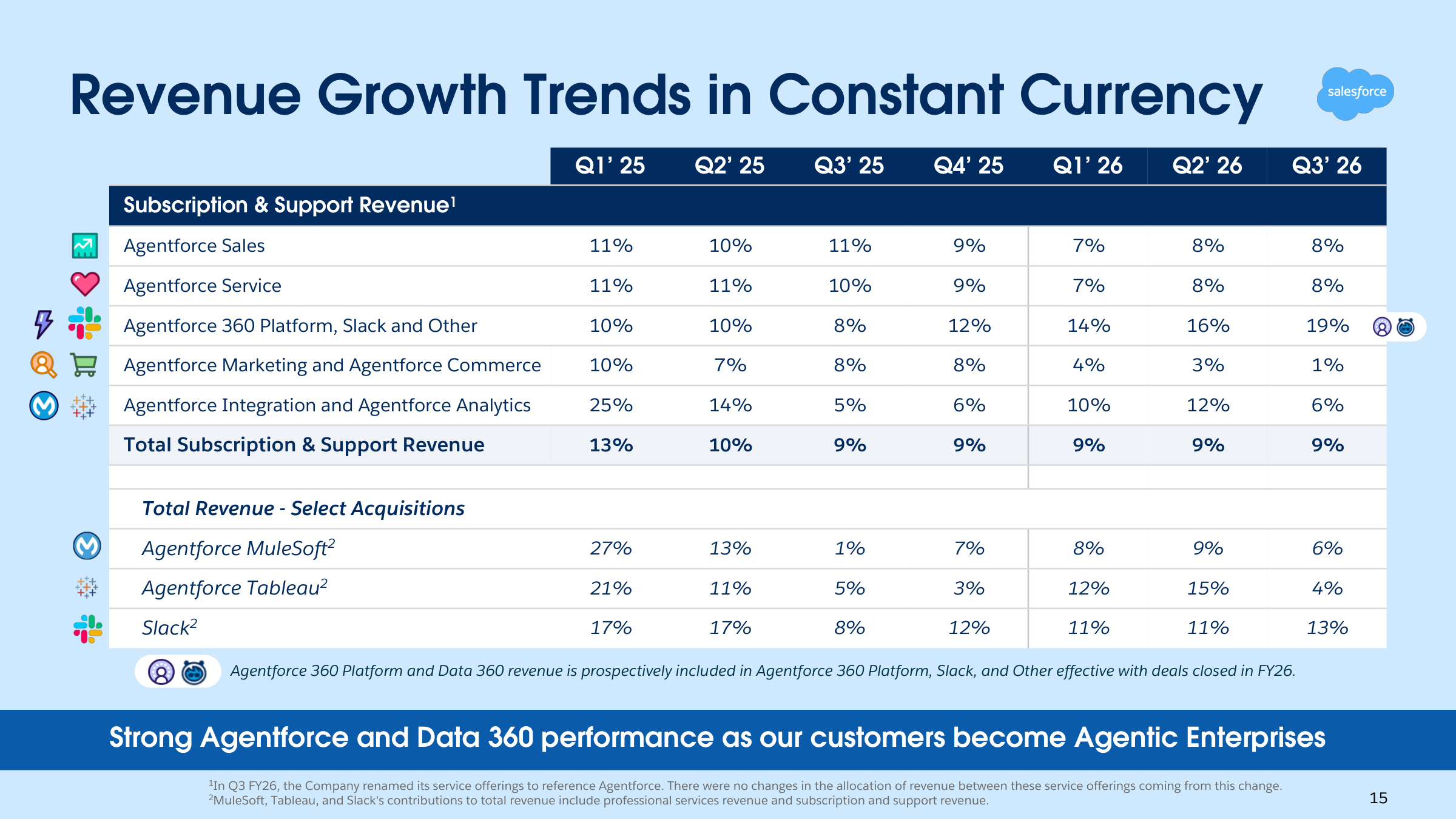

In Q3 FY26, Salesforce’s revenue disaggregation is presented under the new “Agentforce” naming umbrella (and the company explicitly states the rename did not change revenue allocation).

That’s incredibly useful.

It tells you this is, at least partly, packaging and positioning. And make no mistake, packaging matters deeply when the market is busy repricing narratives.

Let’s look at the major subscription buckets (Q3 FY26, USD, GAAP):

Agentforce Service: $2.495B

Agentforce Sales: $2.297B

Agentforce 360 Platform, Slack and Other: $2.180B

Agentforce Integration and Agentforce Analytics: $1.393B

Agentforce Marketing and Agentforce Commerce: $1.361B

Now, let’s talk about the “AI option.” Management isn’t pitching “hey look, we added a chatbot.” They’re pitching “we are the control plane for deployed agents inside the enterprise.”

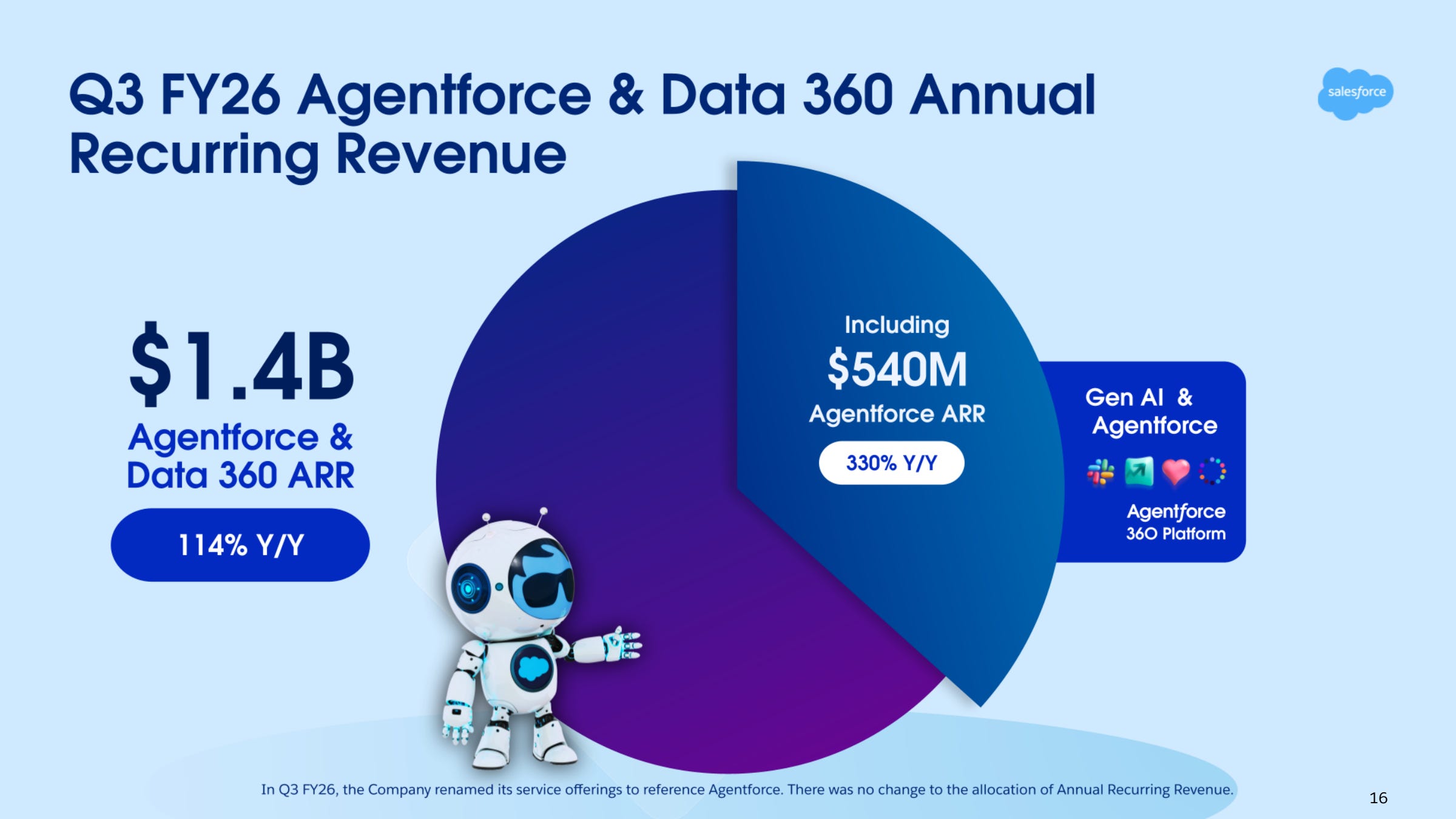

The measurable proof points they’ve chosen to emphasize are adoption and ARR-style monetization, including Agentforce and Data 360 ARR reaching nearly $1.4B, and Agentforce ARR surpassing half a billion.

Atomic Take: Salesforce doesn’t need to “invent a new category”; it just needs to remain the system-of-record and become the system-of-agents that runs on top of it.

Falsifier: Agentforce paid deals stop growing quarter-over-quarter (paid deals were >9,500 and up 50% QoQ in Q3 FY26, company KPI) — if that stalls, it would imply the AI attach motion isn’t sticking.

What Went Wrong

First, growth slowed. Multiples got severely compressed. Then, the market found a convenient story that rationalizes paying less for the stock forever.

What it shows is a shifting growth regime: subscription & support constant-currency growth steps down and sits at 9% through Q3 FY26.

That’s the basic setup for a re-rate. Once growth moves from being a “teen compounder” to “high-single-digit durability,” the market stops paying for endless possibility and starts demanding cold, hard proof.

Stop & Think: Watch the hands, not the mouth. If enterprise customers truly thought AI was going to kill Salesforce, why are they signing thousands of new paid deals for Agentforce?

Then comes the “Narrative Scare”: the belief that AI agents make the application layer less valuable, and that customers will DIY around vendors. Again, this isn’t speculative panic from the cheap seats. It is literally presented on the call as the investor expectation.

So what does Marc Benioff (and management) think of it?

Their stance is basically this: investors are pricing a world where AI agents DIY the application layer and shrink the value of SaaS, but management says customer reality is moving the other way.

They describe a “mismatch” between what the market expects (DIY replacement) and what they’re seeing in the field: companies tried building their own models/toolkits, then ran into the messy reality that enterprise deployment is the hard part.

In Benioff’s framing, the value isn’t in tinkering. It’s in shipping deployed “customer agents” that live inside real workflows.

That matters because it implies a likely path forward; not “magic growth next quarter,” but a migration from experimentation to production:

Customers move from pilots to deployed agents in live workflows.

Deployment forces governance: permissions, auditability, workflow integration, and real data context.

The system-of-record becomes the control plane (because that’s where the workflows + context already live).

Monetization shifts toward attach and expansion (agents/data/products layered onto the core), not just seat growth.

Atomic Take: Salesforce’s bet is that AI doesn’t delete the system-of-record, but it increases its importance, because enterprises will pay for agents that are governed, contextual, and reliably executable.

Rebound Catalysts

Wall Street doesn’t need Salesforce to be a flawless diamond right now. It just needs the boogeyman story (the “SaaS gets disintermediated by AI” campfire tale) to stop being believable.

I’ve always said, you don’t need a perfect company to make money; you just need a mispriced one that proves the loudest skeptics wrong.

Here are the testable catalysts we need to watch. The beauty is, these are tied to the exact KPIs Salesforce is already disclosing. No guesswork required:

1. Backlog credibility stays strong

Think of the backlog like a farmer’s silo. If the silo is full of grain, you don’t worry about starving next winter.

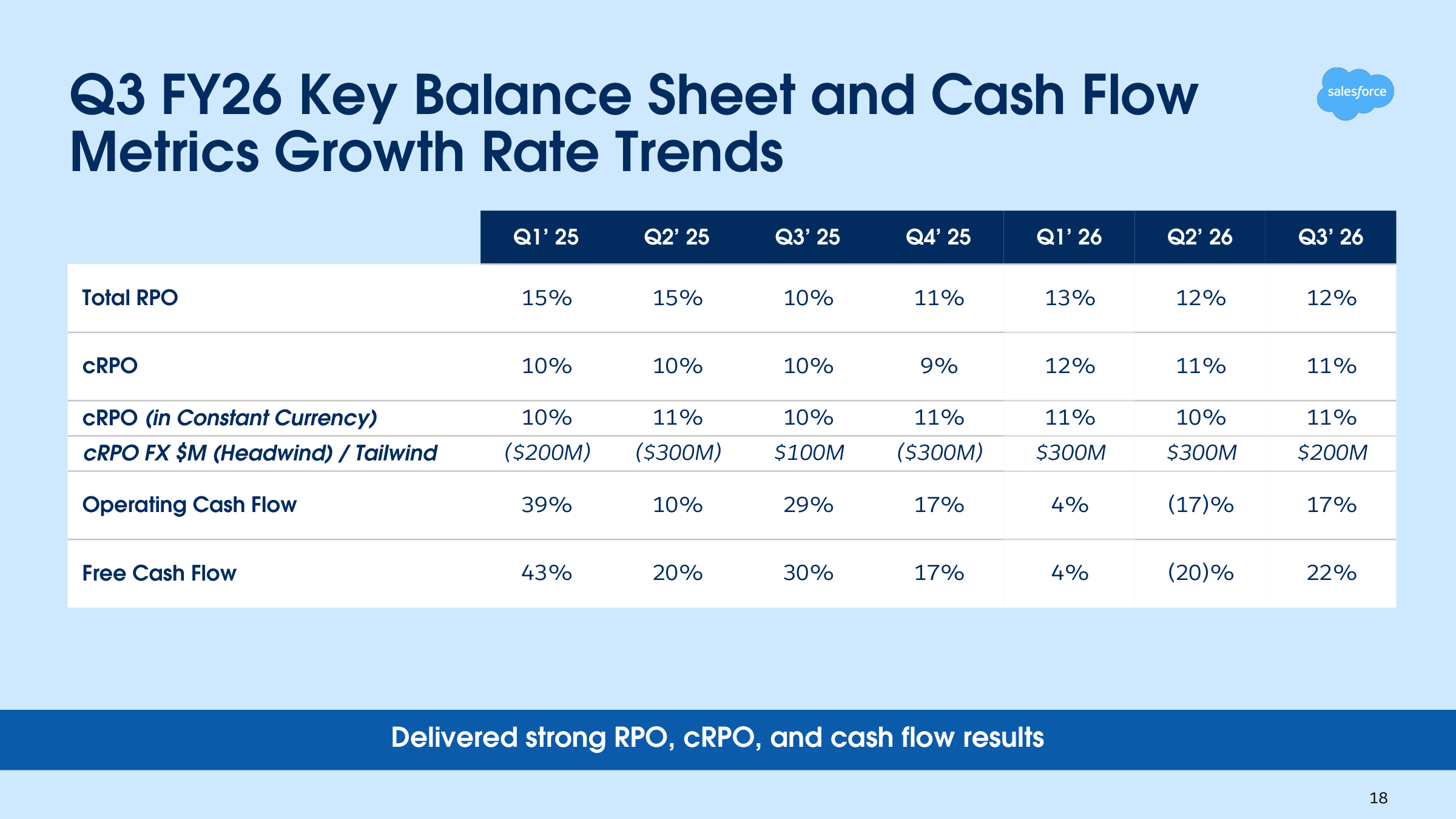

Right now, Salesforce’s cRPO (current Remaining Performance Obligation) is sitting at a massive $29.4B, and total RPO is an even bigger $59.5B.

Even better, management is guiding Q4 FY26 cRPO growth at ~15% Y/Y. As long as that contracted backlog keeps swelling, the “DIY AI” threat remains a ghost story.

2. Agentforce monetization keeps moving line of sight

It’s one thing to have a slick AI presentation; it’s another to get enterprises to open their wallets for it. But the numbers are moving. Agentforce and Data 360 ARR reached nearly $1.4B, up an impressive 114% Y/Y.

Drill down further: pure Agentforce ARR surpassed half a billion, up a staggering 330% Y/Y. We are also seeing paid deals up 50% QoQ.

That is the sound of the cash register ringing, folks.

3. The DIY fear flips into “deployment pain” demand

Management describes a secular shift toward the “agentic enterprise.” Here is the plain English translation: building AI models in a lab is fun, but deploying them securely across 10,000 employees is a nightmare.

The “last mile” is where enterprise IT projects go to die. Ultimately, big companies prefer buying from vendors who can actually ship functional, secure products. When DIY pain sets in, they will call Salesforce.

4. The reacceleration clock stays intact

During the call, Robin Washington reiterated they’re on track to reaccelerate revenue in 12 to 18 months. I love this. That’s a claim with a hard deadline. Deadlines are fantastic for investors because they keep management honest and their feet held to the fire.

Atomic Take: The “way forward” for this stock isn’t about riding AI vibes — it’s about watching the backlog + paid adoption + reacceleration-by-deadline, with heavy cash returns acting as the stabilizer while the narrative fight plays out in the market.

Falsifier: Agentforce/Data 360 ARR is high but cRPO growth actually decelerates — that would be a red flag, implying they are generating temporary excitement without securing durable, long-term contracts.

Financial Quality Rubric (1–5)

I like to look at the underlying plumbing of a business before I buy the house. Let’s grade the structural integrity here:

Revenue durability: 4/5

Make no mistake, this is still a highly sticky subscription business, not a low-margin services business.

Margin discipline: 4/5

They posted a 21.3% GAAP operating margin and an eye-popping 35.5% non-GAAP operating margin. The discipline is holding.

Cash conversion: 4/5

This is a cash-minting machine. Operating cash flow is incredibly robust versus the net income of $2.086B.

Balance sheet resilience: 4/5

Cash & cash equivalents were $8.978B balanced against noncurrent debt of $8.438B. They have the fortress they need.

Capital allocation: 4/5

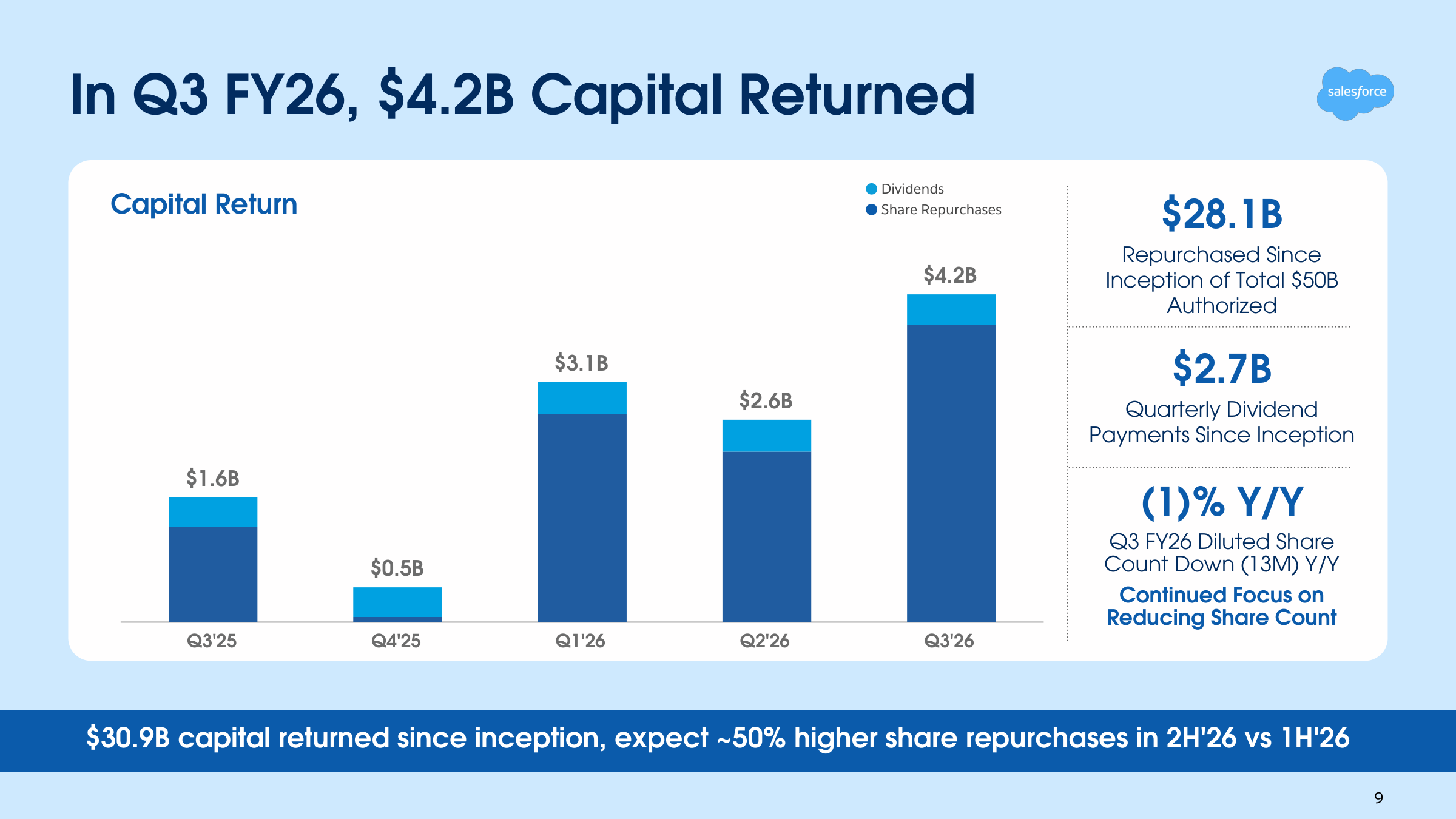

The repurchases and dividends here are not symbolic, tiny gestures meant to appease activists; they are large and ongoing (we will get to the cash flow below).

Narrative risk (AI + culture/politics): 2.5/5

The AI disintermediation fear is loud enough that it literally had to be discussed on the earnings call.

Separately, Wired reports employee backlash tied to Marc Benioff’s ICE comments.Never ignore culture. Internal politics can quickly become an execution drag during major platform transitions.

Now, let me remind you that non-GAAP margins can sometimes look like a superhero cape masking a dad bod.

GAAP is where the actual laws of financial physics live, and it includes items (like restructuring costs) that can linger a lot longer than management’s sunny PowerPoint deck suggests.

Atomic Take: Financially, Salesforce looks exactly like a mature compounder with a highly measurable AI call option attached to it. The entire debate is whether this AI option translates into durable, long-term economics or if it’s just a beautifully produced demo loop.

Falsifier: GAAP operating margin drops while revenue growth stays stuck in the high-single digits — that would suggest their newfound “discipline” was just a temporary phase, not a structural foundation.

Alright, let’s have a look at the financial statements.

The Balance Sheet (The Geiger Test)

Let’s look under the hood. As of Oct 31 2025, Salesforce held a massive $8.978B in cash & cash equivalents. Add to that marketable securities of $2.345B. They have plenty of dry powder.

Stop & Think: A fortress balance sheet buys you the most valuable asset in the tech world: time. Time to figure out the AI transition without the bond vigilantes knocking on your door.

But the “enterprise software reality” is also here: they are carrying goodwill of $52.4B. Now, this is perfectly normal for a company with a long, aggressive acquisition history (MuleSoft, Slack, Tableau, etc.). But it is exactly why forward demand signals matter so much. When growth stops, that mountain of goodwill stops looking like a history of smart buys and starts looking like a massive future impairment question.

On the liability side, the recurring-revenue engine shows its absolute beauty in unearned revenue: $14.996B. That is money sitting in their pocket for services yet to be rendered.

Atomic Take: The balance sheet is highly liquid and not debt-stressed. The key sensitivity here isn’t bankruptcy; it’s growth durability. Why? Because goodwill-heavy balance sheets absolutely hate stagnation.

Falsifier: A sustained decline in total RPO (as of quarter-end, USD, company metric) — that would be the canary in the coal mine, turning “normal goodwill” into “headline impairment risk.”

Cash Flow (The Turbine)

Cash is the lifeblood of any business, and here’s the plain-language bridge of how the Salesforce turbine is spinning.

GAAP net income was $2.086B. But the actual cash coming in the door—Operating cash flow—was $2.316B.

You have to maintain the machine, so capital expenditures were $0.139B.

If we take OCF and back out those capex costs, the simple cash proxy (or free cash flow) is ~$2.177B.

Now, let’s look at the capital return reality check. Share repurchases were an astonishing $3.801B and dividends were $395M.

Did you catch that?

The money they are sending back to shareholders exceeds the simple cash proxy for the quarter. That means these returns are not being funded purely by that quarter’s operating cash after capex.

It tells you the tempo of their capital return program is incredibly aggressive.

Atomic Take: Cash generation is undeniably strong — but the capital return pace is even stronger. As an investor, you need to watch the turbine (the operating cash flow), and not just get distracted by the fireworks (the massive buybacks).

Falsifier: Operating cash flow growth misses the company’s ~13–14% Y/Y guide (FY26, %, company guide) — if that engine sputters, it would eventually force management to rethink their aggressive capital return tempo.

Income Statement (The Reactor)

Let’s look at the core reactor for Q3 FY26 (GAAP):

Revenue was $10.259B (USD). The gross margin is shown at an elite 78%. Operating income pumped out $2.188B, and the bottom line net income was $2.086B.

When you strip out the noise, non-GAAP operating margin was 35.5%, driven largely by the company’s adjustments.

Atomic Take: The core reactor of this business is highly stable. The entire debate on Wall Street right now is whether the new fuel (AI agents) actually increases the reactor’s output, or if it just adds a glossy new control-room label to the exact same machine.

Falsifier: Non-GAAP remains perfectly smooth while GAAP profitability silently deteriorates — that’s the moment when “adjustments” start doing too much heavy lifting and narrative work.

Valuation and Quality

Before I even look at a stock chart, a company has to earn the right to be in my portfolio by passing a basic quality check. Salesforce clears the “quality business” bar with room to spare.

Look at the profitability and cash conversion: they are sitting on a massive 78% gross margin and a 21.3% GAAP operating margin. When you have margins that thick, you have the ultimate shock absorber for whatever the economy throws at you.

Owner Yield

Alright, let’s talk about what we are actually paying for this machine.

Share price: $189.72.

Shares used in computing diluted EPS: 952M (Q3 FY26, shares).

Do the simple math, and that implies a rough market cap proxy of ~$180.6B (USD, derived from price × diluted shares).

Now, let’s look at the cash proxy anchored in the actual reported lines, not the adjusted fantasies. For the first nine months of the year (9M FY26), operating cash flow was $9.532B and capex was a measly $0.453B.

Subtract the capex from the operating cash, and your 9M FCF proxy is ~$9.079B (USD, derived).

If we annualize that 9-month figure as a straight run-rate (and I’ll be the first to tell you, this is a blunt tool, so treat it as such), you get ~$12.1B/year.

Put that against our market cap proxy, and it implies a run-rate FCF yield of ~6.7%.

Now, a run-rate math is not the gospel truth. It’s a Geiger counter. It tells you the “implied burden” the current stock price puts on the business; it doesn’t tell you the exact temperature of the reactor.

Stop & Think: A 6.7% free cash flow yield on a dominant enterprise software company? Five years ago, Wall Street would have trampled you to buy that. Today, they are leaving it on the sidewalk. Why?

The reason is that the market is currently pricing the “SaaS scare” as a permanent, structural decline.

Management, on the other hand, is screaming from the rooftops that this is just a temporary mismatch, and they are putting a hard timeline on reacceleration: 12 to 18 months.

Because of the steep drop to today’s price of $189.72, the burden of proof has entirely shifted. You no longer have to believe in “hypergrowth to the moon” to make money here. You just have to believe in “durability + credible reacceleration.”

Atomic Take: At this level, the debate isn’t “is Salesforce cheap?” — it’s “is the market over-penalizing a highly durable cash generator just because the AI narrative temporarily spooked the multiple?”

Falsifier: If the 12–18 month reacceleration timeline slips meaningfully, and there is no forward-demand strength (like cRPO) to compensate, then you are stuck in a value trap: a cash machine with a permanently discounted story.

Risks (The Meltdown List)

I never buy a stock without looking for the trap doors. Here are the very real risks we are monitoring:

1. AI disintermediation risk (the core “SaaS scare”)

FACT: The fear that AI is “injurious to the SaaS application layer” is explicitly and officially an issue.

HYPOTHESIS: Value capture shifts upward to the AI models and orchestration layers, leaving legacy apps as thin, easily replaceable wrappers.

MONITOR: We watch Agentforce paid-deal momentum vs guidance. If they can’t sell the AI, they become the wrapper.

2. Backlog conversion risk

FACT: RPO includes unbilled amounts that are not yet recorded on the balance sheet. It’s contracted, but it’s not cash in the bank yet.

HYPOTHESIS: The backlog stays high on paper, but it actually converts to cash much slower because enterprise AI deployments elongate and get bogged down.

MONITOR: We need to watch the cRPO-to-revenue conversion trend and management’s commentary on deal cycles.

3. Capital return sustainability risk

FACT: Repurchases were a massive $3.801B and dividends were $395M (Q3 FY26, USD, GAAP cash flow).

HYPOTHESIS: If the core cash generation softens, the tempo of these massive returns will slow down—and investor sentiment will take a brutal second hit.

MONITOR: Keep a hawk’s eye on FY26 operating cash flow growth vs guidance.

4. M&A / integration risk

FACT: The Informatica acquisition is referenced as completed in the presentation deck.

HYPOTHESIS: Digesting massive acquisitions is hard. Integration could distract management from execution right in the middle of a critical AI platform shift.

MONITOR: Watch for any slippage in margin discipline and their forward guidance posture.

5. Culture / politics / brand risk (the sneaky risk)

FACT: Wired reports employee backlash tied to Marc Benioff’s ICE-related comments, including calls for denouncement and restrictions on use.

HYPOTHESIS: Talent bleeding and customer optics degrading at the exact worst possible moment (during a major platform transition) can cripple a software company.

MONITOR: Watch for repeated internal friction becoming external customer friction (but only react when explicitly acknowledged in primary sources, not just rumor mills).

Atomic Take: The biggest risk here is not “Salesforce can’t do AI.” The biggest risk is “the market simply decides Salesforce can’t capture AI economics,” and keeps the multiple severely compressed until the KPIs force a reset.

Falsifier: Agentforce/Data 360 ARR stays strong on the surface, but cRPO stalls out — generating PR excitement without contracted demand is exactly how narratives die.

The Atomic Verdict

★★★★☆ (4/5)

(IMPORTANT: Star system is not a buy recommendation, only a judgement for the quality of the business based on my parameters. DYOR)

The cash engine is humming.

They posted $2.188B in operating income and $2.086B in net income (USD, GAAP), backed up by operating cash flow of $2.316B (USD, GAAP). Let me be clear: this is not a liquidity panic or a margin collapse story. The physics of the business are sound.

Why the stock can still act allergic anyway: The market is currently trading a thesis about the future of SaaS economics—and that fear is directly captured in the transcript.

Management’s rebuttal is essentially: DIY has peaked, real enterprise deployment is hard, and customers are moving from science-fair experimentation to production agents. Wall Street will only believe this when the backlog and monetization make it too expensive not to.

Upgrade Triggers (Measurable things that make me more bullish):

cRPO growth stays around the guided ~15% Y/Y level while subscription & support constant-currency growth improves from its ~9% rut.

Agentforce paid deals continue meaningful QoQ growth from the >9,500 paid baseline.

Hard evidence that the “12–18 months” reacceleration clock is actually showing up in reported growth rates, not just in executive talking points.

Downgrade Triggers (Measurable things that make me run for the hills):

cRPO growth misses guidance and trends down from the $29.4B base.

Agentforce/Data 360 ARR growth decelerates sharply from that impressive 114% Y/Y level (Q3 FY26, company-defined).

GAAP operating margin compresses meaningfully from the 21%+ level while growth stays stuck in the high-single digits.

Atomic Take: Salesforce is a highly disciplined cash engine fighting a brutal narrative war. And in the stock market, narrative wars end when the next two quarters’ KPIs make one side look completely unserious.

Falsifier: If forward demand (cRPO) fails to support the reacceleration timeline, this stock stays Overhang-Heavy regardless of how good the cash returns look.

Note from me:

On Wednesday, February 25, 2026, Salesforce reports Q4 and full-year FY2026 results after the close. Headlines will do what headlines do, so the “cheat sheet” is the underlying scoreboard: cRPO (forward demand), Agentforce paid deals (AI monetization traction), and whether subscription & support constant-currency growth and GAAP operating margin are holding up.

Reference List (Sources Used)

Salesforce, Inc. “Q3 FY26 Quarterly Investor Deck”. Used for: KPI tiles, subscription & support disaggregation, constant-currency growth tables, regional growth, capital return framing, and non-GAAP expense profile (slides 5, 8, 9, 15, 16, 17, 18, 19).

Salesforce, Inc. “Q3 FY26 Earnings Press Release”. Used for: GAAP income statement items, margins, cash flow figures (CFO, capex, FCF), balance sheet line items (cash, unearned revenue), and RPO/cRPO disclosures.

Salesforce, Inc. “Q3 FY26 Earnings Conference Call Transcript” (Salesforce Investor Relations / Q4 CDN-hosted transcript; accessed Feb 14, 2026). Used for: the “SaaS scare” framing (investor question), management’s rebuttal (DIY vs deployed agents), and the 12–18 month revenue reacceleration timeline language.

Salesforce Investor Relations site (investor.salesforce.com; accessed Feb 14, 2026). Used for: document hosting/verification context.

Wired (web article; accessed Feb 14, 2026). “Letter Salesforce Employees Sent After Marc Benioff’s ICE Comments.” Used for: culture/politics headline risk context.

Nasdaq (web page; accessed Feb 14, 2026). “CRM Insider Activity.”

Disclaimer

This Deep Dive is an educational breakdown of a public company based on information available in the materials provided (e.g., annual/quarterly reports, investor presentations, earnings transcripts) and my interpretation of that information. It is designed to be a “bolt-on” intelligence layer to your own due diligence — not a replacement for it.

Independence: I do not accept compensation of any kind from the companies discussed. My research is driven solely by my personal search for high-quality compounders.

Skin in the Game: Unless otherwise stated, assume the author may hold a long position in securities mentioned. Any position creates bias — treat this as commentary, not gospel.

Not Financial Advice: Nothing here is investment advice, a recommendation, or a solicitation. I am not a financial advisor. You are responsible for your own decisions. The stars rating is not a buy recommendation, but meant as a guide to understand the quality of the financial statement of the respective companies.

Error & Update Risk: Financial statements change, companies restate, guidance evolves, and I can be wrong. Verify key figures in the primary filings and consider reading the footnotes before deploying capital.

Large-cap SaaS with defendable moats and pricing power like CRM look very attractive at these levels

Salesforce is getting very attractive here. While I don’t think it has the greatest upside relative to other names in the sector, have to think we’re getting close to a floor here given their domain expertise