The Money Mind: Bill Miller and the 1 in 2.3 Million Anomaly

Deconstructing the pragmatic mechanic that crushed the S&P 500 for a decade and a half, and why calculating odds will always beat predicting the future.

1. The “Impossible” Stat

If you had to calculate the odds of a mutual fund manager beating the S&P 500 for 15 consecutive years, the math is brutal: it is roughly a 1 in 2.3 million probability.

In the hyper-competitive arena of Wall Street, where the brightest minds routinely underperform basic index funds, Bill Miller achieved the impossible. Managing the Legg Mason Value Trust from 1991 to 2005, Miller didn’t just beat the market; he shattered the conventional boundaries of how to value a business.

He didn’t build his unparalleled streak by clinging to safe, predictable assets. He did it by making massive, highly concentrated bets on companies the old-guard “value investors” were terrified of—most notably, turning an early stake in a profitless online bookstore called Amazon into a 24x return.

But Miller’s strategy isn’t magic. It is a highly specific, probability-driven operating system designed to exploit the market’s inability to price the distant future.

2. The Origin Story

Bill Miller’s edge didn’t come from a finance textbook, but from the philosophy department.

Before he ever managed a dollar on Wall Street, Miller served as an intelligence officer in the U.S. Army and pursued a PhD in philosophy at Johns Hopkins University. It was there that he became obsessed with “pragmatism,” a school of thought that fundamentally rewired his brain.

While traditional value investors were rigidly backward-looking—obsessing over past earnings, tangible book value, and historical P/E ratios—pragmatism taught Miller to look beyond the obvious and calculate future possibilities.

This philosophical lens gave Miller his ultimate unfair advantage. He realized that the stock market was obsessed with certainty, demanding immediate GAAP (Generally Accepted Accounting Principles) profitability.

By breaking his reliance on backward-looking analytics, Miller became perfectly positioned to spot value where others only saw risk: the chaotic, fast-paced frontier of the early internet.

3. The Superpower (The Mechanic)

To traditionalists like Benjamin Graham, Miller was a heretic. But Miller’s superpower was recognizing a fatal flaw in Wall Street’s tribalism:

The false dichotomy between “Value” and “Growth.”

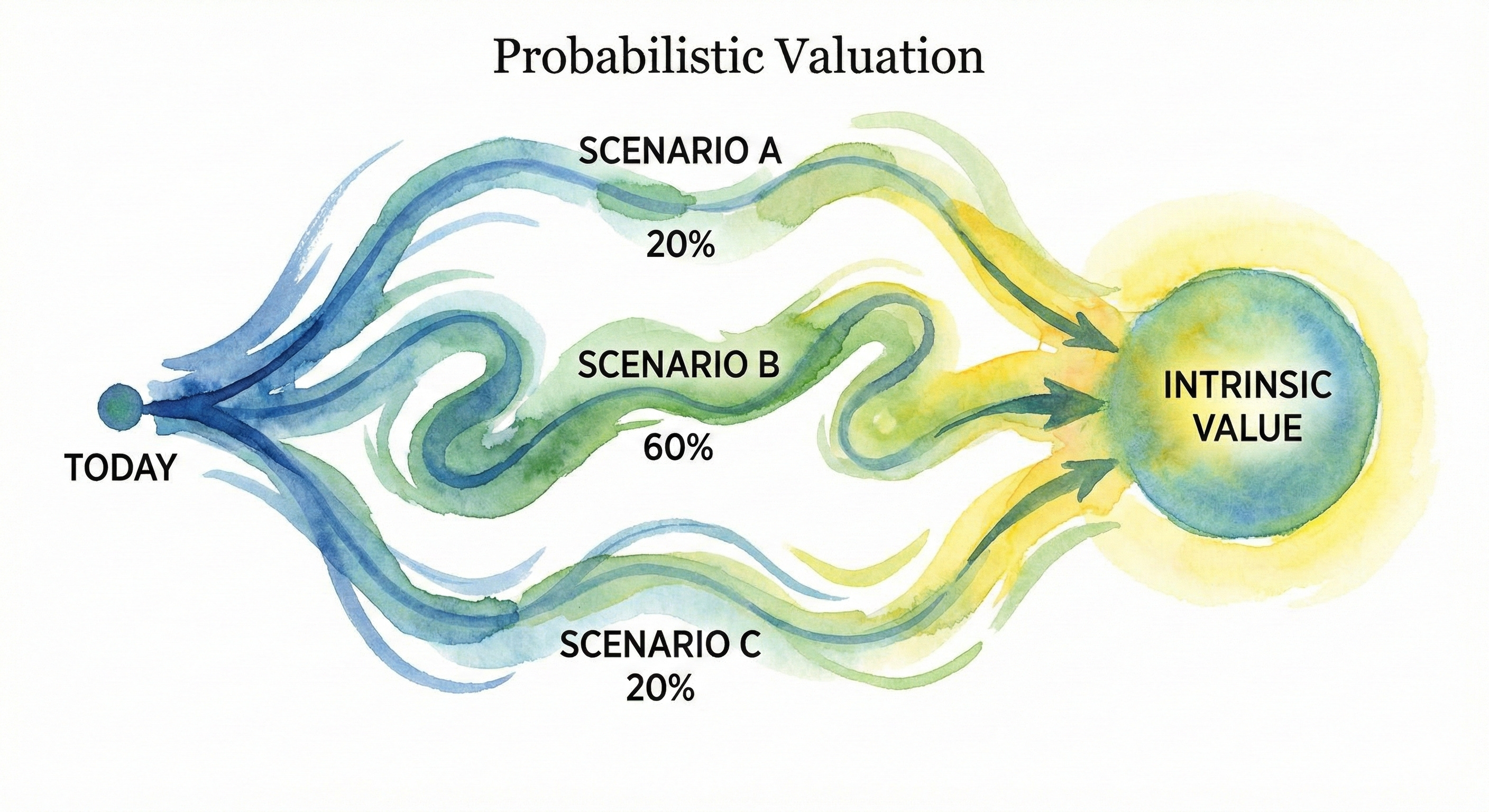

Miller famously declared, “Growth is an input into the calculation of value.” He realized that any stock could be a value stock if it traded at a discount to its intrinsic value. Instead of looking for companies trading at low multiples of today’s earnings, Miller built his strategy on probabilistic valuation.

The mechanic works like this:

Ignore the GAAP, Follow the Cash: Miller discarded traditional accounting profits. He defined intrinsic value purely as the present value of future free cash flows, discounted back to today.

The Cost of Capital Hurdle: He hunted for businesses whose economic models allowed them to earn returns on capital above their cost of capital over an entire economic cycle.

Scenario Weighting: He didn’t try to predict one exact future. He envisioned multiple scenarios for a business, assigned a probability to each, and summed them up to find the “central tendency of value.”

This is how he bought Amazon in 1999. While Wall Street panicked over Amazon’s negative accounting profits, Miller recognized the economies of scale Jeff Bezos was building. He calculated that the massive future free cash flows justified the price, leading him to snatch up a 15% stake in the company.

To Miller, Amazon wasn’t an expensive growth stock; it was a deeply undervalued cash machine hiding in plain sight.

4. The Graveyard (The Risk)

If you play the odds aggressively enough, eventually, you draw a catastrophic hand. For Miller, that hand was dealt in 2008.

Miller’s operating system relied on a specific mechanic: “Lowest Average Cost Wins.” When a high-conviction stock dropped, he didn’t panic; he averaged down and bought more.

This strategy had saved him during the dot-com bust and the Savings and Loan crisis in 1990, where his 40% portfolio concentration in beaten-down financial stocks eventually propelled him to massive gains.

But in 2008, the global financial system wasn’t just cyclical; it was structural. As the housing market cracked, Miller used his old playbook. He loaded up on plummeting shares of Bear Stearns, Citigroup, AIG, and Freddie Mac. He caught a falling knife, and it severed his portfolio.

He bought Bear Stearns at $30 just days before it collapsed. He stubbornly held Freddie Mac even as colleagues begged him to sell, only to watch it get wiped out by government nationalization in September.

Because of these bets, his value fund lost over $12 billion in AUM, underperforming the S&P 500 by 20 percentage points. The losses were permanent, proving the brutal reality of his leverage-like concentration: when the rules of the game change entirely, the historical playbook becomes a death sentence.

5. Steal Their Brain (The Toolkit)

You don’t need a PhD from Johns Hopkins to invest like Bill Miller. You just need to steal his mental models. Here is the toolkit:

The “Probability Matrix” * The Concept: Stop asking “What will happen?” and start asking “What are the odds?”

The Actionable Rule: Never value a company based on a single outcome. Map out three scenarios (Worst, Base, Best), assign a percentage likelihood to each, and blend them. If the current stock price is vastly lower than your blended value, buy.

The “Lowest Average Cost” Mandate

The Concept: If you are right about the intrinsic value, a dropping stock price is a gift, not a warning.

The Actionable Rule: When you buy a stock, mentally prepare for it to drop 20%. If nothing fundamentally changes about the business’s long-term cash flow, you must be willing to buy more.

The “Silver Bullet of Simplification”

The Concept: Complex models create false confidence.

The Actionable Rule: Throw out the 50-tab Excel spreadsheets. Identify the 3 or 4 critical variables that actually drive the business. If you can’t map the future value on those few variables, it’s just noise.

6. The Human Factor (The Quirk)

The 2008 crisis didn’t just break Miller’s portfolio; it broke him physically. The stress of the financial collapse was visceral. Miller reportedly gained 40 pounds during this era.

He spent his nights waking up in a cold sweat, constantly checking his beaten-down stocks as his reputation was shredded in the pages of The Wall Street Journal, and he was unceremoniously fired from a $2.2 billion pension board.

But Miller’s ultimate human quirk is an unyielding, almost stubborn resilience.

He views losses as “tuition payments.”

Later in his career, he ruthlessly purged the complexity from his life. He stopped building financial models, calling them “stupid,” and retreated from the corporate spotlight of Legg Mason to run a smaller, highly concentrated fund under his own name.

He adopted a minimalist approach to data, tuning out the macroeconomic panic of the day to focus entirely on deep, intellectual curiosity—an evolution that eventually led him to place massive, highly lucrative bets on Bitcoin when the rest of Wall Street laughed at it.

7. The Verdict

Bill Miller is the patron saint of the “Contrarian Optimist.” He proved that you can generate monumental wealth by ignoring labels, trusting probabilities, and stepping into the fire when everyone else is running for the exits.

Copy this style if:

You possess a stomach of absolute steel and do not panic when your portfolio drops 30%.

You view stocks as fractional ownership of future cash flows, not squiggles on a chart.

You are comfortable looking like a fool in the short term to be proven a genius in the long term.

Run away if:

You rely heavily on standard metrics like P/E ratios and GAAP earnings to feel “safe.”

You cannot mentally separate a company’s stock price from its underlying business fundamentals.

The idea of averaging down on a plummeting stock keeps you awake at night.

It’s wild to think that a PhD in philosophy was the "unfair advantage" behind a 1-in-2.3-million-year winning streak. I don't know much about the math of Wall Street, but Miller's shift from backward-looking stats to future probabilities sounds fascinating. :)

Do you think this "pragmatist" edge still works in today’s hyper-fast market, or has AI and instant data made it impossible for a human to spot those mispriced futures anymore?

We aren't in the same field, but I'd love to support each other feel free to subscribe if you like my content too!

Jorrit

I think you’re the first person I’ve seen mention Bill Miller on Substack, and honestly, I’m not surprised it’s you. Really strong post!