The Money Mind: Tom Gayner

How Tom Gayner Compounds Wealth (and Life) by 1% and by focusing on being directionally correct.

I actually got the idea for this installment of The Money Mind from a comment a paid subscriber left on a recent portfolio update. They laid out a beautifully detailed, incredibly sharp bear case against one of my core holdings. It was the kind of feedback you can’t ignore; analytically tight and logically sound.

So… I couldn’t do much else but acknowledge his brilliant perspective, but the exchange reminded me of a fundamental truth about markets and life: the world is far too complex to determine with absolute accuracy.

In the long run, it is much healthier, and infinitely more profitable, to focus on being directionally correct.

And nobody embodies that truth better than the man featured in this issue of Money Mind.

William Green spent years interviewing the world’s greatest investors for his book Richer, Wiser, Happier. He expected to find ruthless optimizers. What he found instead, again and again, was something far more disarming: people who had made peace with uncertainty, and built their entire advantage around that peace.

Tom Gayner is perhaps the purest expression of that finding.

Green profiles him not primarily as a stock-picker, but as a man who has constructed an entire life around a single, quietly radical idea: that you don’t need to be right. You just need to be directionally right. And that distinction, compounded over decades, turns out to be worth billions.

Who is Tom Gayner?

Gayner is the CEO and Chief Investment Officer of Markel Corporation, a specialty insurance company based in Richmond, Virginia. To call it unglamorous would be generous.

Markel doesn’t make headlines. It doesn’t disrupt anything. It insures niche, hard-to-price risks (collectible cars, summer camps, horse farms) and it has done so, profitably and quietly, for decades.

Gayner joined Markel in 1990 as an investment officer, trained as a CPA. He arrived with a ledger mindset: systematic, methodical, allergic to sloppiness. Over time, he became the architect of its entire capital philosophy.

Today Markel is often called a “Baby Berkshire”, a comparison earned through a genuine philosophical kinship with how Buffett thinks about business and time.

His personal track record across decades is one of the most consistent in institutional investing.

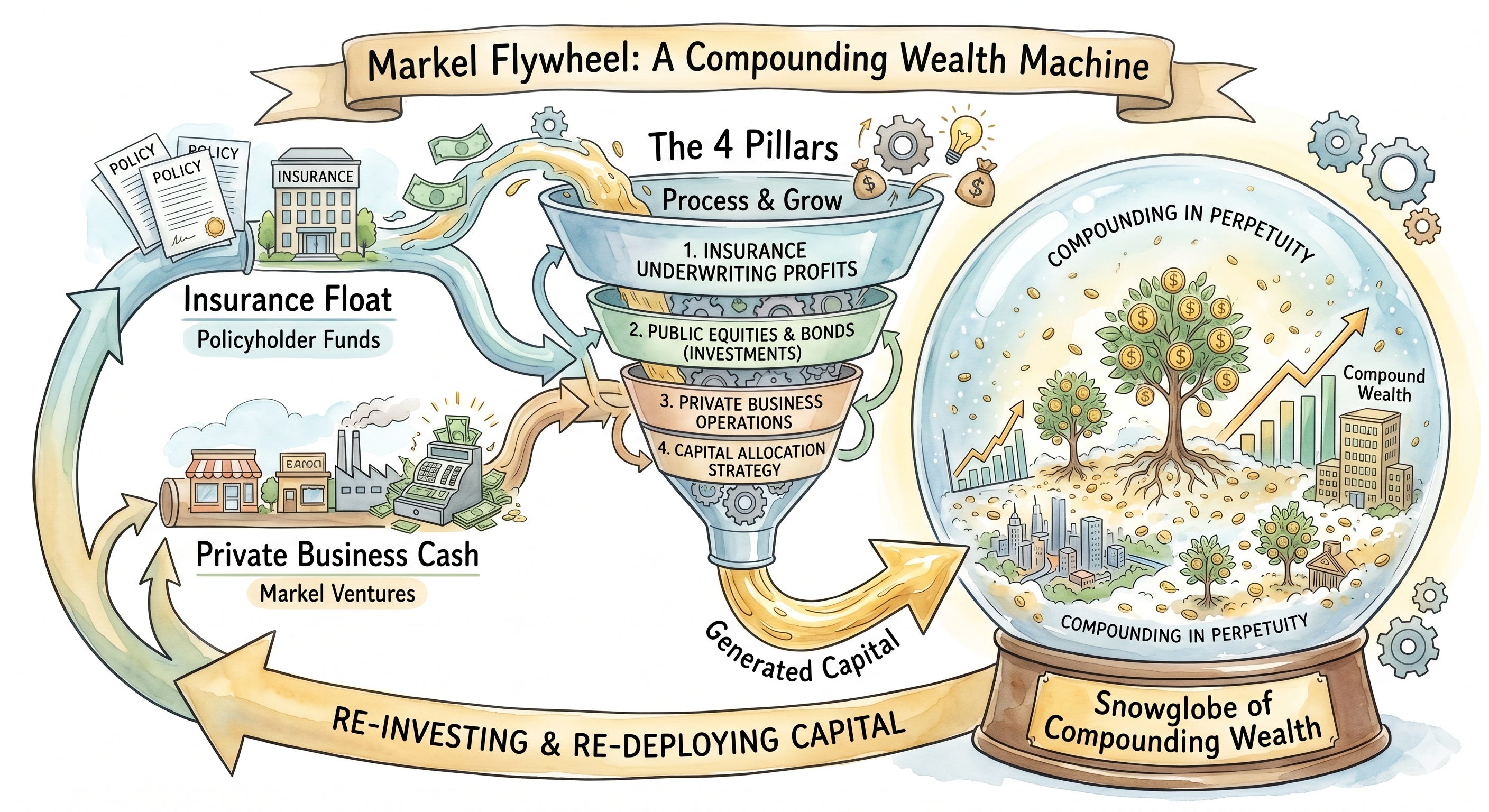

The Accident of Float

To understand Gayner’s edge, you need to understand one structural fact about insurance companies: they collect premiums before they pay claims.

The money sitting in between (sometimes for years) is called the float. It belongs, technically, to future claimants. But until those claims arrive, it can be invested.

Most insurance companies invest their float conservatively, in bonds. Gayner invests Markel’s float in equities, and holds them for years, sometimes decades. Because the float is large, sticky, and doesn’t demand sudden redemption, he never has to sell into a bad market.

He simply waits.

This is a structural advantage most individual investors can’t replicate. But the philosophy underneath it, the willingness to sit still, to resist the pressure to act, is entirely transferable.

The Four Pillars

Gayner filters the entire universe of publicly traded companies through four questions. They are almost aggressively simple:

1. Is the business highly profitable, with strong returns on capital and low debt?

Not flashy revenue growth. Return on capital. He wants businesses that make more money than they consume.

2. Does management have both ability and integrity?

He treats these as inseparable. A brilliant but dishonest management team is worse than useless — they’ll find creative ways to enrich themselves at shareholders’ expense.

3. Are there reinvestment opportunities within the business?

A great business that can’t grow is a melting ice cube. He wants companies that can plow their own profits back into further growth, compounding internally.

4. Is the price fair?

Not cheap. Fair. He’s not hunting for distressed bargains. He’s willing to pay a reasonable price for an exceptional business, and let time do the work.

When all four align, he buys. Then, characteristically, he does very little else.

“Directionally Correct”

In Richer, Wiser, Happier, Green captures something essential about Gayner’s psychology: he is profoundly unbothered by being wrong in the short term, because he has thought carefully about what kind of wrong he can tolerate.

Gayner once described wanting to return to his college weight. His plan wasn’t a diet. It was to lose one pound a year for ten years.

Excruciatingly slow.

Entirely sustainable.

Completely successful.

This is the Gayner framework in miniature. He doesn’t ask: is this the perfect trade at the perfect price on the perfect day? He asks: is this the right direction? If the answer is yes, he acts. Then he waits. Then he compounds.

Green’s broader argument in the book is that the investors who survive and thrive across long periods share a particular kind of temperament; what he calls equanimity. In other words, the ability to remain calm when the crowd panics, and to resist action when action is not warranted. Gayner is his clearest example.

This runs against everything Wall Street rewards. Financial culture prizes speed, activity, decisiveness. Gayner prizes stillness. He’s made a fortune from it.

The Markel Style

What makes Gayner unusual even among patient, value-oriented investors is that he refuses to separate his investment philosophy from his values as a person and an employer.

Markel operates according to something called the Markel Style, a document that has guided the company’s culture for decades. Its logic inverts the standard corporate hierarchy: customers win first, employees win second, shareholders win third.

If you genuinely serve the first two, shareholder returns compound naturally as a byproduct. Exploit either group and the whole machine corrodes.

The Markel Ventures Family

This is where the Markel Style becomes most visible. Rather than owning a collection of abstract equity stakes, Gayner has assembled what he calls a “family of companies” — unglamorous, capital-efficient businesses run by people he genuinely trusts, operating with a high degree of autonomy under a shared set of values.

The portfolio spans industries that couldn’t feel further apart. And that’s precisely the point.

A few that currently call Markel home:

Markel Food Group (AMF Bakery Systems)

If you’ve eaten a fast-food hamburger bun, there’s a reasonable chance AMF’s equipment made it.

The company manufactures industrial bakery equipment used by customers to produce billions of buns, crackers, cookies, and pizzas annually. It was Gayner’s very first Ventures acquisition in 2005. Chosen, he said, partly because bread has been around for thousands of years and seemed unlikely to be technologically disrupted.

Costa Farms

The largest producer of ornamental plants in the world, founded in 1961 by Jose Costa and now a third-generation family business stretching over 4,000 acres globally.

This is Gayner’s philosophy made literal: a business so unglamorous it sells houseplants, compounding quietly for generations.

Brahmin

A creator of fashion leather handbags with significant wholesale distribution and a growing direct-to-consumer business, founded in 1982. Gayner said when Markel and Brahmin were introduced, it was immediately clear they shared the same business vision and culture.

Buckner HeavyLift Cranes

A provider of heavylift crawler cranes serving wind energy, data centers, semiconductor manufacturing, nuclear energy, and space markets.

Boring by any surface reading. Structurally essential to almost every industry building the future.

Havco Wood Products

Manufactures laminated oak and composite wood flooring for truck trailers, intermodal containers, and truck bodies. Floor panels for freight trucks. It couldn’t sound less exciting. It also isn’t going anywhere.

Others:

CapTech: An IT consulting firm.

PartnerMD: A concierge primary care and executive health company.

VSC Fire & Security: Fire suppression systems.

Ellicott Dredges: Industrial dredging equipment.

Metromont: Precast concrete.

Cottrell: Over-the-road car haulers.

Lansing Building Products: Building materials distribution.

Weldship: Industrial and specialty gas storage vessels.

Read that list aloud and you get a picture of what Gayner means by “a diverse and resilient family.”

Experts in bakery equipment, car haulers, IT consulting, medicine, industrial gas storage, ornamental plants, precast concrete, construction, fire protection, furniture, dredges, leather goods, trailer flooring, building products distribution. Not a single one of them will ever trend on social media.

That’s the whole idea. Every acquisition goes through the same four-part test: strong returns on capital with low debt; management with equal measures of talent and integrity; reinvestment opportunities with capital discipline; and a fair price. The industry is almost irrelevant.

The character of the business and the people running it are everything.

Who this is for, and who it isn’t

Gayner’s approach will bore you during bull markets. When meme stocks are doubling overnight and AI darlings are soaring, a portfolio of unglamorous, capital-efficient businesses will feel like a punishment.

You will be mocked, at least implicitly, by your brokerage app’s performance tab.

That is the price of admission. If you can pay it — if you can hold through that grinding underperformance without flinching — the math of compounding will eventually reward you in ways that the hype cycle cannot.

If you can’t, that’s worth knowing too. The first thing Gayner’s philosophy asks of you is honesty about your own temperament.

Green’s book is worth reading in full for exactly this reason. Its central argument is that the best investors are not the ones with the best models; they are the ones who know themselves clearly enough to build a strategy they can actually sustain.

Three things you can take from Gayner today

The 48-hour rule. Before any trade, wait two days. Then ask: is this driven by a real change in the business fundamentals, or by anxiety and the need to feel like you’re doing something? Most of the time, it’s the latter.

Apply the four pillars ruthlessly. Not as a checklist to rationalize a decision you’ve already made. No, use this as a genuine filter. If a holding fails any one of the four, ask whether you’d buy it fresh today. If the answer is no, that’s information.

Think about direction, not precision. You will not call the top. You will not call the bottom. Neither will anyone else, consistently. The question is whether the trajectory of your portfolio — its quality, its time horizon, its underlying businesses — is pointing the right way.

Richer, Wiser, Happier by William Green is one of the most honest books written about what great investing actually looks like from the inside. If Gayner’s thinking resonates with you, I highly recommend you give the book a read.

Had a great time at the Markel Reunion this year. I love that they are focused on the longterm and truly keep the shareholder’s interest top of mind.

Markel is a solid, resilient company with improving insurance underwriting, large investible float, good investment results over reasonable time periods and a well-diversified group of cash-generating businesses.