The Money Mind: Voya And The Profitable Art of Absolute Laziness

The Voya Fund hasn't bought a new stock since 1935. Here’s the modern applicable strategy for replicating their extreme success.

I recently started reading Chris Mayer’s excellent book (which I have already read 3 times before), 100-Baggers. It is a fascinating deep dive into the math and psychology of finding stocks that return 100-to-1.

It’s a great read, but one specific chapter stopped me in my tracks. Mayer briefly highlighted the importance of extreme long-termism by pointing to an obscure mutual fund that achieved incredible success by doing, well, absolutely nothing.

I was hooked. I went down a rabbit hole, digging through financial archives and old news clippings, including a fascinating 2015 Reuters piece detailing the fund’s history. What I found wasn’t just a quirky financial anomaly; it was a masterclass in alpha generation, the power of corporate evolution, and the staggering edge you gain by simply leaving your investments alone.

Here is the story of the Voya Corporate Leaders Trust Fund, why its radically lazy approach beat the smartest guys in the room, and exactly how we can apply its playbook today.

The Time Capsule from 1935

The story starts in 1935. The United States was grinding its way through the Great Depression. Franklin D. Roosevelt was in the White House, and the economic mood was grim.

Amidst this, the fund’s original sponsors, Corporate Leaders of America, launched a deceptively simple experiment.

They didn’t try to time the market, and they didn’t look for hidden, undervalued gems. Instead, they identified the undeniable pillars of the American economy; the industrial giants that kept the lights on, the trains moving, and the factories humming.

They bought equal amounts of stock in 30 major U.S. corporations. The blue-chips of the era like General Electric, Union Pacific, Procter & Gamble, and DuPont.

Then, they did something revolutionary: They locked the door and threw away the key.

The fund’s charter essentially forbade the managers from ever buying a new stock. They were a trust, meant to hold these specific companies forever.

For the next 80-plus years—through World War II, the Cold War, the 1987 crash, the dot-com bubble, and the 2008 financial crisis—the fund made zero active investment decisions.

The results? Astonishing.

By doing zero work, this “do-nothing” approach crushed professional active managers, beating 98% of its large-value peers over 5- and 10-year stretches. Assets that were practically “dead in the water” at $60 million in the late 1980s swelled to over $1.7 billion as the strategy’s brilliance proved itself.

The Magic of “Corporate Darwinism”

If you bought 30 stocks today and didn’t touch them for 80 years, common sense says half of them could go bankrupt and leave you destitute.

And you know what? A bunch of them did. Companies like the Pennsylvania Railroad Co. and American Can eventually went bust or faded into irrelevance. Today, only about 21 “bloodlines” of the original 30 remain.

So how did the fund survive, let alone crush the market? Because while the portfolio managers were completely passive, the underlying companies were fiercely active.

The portfolio benefited from what I like to call “Corporate Darwinism.” Over eight decades, the portfolio evolved organically through the natural lifecycle of business.

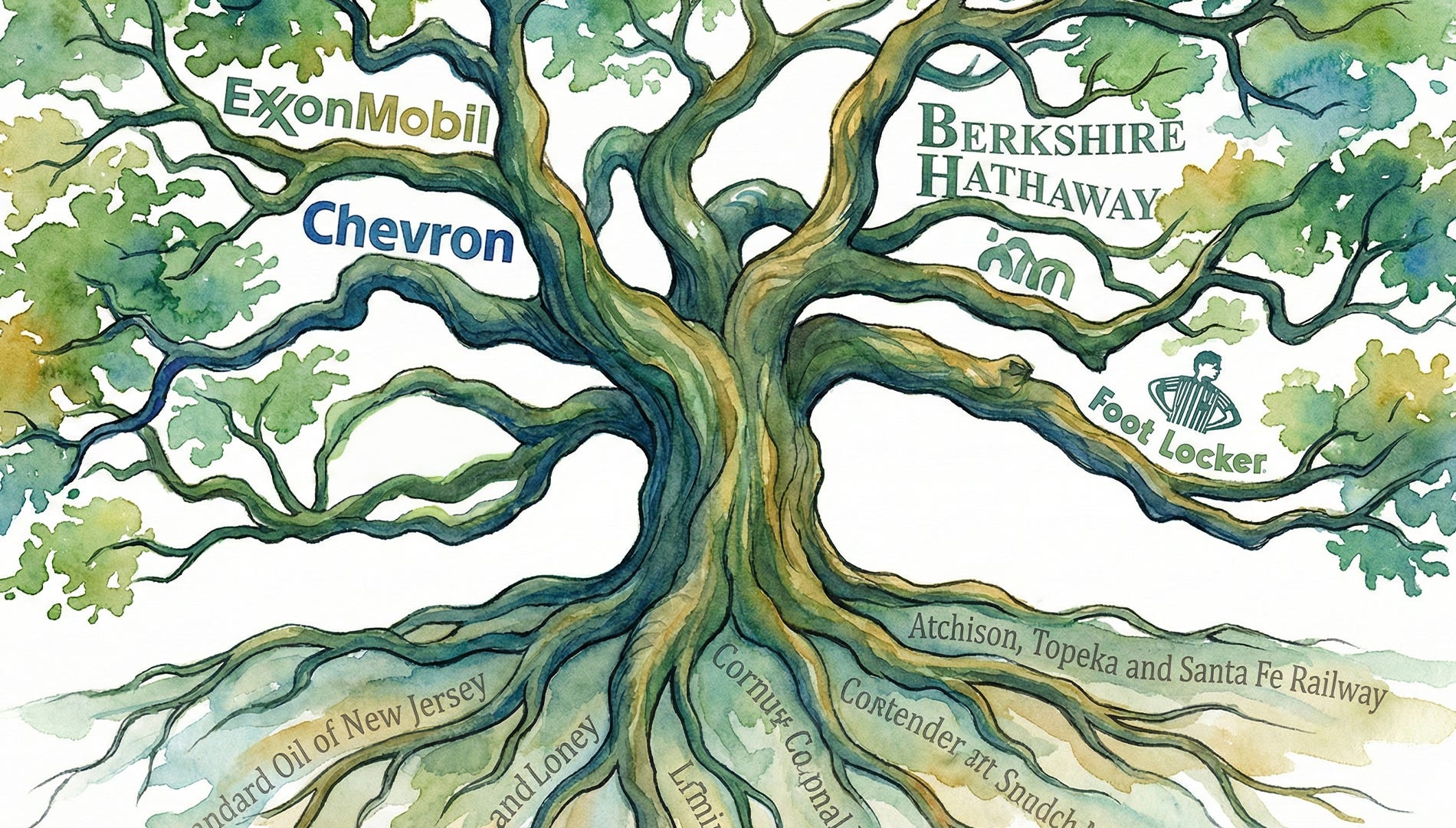

Beneficial Mutations (Spin-offs): When a massive conglomerate in the portfolio decided to spin off a division into a new, separate company, the fund simply accepted the new shares and held them. For example, the original portfolio held Standard Oil. Over decades, through antitrust breakups and mergers, that single holding automatically mutated into massive stakes in both ExxonMobil and Chevron.

Strategic Absorption (Mergers): When one of the portfolio companies was acquired by another giant, the fund received and held the stock of the new acquirer. An original holding in the Atchison, Topeka and Santa Fe Railway eventually, through a series of corporate deals, morphed into shares of Warren Buffett’s Berkshire Hathaway—which became the fund’s second-largest holding. F.W. Woolworth, the retail pioneer, eventually evolved into Foot Locker.

The lesson here is profound:

If you own the highest-quality businesses, they will find ways to survive, adapt, and acquire their way into the future. The losers in the portfolio went to zero, but the math of long-term investing is brilliantly asymmetrical.

A stock can only lose 100%, but it can grow 10,000% or more. The massive winners—the 100-baggers—more than compensated for the bankruptcies.

The Edge of Lethargy

Why did this lazy strategy work so incredibly well?

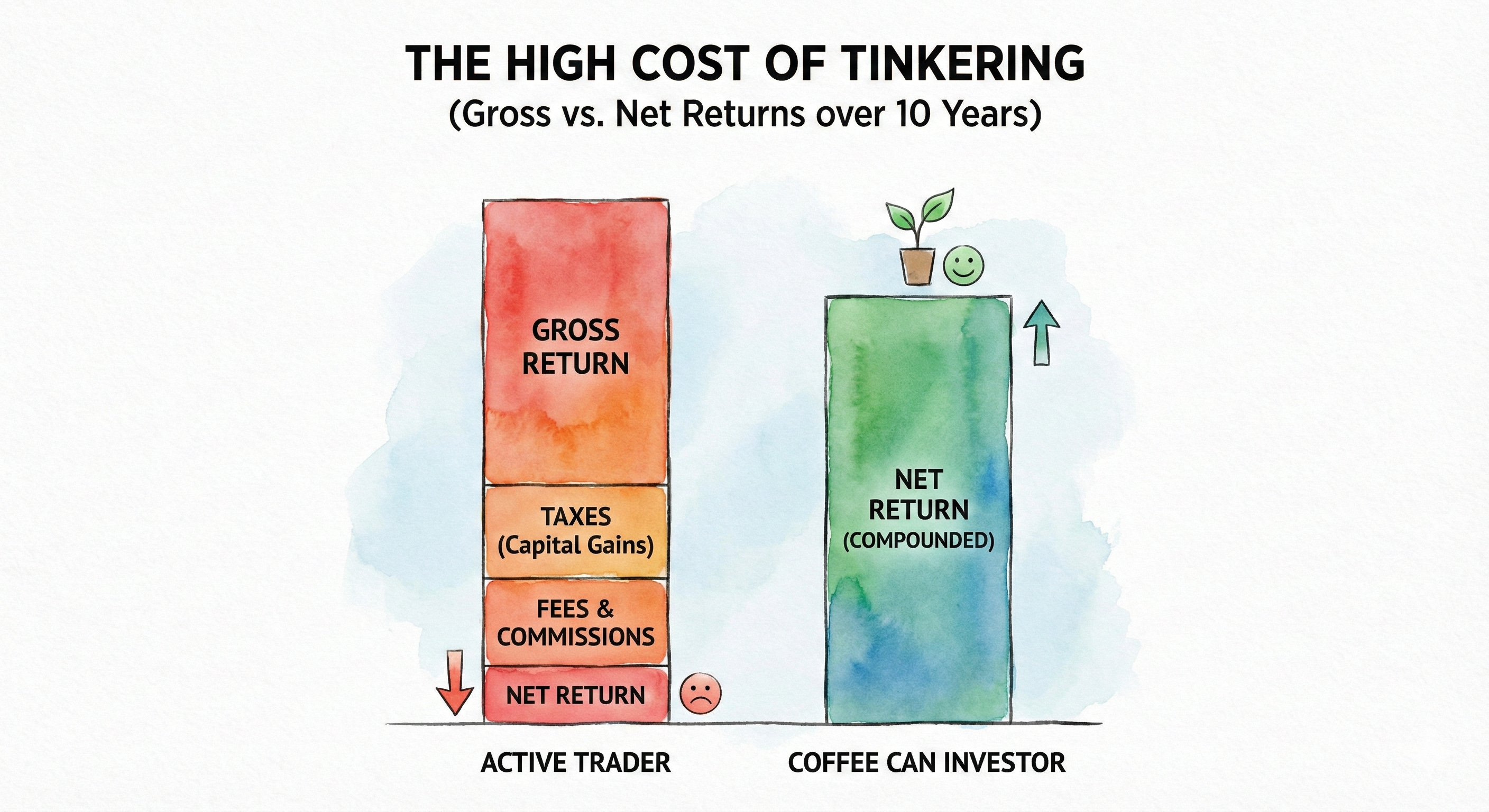

First, it eliminated human error. The greatest enemy of the investor is their own brain. We sell in a panic at the bottom and buy in a frenzy at the top. The Voya charter removed the ability for managers to make stupid emotional decisions.

Second, it created extreme tax efficiency. In taxable accounts, high turnover is a wealth killer. Every time you sell for a profit, the government takes a cut, leaving you less capital to compound. Because the fund never voluntarily sold, it generated virtually no capital gains taxes for decades, allowing nearly 100% of the capital to compound uninterrupted.

Finally, it let the winners run. Standard Wall Street advice is to “rebalance”—selling your winners to buy more of your losers. The 1935 trust did the exact opposite. It let its winners grow into massive, dominant positions that carried the entire portfolio.

The Modern Playbook: Building a 2100 Portfolio Today

I am perfectly aware that you cannot buy the Voya fund today hoping for the same century-defining returns; its portfolio is frozen in 1935 and is heavily overweight in yesterday’s economy (like oil and old industrials).

But we can emulate their exact methodology today.

To be clear: I am not enthusiastic about this strategy if it is used recklessly. If you buy 30 speculative, profitless tech companies today and lock them in a drawer for 50 years, you probably won’t get a 100-bagger—you’ll just get a tax write-off.

This extreme “do-nothing” approach only works if you are buying companies with true, atomic moats. You need businesses so deeply entrenched that they act as the raw infrastructure of the economy.

Here are the rules of engagement for building your own 80-year portfolio today:

1. The Rules of the Trust

Select 25 to 30 Stocks: This is the sweet spot. It provides enough diversification to absorb the inevitable bankruptcies of a few companies over a century, while remaining concentrated enough to let the mega-winners drive the total return.

Start with Equal Weights: Put the same dollar amount into each company.

The Blood Oath—Never Sell: This is the hardest rule. You must be mentally prepared to hold through 50% drawdowns without flinching. If a stock drops 80%, you hold. If it goes up 2,000%, you hold.

Embrace the Mutations: When your companies spin off new divisions, keep the new shares. When they merge, keep the new company. This is how your portfolio stays automatically relevant.

Reinvest Dividends: Use the dividends to buy more shares of the exact same original companies. Never add a 31st stock.

2. The Candidates: Finding Today’s “Pillars”

If you look at the original 1935 portfolio, the managers bought the obvious mega-caps of their day—heavy railroads, giant oil producers, and steel monopolies. But if our goal is to engineer a portfolio capable of returning multibaggers, and especially 100-to-1 over the coming decades, we cannot buy today’s $3 trillion tech giants. The math simply doesn’t allow a $3 trillion company to become a $300 trillion company.

When the Voya managers bought the giants of their era—companies like General Electric, DuPont, and Standard Oil—they were indeed buying the absolute largest, most dominant monopolies on earth.

But the scale of the economy was fundamentally different.

In 1935, the entire nominal GDP of the United States was roughly $74 billion. The absolute largest corporations in the country at the time had market caps hovering between $1 billion and $3 billion.

This meant that even the undisputed kingpins of American industry represented just 1% to 3% of total US economic output. They were massive, yes, but they still had a virtually infinite runway to grow alongside the industrial explosion of the 20th century.

Fast forward to today. The US GDP is pushing $28 trillion, and our modern titans—Microsoft, Apple, Nvidia—boast market caps around $3 trillion.

That means a single mega-cap tech company today represents roughly 10% of the entire US economic output. The structural ceiling has been hit. For a $3 trillion company to become a 100-bagger, it would have to grow to $300 trillion—which is more than double the GDP of the entire planet.

Therefore, to truly level the playing field and match the geometric growth runway that the Voya managers enjoyed in 1935, I don’t think we could buy today’s top 10 household names. We have to look for companies that represent the same relative economic footprint today that GE did in the 1930s.

This brings us down to the $10 billion to $50 billion market cap range (and if you want 100-baggers, preferably even less than $10 billion).

In this range, we find the “Hidden Champions”—businesses with the exact same monopolistic dominance and atomic moats as the original 1935 blue chips, but with the mathematical breathing room required to actually multiply your wealth, similar to what Voya did, over the next few decades.

Here are the modern pillars for an 80-year portfolio:

The Financial Gatekeepers: These are the businesses that act as the invisible referees of the economy. They require virtually zero physical capital to grow and operate as pure tollbooths on commerce.

Examples: Fair Isaac Corporation (FICO), MSCI Inc. (MSCI). FICO is the ultimate example; 90% of top lenders use their credit scores. It is so deeply embedded into the underwriting process of global finance that replacing it is functionally impossible.

The Civic Operating Systems: Government agencies, courts, and municipalities are notoriously slow-moving and risk-averse. Companies that digitize these institutions benefit from punishingly high switching costs; once a city adopts a system, the revenue is practically guaranteed for life.

Examples: Tyler Technologies (TYL), Motorola Solutions (MSI).

The “Dirt” Monopolies: In the digital age, physical land constraints create incredible advantages. Look for companies whose business models rely on owning physical infrastructure that nobody else wants in their backyard.

Examples: Copart (CPRT), Waste Management (WM). Copart dominates the online auction market for totaled vehicles because they own massive tracts of land near major cities to store the wrecks. No municipality is going to zone new land for a massive junkyard today, meaning Copart’s moat is made of literal dirt.

The Essential Aftermarkets: Businesses that provide the crucial maintenance, parts, and distribution for massive industries. They don’t take the massive R&D risk of manufacturing the core product; they just tax the ongoing usage and repair of it.

Examples: HEICO Corporation (HEI), Pool Corporation (POOL), TransDigm Group (TDG).

The Route-Density Masters: Service companies where unit economics drastically improve as they gain local market share. When one technician services 15 houses in the exact same neighborhood, fuel and labor costs plummet, making it impossible for a new startup to compete on price.

Examples: Rollins, Inc. (ROL), Cintas (CTAS).The Ultimate Test of Patience

The Voya Corporate Leaders Trust is a profound lesson in humility. It proves that over a long enough timeframe, the combined ingenuity of the world’s best businesses—left entirely alone by anxious humans—is an unparalleled wealth-creation machine.

To replicate this kind of success, you don’t need to trade faster or guess the next macro trend. You just need to buy exceptional quality, and then have the supreme discipline to do absolutely nothing.

But I wonder how many has tried to do something similar and failed, in hindsight we can find brilliant funds and investors but in real time it’s not that easy … this is a topic / though that I’m currently wrestling with in my mind … looking for the right answer for myself.