The Simple Truth: AVTECH AB (AVT B)

All you need to know from my 3000+ word AVTECH Deep Dive. Distilled into 3 minutes.

I write 20-page deep dives because I love digging into the numbers.

But I create these ‘Simple Truths’ summaries because I know not everyone have time read my ultra-long content.

My goal is simple: I do the hours of heavy lifting (stripping away the corporate jargon and complex tables) to hand you the pure signal.

Here is my full research on AVTECH, distilled into a 3-minute read that respects your time.

The Napkin Pitch (The Hook)

The One-Liner: AVTECH is a boring, profitable, debt-free Swedish microcap that sells software to airlines to help them save fuel and arrive on time—and once an airline plugs it in, they rarely unplug it.

The “Back of the Napkin” Thesis:

The “Invisible” Toll Booth: They embed software into the cockpit workflow that saves airlines millions in fuel; it’s mission-critical “sticky” revenue.

Fortress Balance Sheet: They have zero long-term debt and a massive pile of cash relative to their size (91.8% equity ratio).

The “Land and Expand” Play: They are already installed on 2,200 aircraft, but most aren’t using the full menu of tools yet—growth comes from simply upselling existing friends.

Microcap paradox: It’s too small for Wall Street to care about yet (MSEK 408 market cap), which is exactly why the opportunity exists.

The Lemonade Stand (Business Model)

Imagine a lemonade stand, but instead of lemonade, you sell a specialized GPS calculator to truck drivers that tells them exactly how to drive to save 2% on gas.

What they sell: AVTECH builds digital tools that help airplanes “talk” to air traffic control and pilots. Specifically, their software analyzes weather and flight paths in real-time to optimize flight profiles. This solves the three things that keep airline CEOs awake at night: high fuel costs, environmental emissions, and being late.

The Customer: Commercial airlines (like Wizz Air). These customers are massive, slow to make decisions, but incredibly loyal once they sign a contract.

How the cash enters the building: It is shifting to a subscription model (the “Holy Grail” of business). They measure success in Annual Recurring Revenue (ARR). As of Q4 2025, they have an ARR of 51.2 MSEK. This means they are moving away from one-time sales and toward “renting” their genius to airlines every month.

The Moat (Why They Win)

Why can’t a competitor just write some code and steal their lunch?

1. The “Don’t Touch It” Factor Aviation is a high-stakes game. Once an airline like Wizz Air integrates AVTECH into their safety and efficiency workflow, the cost and headache of ripping it out are massive. It becomes “mission-critical.” If the software saves them a fortune on fuel, removing it is literally burning money.

2. The Toothbrush Test Is this used daily? Yes. Every time a plane takes off, the pilot needs data to fly efficiently. AVTECH positions itself as the “pick and shovel” play—they don’t build the risky plane; they just make every flight 10% more profitable by existing.

3. The Upsell Runway They don’t need to hunt for new customers to grow. They are already on 2,200 planes. The moat is their existing footprint. They can double their revenue simply by convincing their current friends to buy the “Dessert Menu” (new modules launching this spring)

The Price Tag (Valuation)

Warning: This is a Microcap (tiny company). The stock price will swing wildly. Do not bet the farm.

We need to look at what you are paying for every dollar of cash this business generates. The market currently values the company at SEK 407.78m (approx. SEK 7.22 per share).

The “Cash is King” Discrepancy: On paper, they look reasonably priced (Earnings Yield of 4.17%). However, their actual cash flow is lower than their reported earnings because they are reinvesting heavily and some customers paid late.

What You Get For Your Money

1. The “Accounting” Price (P/E Ratio)

The Number: 23.99x

The Translation: You are paying roughly $24 for every $1 of reported profit. This is a “growth” multiple, not a bargain bin price. Investors are paying a premium because they expect the company to get significantly bigger in the next few years.

2. The “Theoretical” Interest Rate (Earnings Yield)

The Number: 4.17%

The Translation: If their accounting profits were paid out as cash today, this is the annual return you would get. It matches a decent high-yield savings account, but remember: you are taking stock market risk to get it.

3. The “Cash Payback” (Price-to-Operating-Cash-Flow)

The Number: ~33.7x (Calculated: Market Cap 408m / Operating Cash Flow 12.1m)

The Translation: Based on the SEK 12.1m operating cash flow, it would take roughly 33 years of current cash flow to pay back your purchase price. This looks expensive today, but if their cash flow grows as fast as their sales (38%), this number drops quickly.

The Cash Verdict: The stock is priced for growth. The market is paying a premium (24x earnings) because they see the sales growing 38% year-over-year. If that growth stops, this price tag is too high. If the growth continues and the cash flow catches up to the earnings, this could be cheap.

The Money (Financial Health)

This is where AVTECH shines. They are built like a bunker.

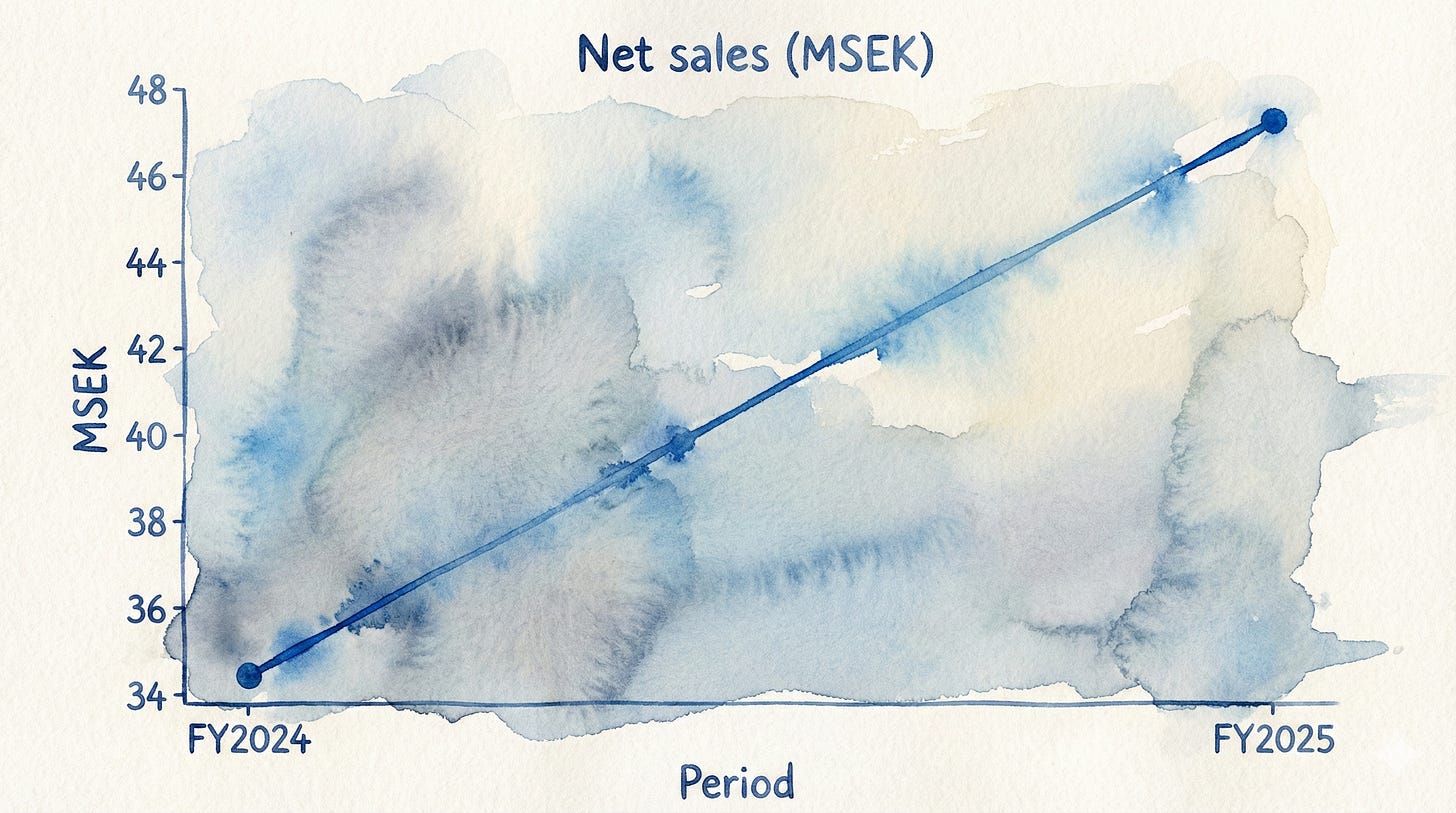

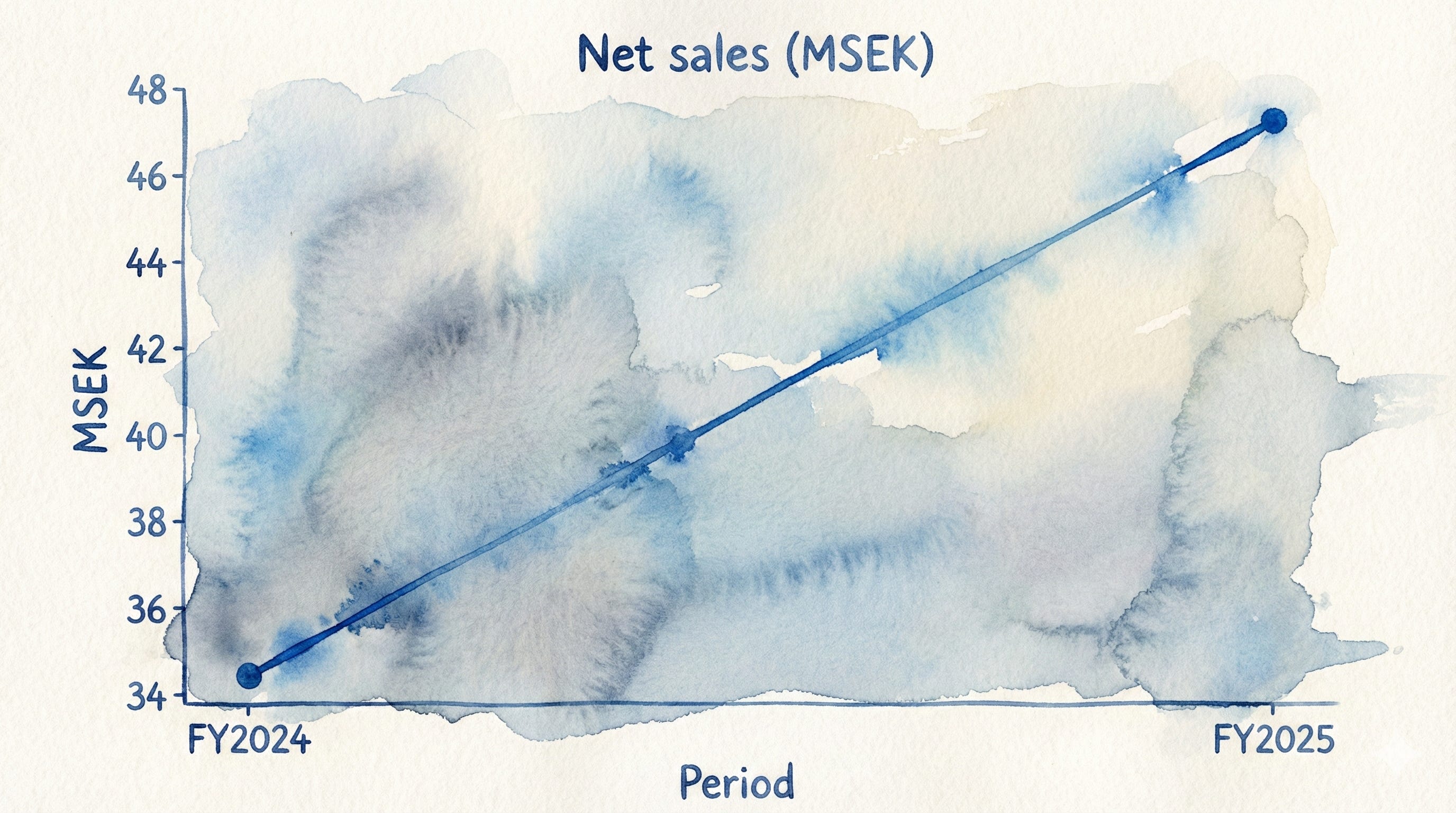

Profitability: They are printing accounting profits. Net sales jumped from 34.3 MSEK to 47.4 MSEK in one year. Net earnings rose to 17.0 MSEK. They have a “Rule of 40” score of 67.6% (Growth + Profit Margin), which is “Valedictorian” status in the software world.

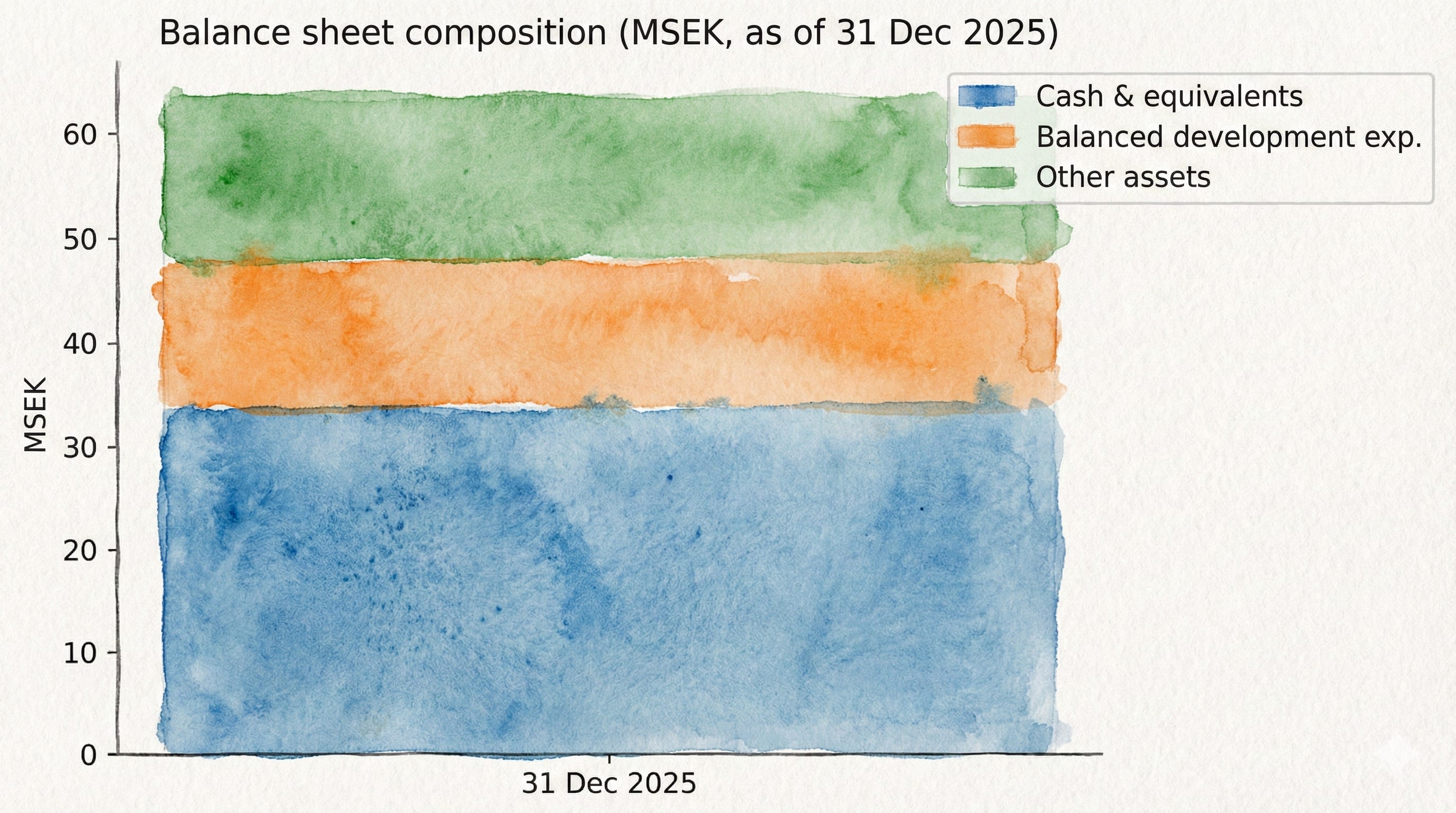

The Balance Sheet (Solvency): They have zero long-term debt and roughly 34 MSEK in cold hard cash sitting in the bank. Their equity ratio is 91.8%. This means they can survive a recession while their debt-heavy competitors go bust.

The “Lumpy” Cash Warning: While they reported 17 MSEK in profit, only 12.1 MSEK came in as Operating Cash Flow. Why? Two reasons:

Late Checks: Some customers haven’t paid their bills yet.

Investment: They are spending money on R&D and hiring people to fuel growth.

The Bear Case (Risks)

What could blow this up?

1. The “Paper Asset” Risk (The Kill Switch) This is technical but important. They have 14.1 MSEK in “balanced development expenses” on their balance sheet. This is money they spent on salaries to build software, but they counted it as an “asset” instead of an “expense.” If that software turns out to be useless and doesn’t sell, that asset vanishes, and their profits were an illusion.

2. The Waiting Game Selling to airlines is painfully slow. Decisions take forever. If the sales cycle drags out, the growth slows down, and that 24x P/E ratio will look very expensive very quickly.

3. Currency Gremlins They are a Swedish company selling globally. Fluctuations between the US Dollar and the Swedish Krona (SEK) can eat their profits. A weak dollar hurts them.

The Summary

I like this stock because it passes the “sanity test.” It has no debt, high margins, and a product that customers are afraid to turn off. It is a classic “picks and shovels” play on the aviation industry without the risk of actually owning airplanes.

It is currently in a transition phase—spending cash now to hire sales staff and build products for a massive payoff later. If the “ARR Staircase” keeps climbing past 51 MSEK, the current price is a steal.

There is a hidden catalyst launching this spring: new “Time” and “Dispatch” modules. If these upsells work, the company could see a massive spike in profit margins without finding a single new customer.

Do you enjoy complex Deep Dives distilled into a simple 3-minute read? ⏳

Do a friend (and me) a huge favor: Forward this to a busy investor who values quality over quantity.

Disclaimer:

I Am Not Your Financial Advisor: I am a researcher sharing my homework, not a wealth manager giving you a plan. This is for education, not a recommendation to buy or sell.

I Am Biased: I own AVTECH in my personal portfolio. I have skin in the game and I want this company to win. Read this with that in mind.

The Golden Rule: It is your money. Do your own due diligence, read the actual filings, and never invest money you cannot afford to lose.