The Titan Test: Would Dev Kantesaria Buy dLocal ($DLO) Today?

Can we apply Kantesaria’s rigid “Toll Booth” framework to a small-cap stock to find a monopoly before it becomes famous?

New to The Atomic Moat? This Titan Test of dLocal ($DLO) is a prime example of how we dissect high-quality compounders. If you want these ‘Titan Tests’ sent to your inbox, join 900+ other investors below.

I have long kept a collection of various Dev Kantesaria’s interviews in my notepad. His intellectual discipline is something I deeply admire; he doesn’t just beat the market, he ignores 95% of it, focusing exclusively on “inevitable” monopolies like Visa or Moody’s.

But you and I possess a distinct advantage over the giants of Valley Forge: agility.

While funds like Kantesaria’s must deploy billions, forcing them to hunt only among the largest, most efficient mega-caps, we are not so constrained. As retail investors, we can navigate the shallow waters where the whales cannot swim. We can buy the illiquid, the misunderstood, and the small.

This begs a lucrative question: Can we apply Kantesaria’s rigid “Toll Booth” framework to a small-cap stock to find a monopoly before it becomes famous?

Today, we run that experiment. We are taking the rigorous lens of Valley Forge and focusing it on a $3 billion emerging market fintech player: dLocal (DLO).

Does it pass the test? Let’s find out.

Pillar 1: The “Toll Booth” Test (Market Structure)

Kantesaria’s favorite holding is often the credit rating duopoly (S&P Global / Moody’s) or the payment rails (Visa / Mastercard). He loves them because they are Natural Monopolies. If you want to issue a bond or swipe a card, you must pay the toll.

Is dLocal a toll booth?

The Bull Case: dLocal describes itself as the “One dLocal” solution. They abstract away the messy complexity of emerging markets—managing hundreds of local payment methods like Pix in Brazil or Fawry in Egypt—so that a global merchant like Google or Bolt only needs one API.

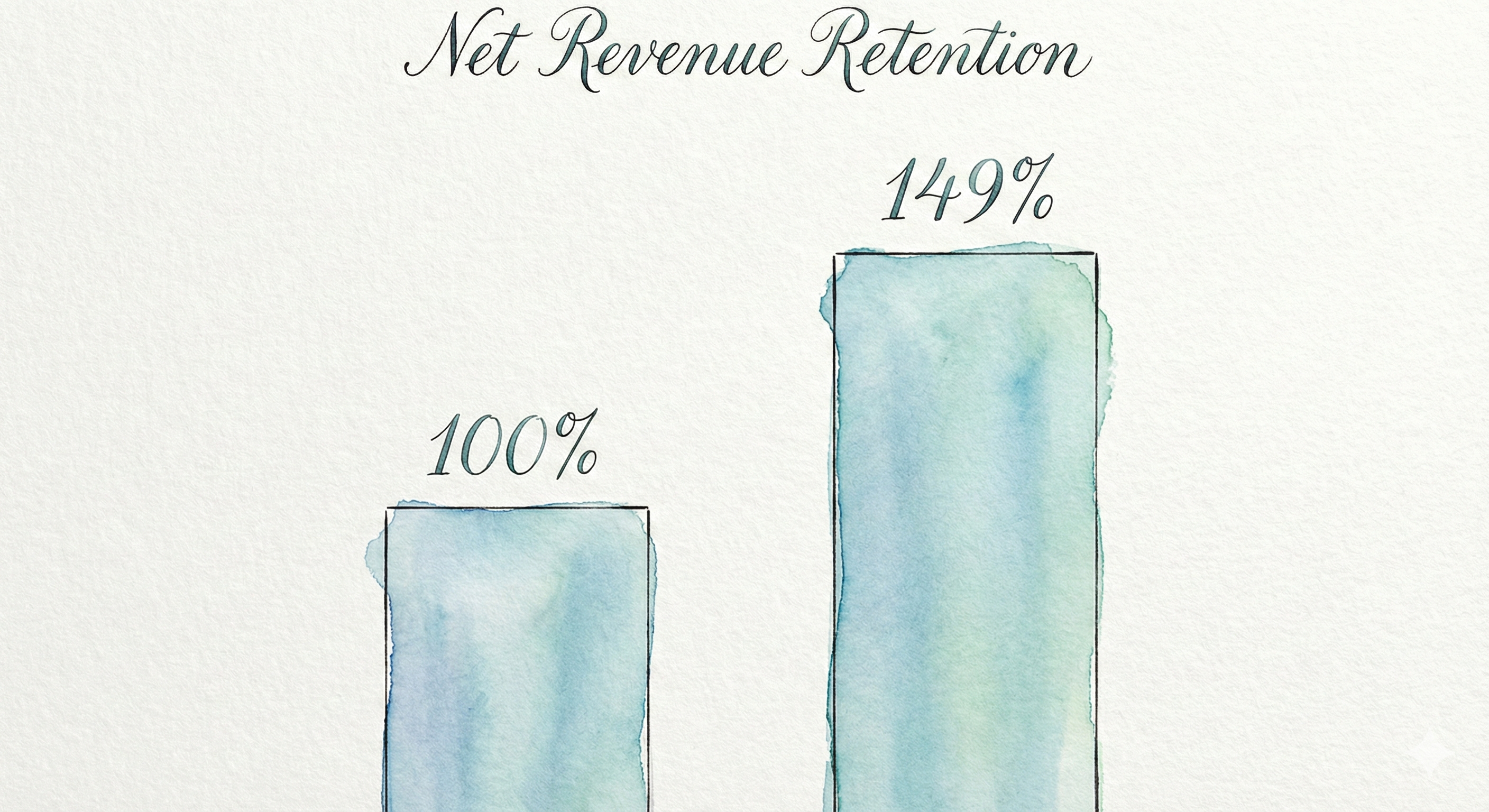

The evidence of “lock-in” is strong. Kantesaria looks for Net Revenue Retention (NRR) as a proxy for how indispensable a product is. dLocal reported a staggering 149% NRR in Q3 2025. This means that even without adding new clients, their existing customers (cohorts) are spending 49% more with them year-over-year. That is the kind of “sticky” compounding Kantesaria craves.

The Kantesaria Critique: However, dLocal is not a monopoly. It is an Aggregator, not a Network. In Brazil, dLocal processes Pix payments, but they don’t own Pix. In Egypt, they process cards, but they don’t own the rails. They are a layer on top.

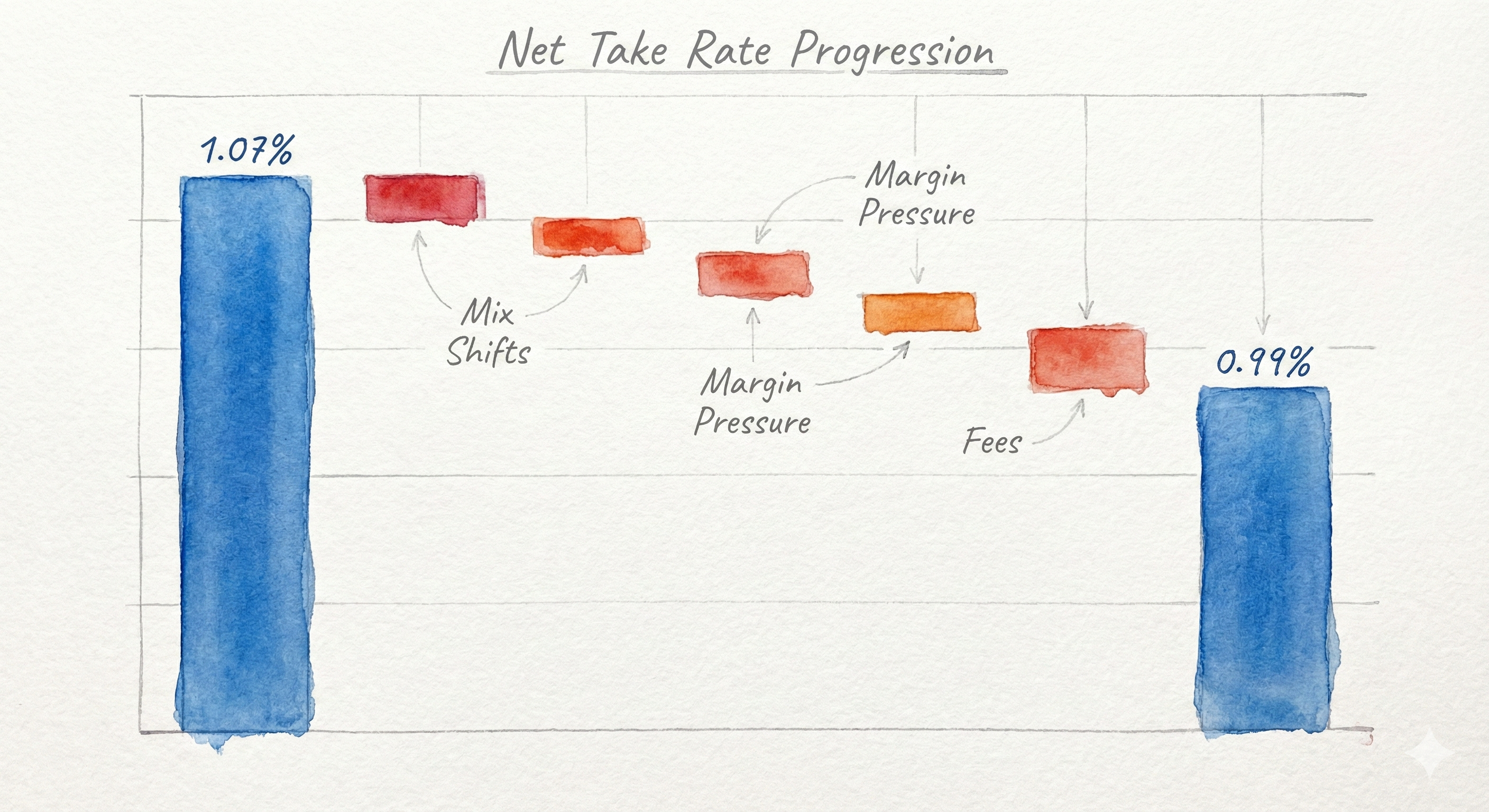

Furthermore, the “toll” is under pressure. dLocal’s management admitted that their net take rate (the % they keep of every dollar) was down sequentially in Q3. This was driven by mix shifts and “temporary margin pressure” in Mexico.

Kantesaria defines pricing power as the ability to raise prices 3–4% annually. If dLocal’s take rate is compressing due to “aggressive discounting by competitors” (a risk explicitly flagged in their guidance ), it fails the primary Kantesaria test. A true monopoly doesn’t discount.

Pillar 2: The Capital Intensity Filter

Kantesaria avoids businesses that must burn cash to grow (like airlines or factories). He demands High Return on Invested Capital (ROIC) and 100% Free Cash Flow (FCF) conversion. He wants a business that grows purely on intellectual property, not steel and concrete.

The Financials: dLocal shines here initially. It is an asset-light software business.

Gross Profit: $103 million (up 32% YoY).

Adjusted EBITDA Margin: A robust 70% of Gross Profit.

Revenue per Employee: This metric improved sequentially, showing operating leverage.

Kantesaria loves when a company grows revenue ($282M, up 52% YoY ) faster than its headcount costs.

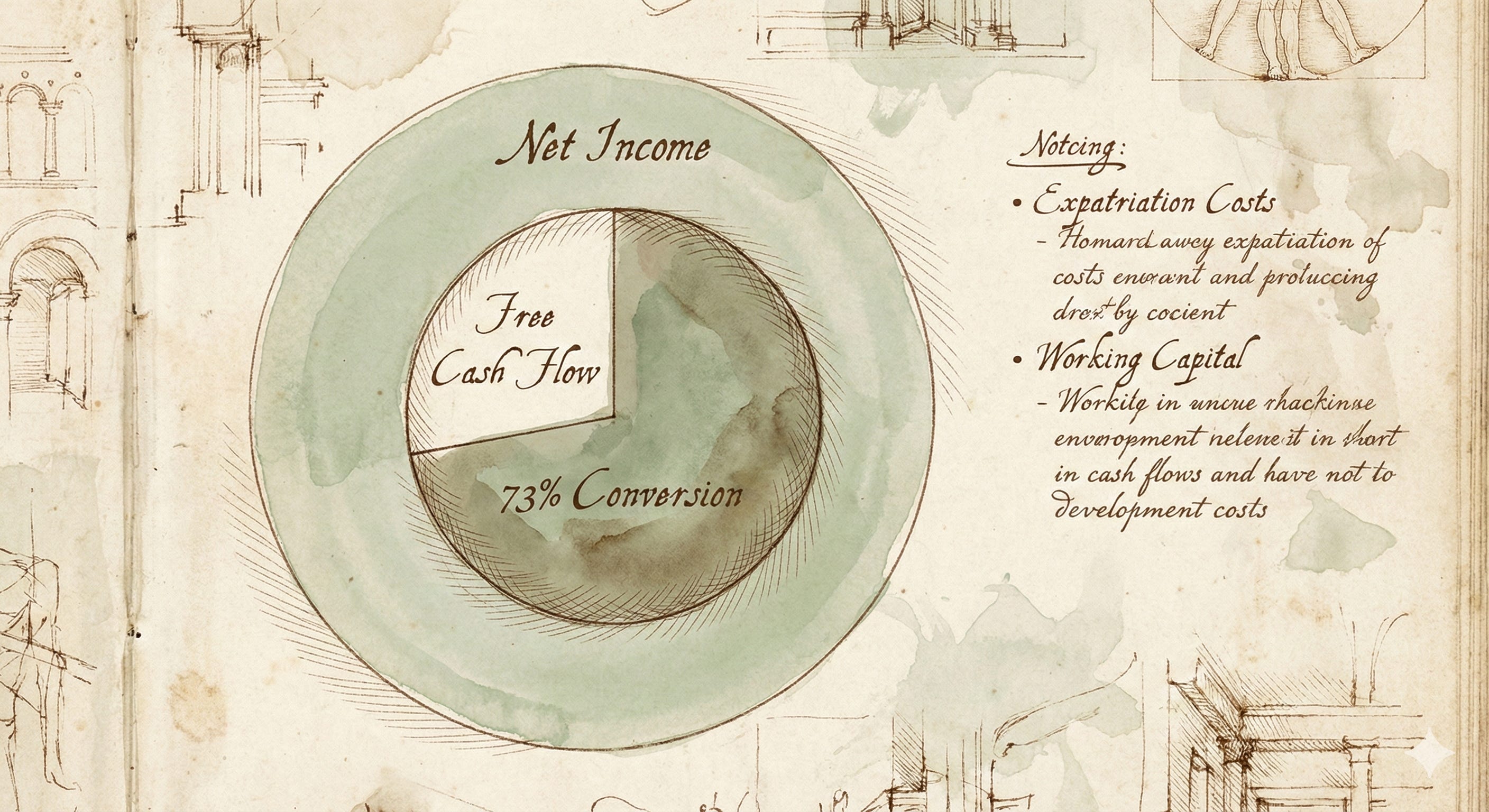

The Cash Flow “Leak”: However, the “100% FCF Conversion” metric hit a snag. In Q3 2025, dLocal’s Adjusted Free Cash Flow conversion to Net Income dropped to 73%.

Why? Because of the reality of operating in volatile emerging markets. The company faced a $13M impact related to “structuring used to expatriate flows from Argentina”.

Kantesaria views “expatriation costs” and “inflation adjustments” as unnecessary friction. He wants a clean machine. A company that has to construct complex financial vehicles just to get its own cash out of a country (Argentina) introduces a layer of operational risk that Mastercard (mostly) avoids.

Pillar 3: Predictability vs. The “Macro” Excuse

Perhaps the most rigid filter in the Valley Forge philosophy is Predictability. Kantesaria avoids cyclical industries because he wants to hold a stock for 20 years without sweating the headlines.

dLocal’s Q3 2025 report is filled with what Kantesaria would call “noise”:

Currency Devaluation: Revenues in Egypt were hit by a devaluation.

Political Risk: New tariffs in Mexico slowed down TPV (Total Payment Volume).

Inflation Accounting: The company has to apply “IAS 29” inflation adjustments for Argentina, which distorts the P&L.

Management reiterated guidance, expecting TPV to exceed the high end of their range. The growth is undeniable—Total Payment Volume hit a record $10.4 billion, up 59% YoY.

But Kantesaria doesn’t buy growth; he buys certainty. He would look at the “Key Risks” slide (which lists currency devaluations in Egypt and Bolivia, fiscal regime changes in Brazil, and tariff wars) and likely conclude that the external variables are too high.

He prefers businesses where the only variable is “how many people used the product,” not “what is the inflation rate in Buenos Aires today?”

The Verdict

Applying the strict, “old money” discipline of Dev Kantesaria to dLocal (DLO):

Status: Pass (Keep Watching)

The Titan’s Reasoning: dLocal is an exceptional Growth company, but it is not yet a Valley Forge company.

Quality: The NRR of 149% is world-class. It proves the service is essential. Kantesaria would respect the “stickiness.”

Valuation/Capital: It is capital-light and profitable, fitting the financial model.

The Dealbreaker: It lacks Pricing Power and Predictability. Kantesaria invests in “monopolies in plain sight” that act as toll booths on the global economy. dLocal is currently fighting a war on multiple fronts—battling competitors on price (take rate compression) and battling governments on macro-economics (Argentina/Egypt).

Kantesaria is willing to pay a premium for a company that controls its own destiny (like FICO). dLocal, despite its brilliance, is still at the mercy of Emerging Market central banks and tariffs.

Final Thought for the Long-Term Investor: If you have a higher risk tolerance than Kantesaria, dLocal’s 59% volume growth is intoxicating. But if you are building a “sleep well at night” portfolio, dLocal has not yet dug a wide enough moat to keep the macro-economic storms at bay.

Compounding requires a smooth runway. Currently, dLocal is taking off on a gravel road.

Disclaimer

Not Financial Advice: The content provided in “The Atomic Moat” and “The Titan Test” is for informational and educational purposes only. It represents the opinions of the author and should not be construed as professional financial, legal, or tax advice. We are analyzing businesses, not providing personal investment recommendations.

Do Your Own Research: Financial markets are inherently risky. The strategies and frameworks discussed (including those of Dev Kantesaria) may not be suitable for your specific risk tolerance or time horizon. Always conduct your own due diligence or consult with a licensed financial advisor before making any investment decisions.

No Guarantees: Past performance is not indicative of future results. The numbers, figures, and “falsifiers” presented are based on current data and management guidance, which are subject to change without notice.