A boring monopolist Mr. Market decided to panic about

A 78% EBITDA margin. A 50% stock decline. One very confused market.

I want to start by telling you a story.

In 1973, Warren Buffett bought a controlling stake in The Washington Post Company. The market valued the whole business at around $80m. Buffett thought it was worth $400m. He was not being clever. He was just reading the business correctly while everyone else was reading the stock price.

What made Washington Post worth $400m was not the journalism. It was the classifieds: Job listings. Apartment listings. Car listings. Every employer, landlord, and car dealer in the Washington metropolitan area had one place to reach buyers, and that place was the Post.

They had no real alternative, and they knew it. The Post raised its rates every year. So they kept paying. The economics were, as Buffett later put it, like owning an unregulated toll bridge.

Pricing: The Atomic Moat

Premium members pay $199 per annum. With this membership, you will get access to all my curated watchlists and fat-pitch triggers, which will save you a lot of time and work. You will also get access to my current portfolio, deep dives, and much more.

Buffett held that position for decades. It became one of the most celebrated investments in history.

Here is what I find interesting: The same flywheel that made Washington Post’s classifieds extraordinary now runs on the internet, in markets where one digital platform has won so completely that competition has effectively stopped trying.

Baltic Classifieds Group is not The Washington Post. I want to be clear about that. Buffett bought Washington Post at roughly twenty cents on the dollar during a full market panic. BCG today is a fair price for a good business, not an absurd discount to obvious value.

The degree of cheapness is completely different.

But the structure of the moat is the same. Same type of business. Same type of professional dependency. Same type of pricing power. Same type of local dominance that looks boring from the outside until you understand why nobody can compete with it.

Buffett understood something in 1973 about classifieds franchises that most investors still miss today. BCG is the same insight, fifty years later, in digital form. The question worth asking is whether the market currently understands what it owns.

I think it does not. Here is why.

Baltic Classifieds Group is a small company in Northern Europe that most investors have never heard of, charging brokers, car dealers, and job recruiters a modest monthly fee to exist professionally online.

The brokers pay. The dealers pay. The recruiters pay.

And because everyone pays, everyone lists their properties, cars, and jobs on BCG’s websites. And because everything is listed there, anyone in Lithuania, Estonia, or Latvia who needs to buy or sell something significant goes there too.

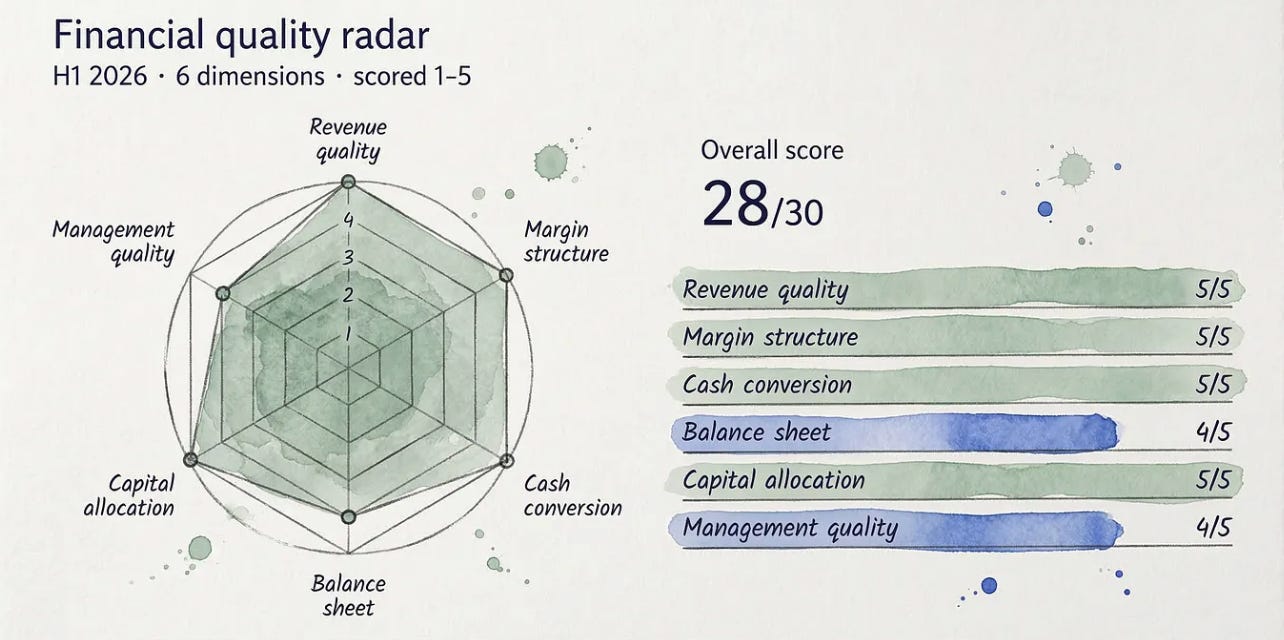

Fourteen websites. Six million people. A 78% EBITDA margin.

Yup, 78%.

Sit with that for a second. Apple, one of the most profitable companies in the history of capitalism, runs at around 33%. BCG runs at 78% on a portfolio of classifieds websites in a corner of Europe most investors could not find on a map.

First, understand what this business actually is

A classifieds business is a middleman that connects buyers and sellers. Bah! That description makes it sound… ordinary.

It is not.

The thing that makes classifieds businesses extraordinary is what happens once they get big enough.

Think about it from a seller’s perspective. If you are a Lithuanian trying to sell your apartment, you want to list it where the most buyers are looking. And if you are a buyer looking for an apartment in Vilnius, you go to whichever website has the most listings. The seller follows the buyers. The buyers follow the listings. The listings attract more buyers. The buyers attract more listings.

This is a flywheel, and once it gets spinning it is almost impossible to stop. The market leader gets more listings because it has more buyers. It gets more buyers because it has more listings. Everyone else gets the scraps.

BCG has been spinning this flywheel since 1999. Its real estate portal in Lithuania now leads the nearest competitor by 48 times on time spent on site. Its auto portal in Estonia leads by 31 times. These numbers are not the result of clever marketing. They are the mathematical consequence of a flywheel that has been running for twenty-five years.

Peter Lynch used to say the best businesses are the ones you can explain in a sentence.

Here is BCG in one:

It owns the only relevant classifieds platforms in three small countries, and because it owns the only relevant platforms, nobody can afford not to use it.

Now understand why the margins are what they are

BCG is not profitable because it is efficient. It is profitable because of what kind of business it is.

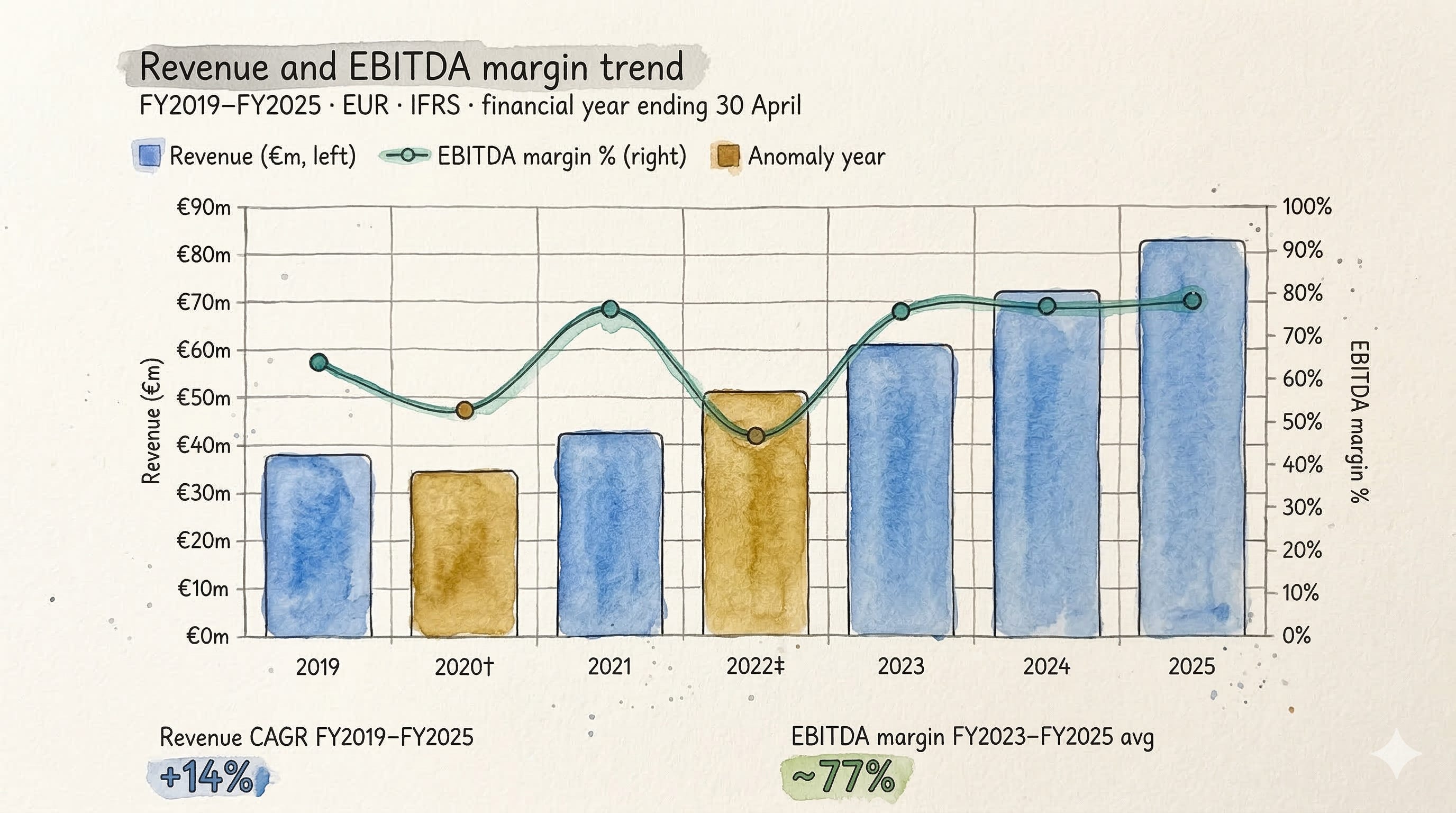

In the six months ended October 2025, BCG collected €44.8m in revenue. It spent €9.7m running the operation: salaries for 153 people, some third-party IT, modest marketing, a small amount of data costs. The remaining €35.2m was EBITDA.

Here is why it stays there: When BCG wants to grow, it does not build a factory. It does not hire a thousand new salespeople. It raises prices and ships product features.

The cost of serving one more broker, one more dealer, one more private seller is close to zero. There are no physical goods to produce, no delivery infrastructure, no inventory to finance. The platform exists. Adding more users to it costs almost nothing.

Capital investment for the half-year was €0.4m. Not €4m. Not €40m.

€0.4m.

Buffett has a word for businesses like this. He calls them toll roads. You want to cross the bridge, you pay the toll. BCG is the only bridge, so everyone pays.

And unlike a real toll road, BCG never needs to repave the asphalt.

Okay, so why is the stock down 50% from its peak?

Well, the short and sweet answer is: Estonia taxed car ownership.

In December 2024 the Estonian government introduced a vehicle transaction and ownership tax. Car transactions in Estonia promptly collapsed, falling between 45% and 66% every single month through 2025 compared to the year before.

Fewer car sales meant fewer private sellers listing cars on BCG’s Auto24.ee platform. Auto listing volumes fell 29%. The market looked at the numbers, saw a business where the largest segment appeared to be in freefall, and sold.

Here is what it missed. Auto segment revenue for the six months ended October 2025 was €16.0m. Exactly flat with the prior year. Not down. Flat.

How? Professional car dealers pay BCG a monthly subscription regardless of whether anyone is buying cars that month. And the private sellers who still needed to sell had nowhere else to go, so they kept listing, paying BCG’s higher per-listing prices as the company continued its annual yield increases. The volume collapse and the pricing increase cancelled each other out almost perfectly.

I find this genuinely fascinating. A government policy that halved the car transaction market in an entire country, and BCG’s Auto revenue did not move. That is what a real moat looks like. Not in a PowerPoint. In the actual numbers.

There is also a comparison problem making everything look worse than it is. H1 2025 was peak inventory across BCG’s platforms, the best comparable the company has ever produced. A 29% decline in listings against a record comparable looks catastrophic.

Against the actual number of listings on the platform today, it is a policy-specific correction in one country. Management has confirmed year-on-year Auto growth is expected to resume from January 2026. Not because Estonians suddenly start buying cars again in volume, but because you are now comparing against the already-collapsed numbers from a year ago.

The tax stays. The comparison distortion does not.

The bear case deserves a fair hearing

BCG serves six million people. That is pretty much the ceiling, and it is not going up a lot more. The growth of recent years has come almost entirely from raising prices on existing users and converting free users to paid tiers.

Both are finite. At some point the broker paying €238 a month says no. At some point the private seller decides €9 to list a used sofa is not worth it.

Facebook Marketplace is the name that comes up most often in the competitive risk discussion. If Meta decided to offer free listings across Lithuania, Estonia, and Latvia, BCG’s inventory advantage could erode faster than the financials suggest. It has happened in other small markets.

And regulation is a genuine concern. BCG is a functional monopolist in several verticals. The Estonian Competition Authority has active enquiries open. Raising prices every year on customers who have no real alternative is exactly the profile that attracts antitrust attention.

These risks are real. Anyone who tells you otherwise is not being straight with you.

But here is where the bear case runs into a problem

A real estate broker in Vilnius does not use Aruodas.lt because it has the most listings. She uses it because her entire professional life runs through it: her active listings, her client inquiries, her pricing data, the tools she uses to advise sellers.

Two years ago BCG introduced Property Price Compass, which pulls actual transaction data from the national land registry, connects it to listing history, and produces a professional pricing report she can hand to a vendor with her own name on it.

Her clients now expect that report at the first meeting.

Try to compete with that. You are not competing with a website. You are competing with a workflow embedded in thousands of professional relationships built over years.

The moat in plain language

BCG does not just host listings. It runs the professional workflow of every broker, dealer, and recruiter in its markets. Switching costs are not about price; they are about rebuilding years of embedded client relationships from scratch.

Car dealers use Autopulsas to track real-time market dynamics for specific models. Recruitment companies use CVbankas to access a salary estimator trained on a decade of job offers and CVs that no new entrant could replicate.

BCG has spent years quietly converting listing services into professional tools, and professional tools are a completely different proposition to a website with listings on it.

Facebook Marketplace can offer free listings to private sellers. It cannot replace the morning routine of a car dealer checking Autopulsas before he prices his inventory. The segment most exposed to free-listing competition, generalist C2C, is 15% of BCG’s revenue. The professional segments are protected by something that compounds with every year BCG operates.

Lynch called it a moat. Munger called it the nature of the business. Buffett called it pricing power. They were all describing the same thing:

A business that gets harder to displace over time, not easier.

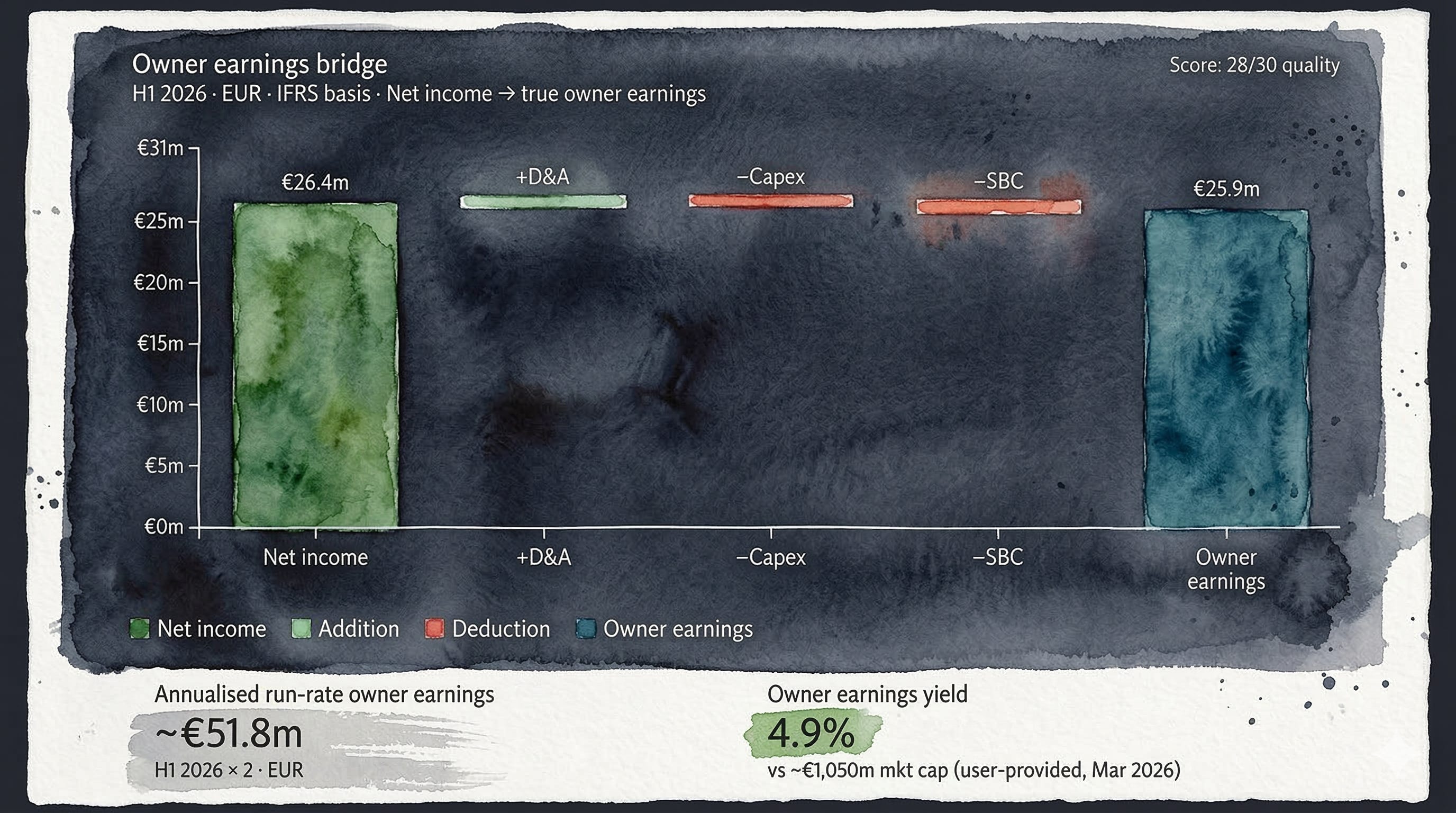

The financials, laid out plainly

Strip out stock compensation as the real cost it is, net out the minimal capital requirements, and owner earnings come to roughly €52m annualised. Against an enterprise value (EV) of approximately €1.05bn, that is a 4.9% yield on a business moving to zero debt with 99% cash conversion.

At 4.9% you are paying what I would say is a fair price for a good business. The argument for owning BCG is not that it is mispriced in a screaming obvious way, even after a nearly 50% drop.

No, the argument is that a genuinely dominant franchise has been de-rated by a policy shock that is already reversing, that B2C price increases from October 2025 have not yet fully landed in the reported numbers.

And that a well-run, debt-free company with €60m of annual cash flow and an £880m market cap is about to have a very interesting capital return conversation with its shareholders.

Management outlook · H1 2026 half-year report

“Despite record inventory comparables, and challenges in the Estonian auto market, we expect revenue growth for the second half of the year will be above that of H1 and will accelerate into double digits for FY2027.”

BCG management · December 2025

Management has said the company could be debt-free by April 2026. When that happens, the capital allocation question becomes very simple.

The base case, Estonian comparables normalising through H2 2026 and the pricing tailwinds feeding through, gets you to around 220p. Roughly 15% from here. The bull case, where product deepening drives yield growth above what management has guided, reaches closer to 280p. Neither requires heroics.

The question I keep coming back to is what would have to be true for the pessimists to be right. BCG’s pricing power would need to be more fragile than three consecutive years of evidence suggests, or a competitor would need to successfully attack the professional workflow layer rather than just the listing layer, or a regulator would need to act.

None of that is in the data right now. But this is exactly the kind of thesis where monitoring matters more than the initial call.

The two things I watch are simple:

First, Auto and Real Estate C2C active ad volumes: if they start declining for multiple consecutive quarters without a named policy cause, that is the early signal that something structural is happening to inventory depth.

Second, any formal announcement from the Baltic competition authorities specifically targeting BCG’s B2C pricing practices.

I am currently working on a platform for investors who think in businesses, not tickers. It’s the place to write your thesis, track what actually matters about the companies you own, and build a research trail that compounds alongside your portfolio. More on this very soon.

What is in the data is a business that absorbed a 50% collapse in car transactions in its second-largest market, held Auto revenue flat, grew Real Estate by 20%, and maintained a 78% EBITDA margin throughout. It ended the period in net cash for the first time.

Fifty percent de-rating. Seventy-eight percent margin. Two very different numbers telling two very different stories about this company.

I know which one I trust.

Disclaimer

This is not financial advice. Nothing in this post constitutes a recommendation to buy, sell, or hold any security. I am not a financial advisor, and Atomic Moat is not an investment advisory service.

Everything here reflects my own research, analysis, and opinions at the time of writing. I can be wrong — and when I am, I’ll say so.

I may hold a position in companies I write about. Where that is the case, I will disclose it. At the time of publishing this piece, I do not hold a position in Baltic Classifieds Group (BCG.L).

Do your own research. Use this as a starting point, not a conclusion. The goal of Atomic Moat has always been to help you build your own process; not to replace it.