Three Trillion Dollars of IPO Hype Is Coming. I'd Wait.

SpaceX, OpenAI, and Anthropic are about to go public. The hype is real. The companies are real. But I would listen to Charlie and Warren first.

Every IPO, at its core, is a theatrical performance.

There is a script. There is a cast. There are producers who have been working behind the scenes for years. And then there is an opening night, when the curtain finally rises and the audience, that’s you, buys a ticket at the box office and takes a seat in the dark.

What I find fascinating, and what I think most coverage gets badly wrong, is that nobody tells you that by the time you walk through the doors, everyone who actually matters has already seen the dress rehearsal. The critics got advance screenings. The investors who will make the most money were in the room when the script was still being written.

You? You’re buying a ticket on opening night. At full price. From the box office. For a show the cast is very motivated to sell you.

The IPO process is structurally tilted away from you.

And right now, with SpaceX, OpenAI, and Anthropic all about to hit public markets within months of each other, I think it’s worth sitting down and talking through exactly what kind of theatre you’re about to walk into.

First, Let’s Talk About What’s on the Marquee

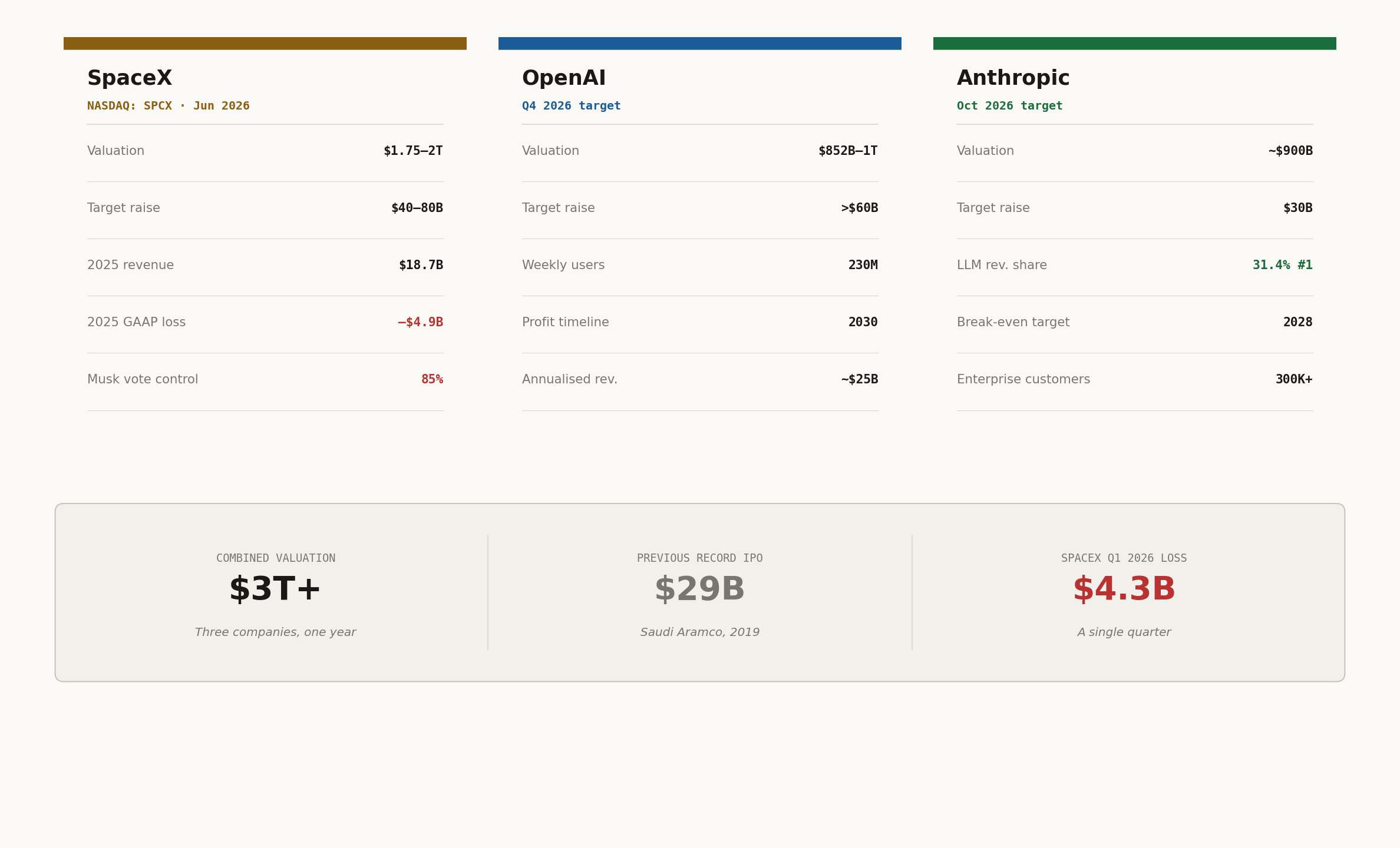

On May 20, 2026, SpaceX filed its IPO prospectus with the SEC. The company is expected to trade on Nasdaq under the ticker SPCX, with trading possible as early as June 12, depending on the final roadshow and pricing process.

The reported valuation target is around $1.75 trillion. On listing day, that would not quite put SpaceX beside Apple, Microsoft and Nvidia at the very top of the market, but it would put it in a ridiculous neighbourhood: potentially the seventh-most valuable public company in America.

To put that in perspective: the entire global IPO market raised $42.6 billion in Q1 2026. Even if these companies only sell a small slice of themselves, the proceeds could dwarf what the normal IPO market does in an ordinary quarter.

Then comes OpenAI, the company behind ChatGPT, a product now used by more than 900 million people every week. It is reportedly preparing for a possible public listing as early as September.

Then Anthropic, the makers of Claude, which is also reportedly circling the public markets with valuation talk somewhere near the trillion-dollar edge.

Put the three together and, if the reported targets hold, you are looking at well over $3 trillion in market value trying to enter public markets in less than a year.

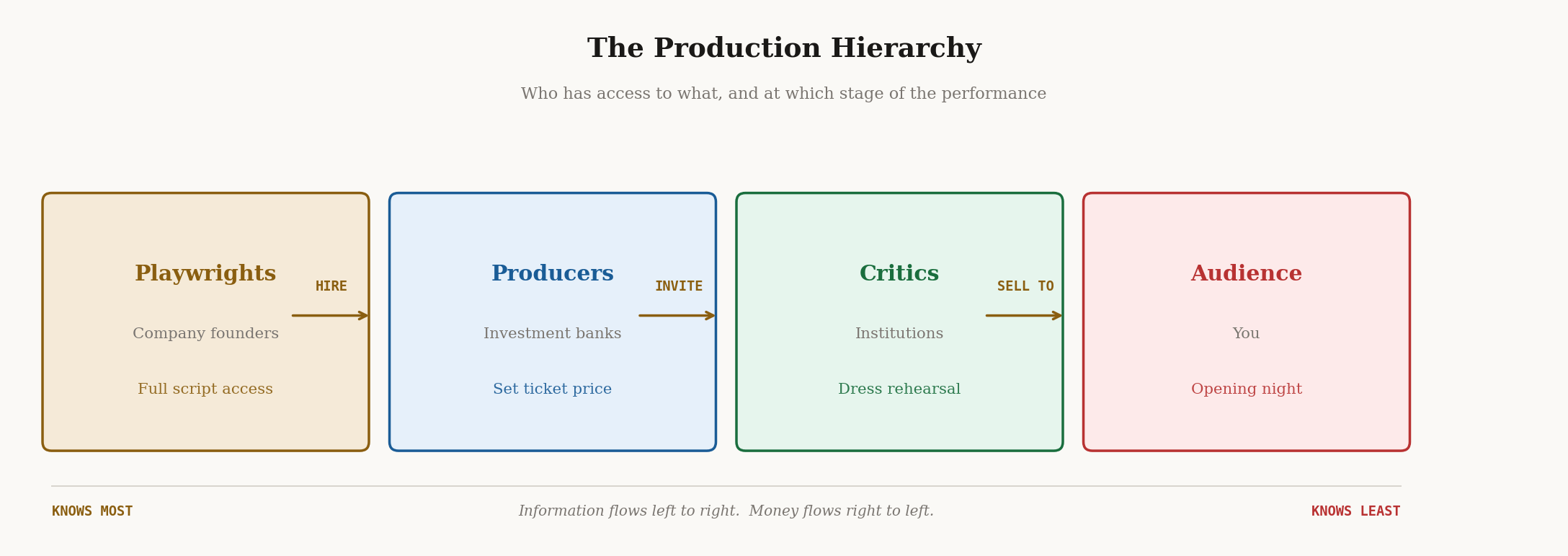

The Production You’re Joining (And Who Runs It)

Here is how an IPO actually works:

A private company, let’s use SpaceX as our example, hires investment banks. Goldman Sachs. Morgan Stanley. You know, the usual names.

These banks take the company on a “roadshow,” which is the industry’s polite word for a travelling sales performance. The “cast and producers” sit across from the world’s largest pension funds, sovereign wealth funds, and hedge funds. Together, they set the price. Together, they decide who gets seats.

Then the stock lists on an exchange, and you, an individual investor sitting at home, get to buy whatever’s left in the general admission section.

Ask yourself honestly: at which point in that production do you think the pricing most favors the general audience?

“Anytime anybody offers you anything with a big commission and a 200-page prospectus, don’t buy it. Occasionally, you’ll be wrong if you adopt Munger’s Rule. However, over a lifetime, you’ll be a long way ahead, and you will miss a lot of unhappy experiences.”

Charlie Munger, Vice Chairman, Berkshire Hathaway

A SpaceX S-1 prospectus is, almost to the letter, that 200-page programme. And much like a real theatre programme, it was written by the production’s own lawyers, it tells you what they want you to know, and it costs you nothing because the real price comes later.

The company and its bankers choose the exact moment to go public. They pick the moment most favorable to them: when sentiment is high, when the story is cleanest, when the numbers look best. They do not ring a bell and announce that now would be a great time for retail investors to buy their shares at a fair price.

The curtain goes up when the production company is ready. Full stop.

What the Historical Reviews Actually Say

Alright, let’s talk data, because the data is fascinating and I find it consistently ignored in the excitement around big IPOs.

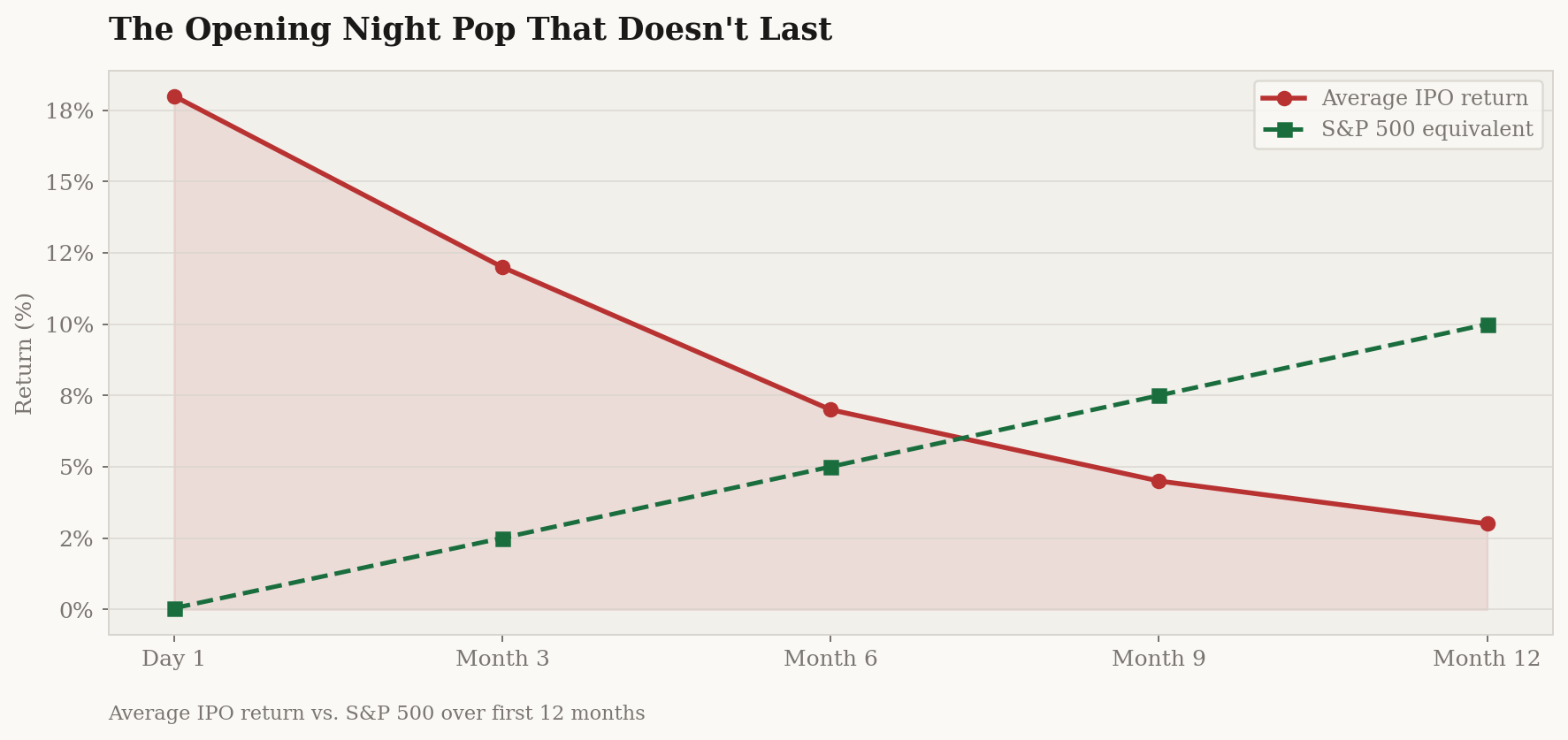

Academic research on IPOs has found the same uncomfortable pattern, over and over: the opening-night applause is often much better than the long run.

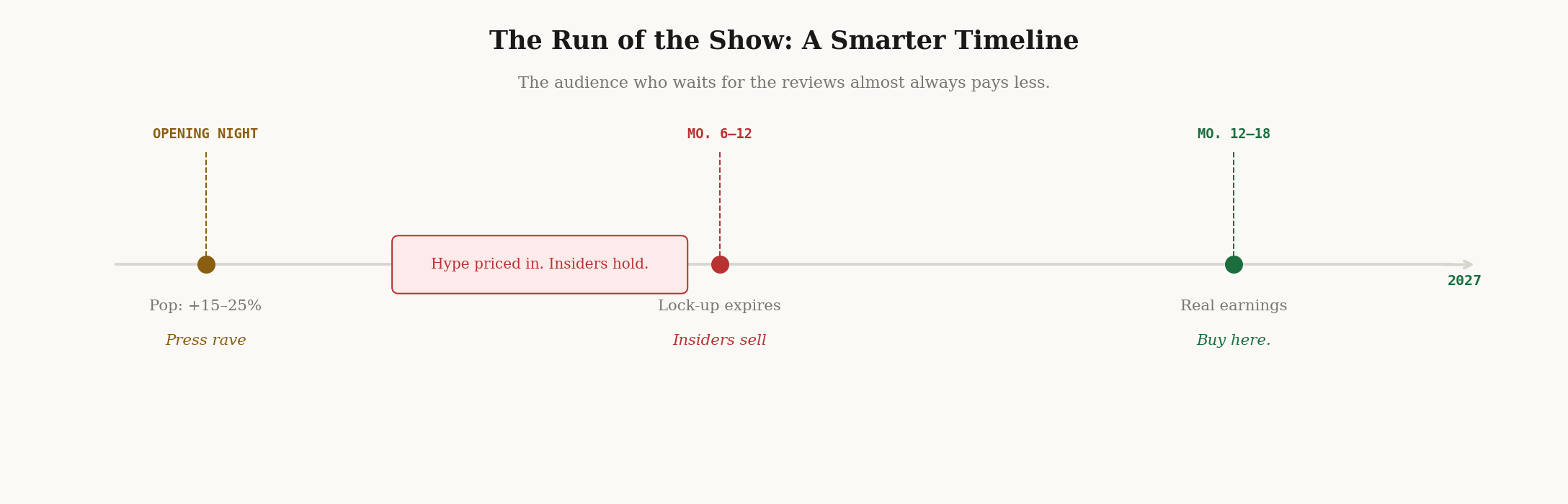

The first-day pop, that exciting percentage you see on the news, has historically averaged somewhere around the high teens. That is the part everyone talks about. That is the champagne. That is the photo outside the theatre.

But over longer periods, IPOs as a group have tended to disappoint against the boring old market index sitting quietly in the background.

I think about this the way critics talk about opening-night reviews versus the longer run. Shows get standing ovations on opening night all the time. It takes a few weeks to know whether it’s actually any good.

Here is the detail that really stings. The opening-night pop that makes the headlines? The one you see screaming across financial Twitter at 9:35am? I want you to understand that you almost certainly cannot access it at that price.

The best IPO allocations, the shares sold at the official offering price before the market opens, are reserved for the banks’ most valuable institutional clients. Research has shown this clearly: the IPOs with poor opening-night performance are easy to get allocations for. The ones with strong performance are quietly distributed to hedge funds and pension managers before retail investors can act.

By the time you see the pop, you’re watching a performance that opened without you. The people selling into that excitement are the ones who got in at dress rehearsal. They’ve already seen the show. They’re selling you their seats on the way out.

“I think buying new offerings during hot periods in the market is not anything that the average person should think about at all.”

Warren Buffett, Chairman, Berkshire Hathaway

Buffett has missed Amazon. He’s missed Google. He acknowledges both. His view is that owning great companies is one of the best things you can do with money. The IPO moment specifically is when the structural odds tilt hardest against the retail investor, and he has simply refused to play on those terms for seventy years.

It’s hard to argue with seventy years.

Now Let’s Read SpaceX’s Programme

Here is where I have to be honest: SpaceX is a legitimately extraordinary company.

It has done things that were supposed to be impossible. Reusable orbital rockets. The largest satellite constellation in human history. NASA contracts that previously went to companies ten times its size. The Falcon 9 launch cadence is something the aerospace industry still struggles to comprehend.

The S-1 reveals, for the first time, what the production actually looks like backstage. And backstage tells two very different stories.

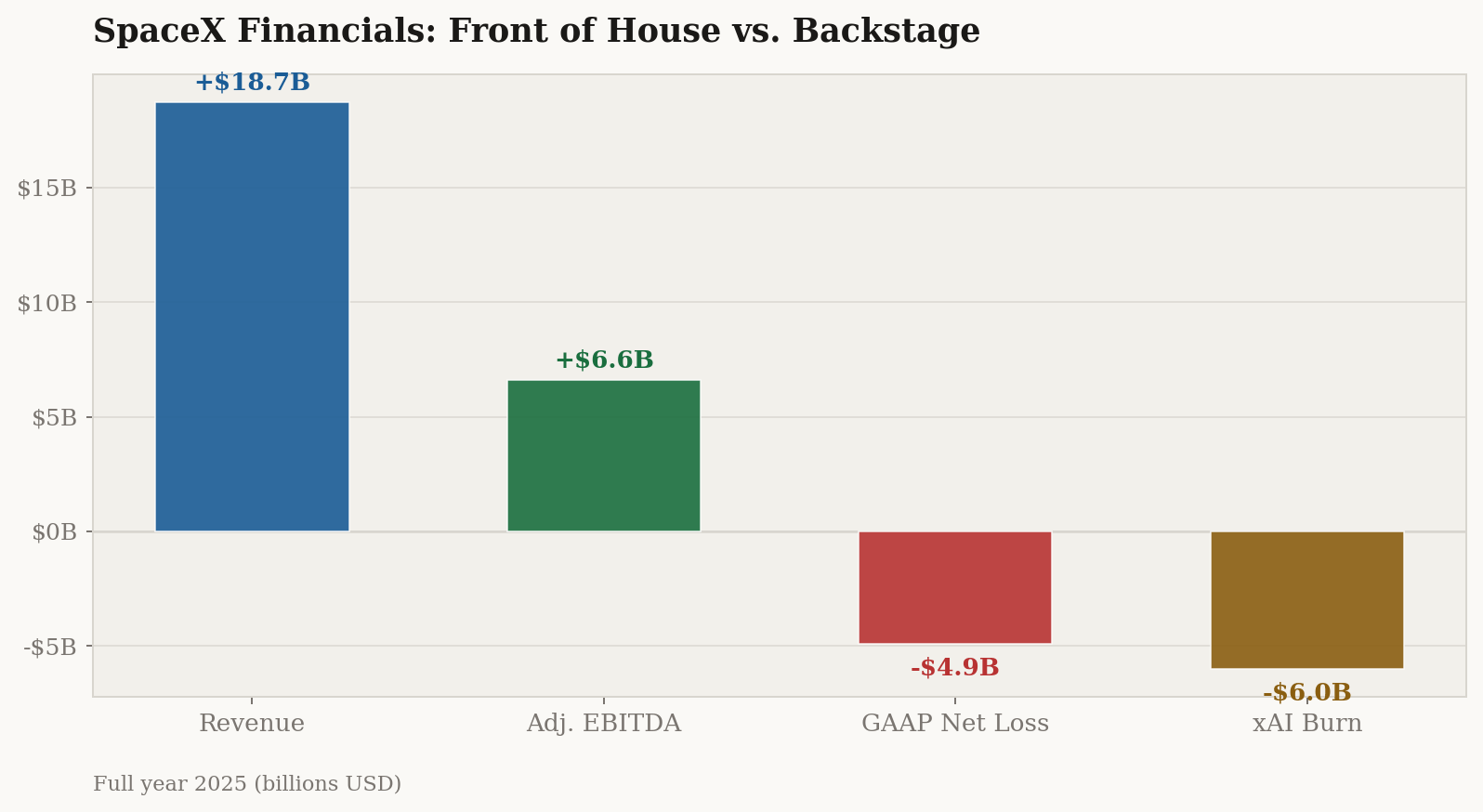

The front-of-house story: SpaceX generated $18.7 billion in revenue in 2025, up sharply from the year before. On an adjusted EBITDA basis, the company produced about $6.6 billion in profit. Starlink, its satellite internet division, is a dominant machine in low-earth-orbit broadband, serving parts of the world that traditional networks either cannot reach or cannot reach profitably.

The backstage story: despite that adjusted profit, SpaceX posted a GAAP net loss of about $4.9 billion for full-year 2025. And in Q1 2026 alone, it lost roughly $4.3 billion.

That gap between “adjusted EBITDA profit” and “actual loss” is not a rounding error. It is the show behind the show: depreciation, stock-based compensation, enormous capital spending, and, most unusually, the cost of folding Elon Musk’s AI empire into the SpaceX story.

Let that sit for a moment. When you buy SpaceX, you are not only buying Falcon 9, Starship and Starlink. You are also buying exposure to Grok, X, and Musk’s attempt to build an AI platform that competes, in one way or another, with the other two productions coming to market: OpenAI and Anthropic.

It makes the investment considerably harder to explain.

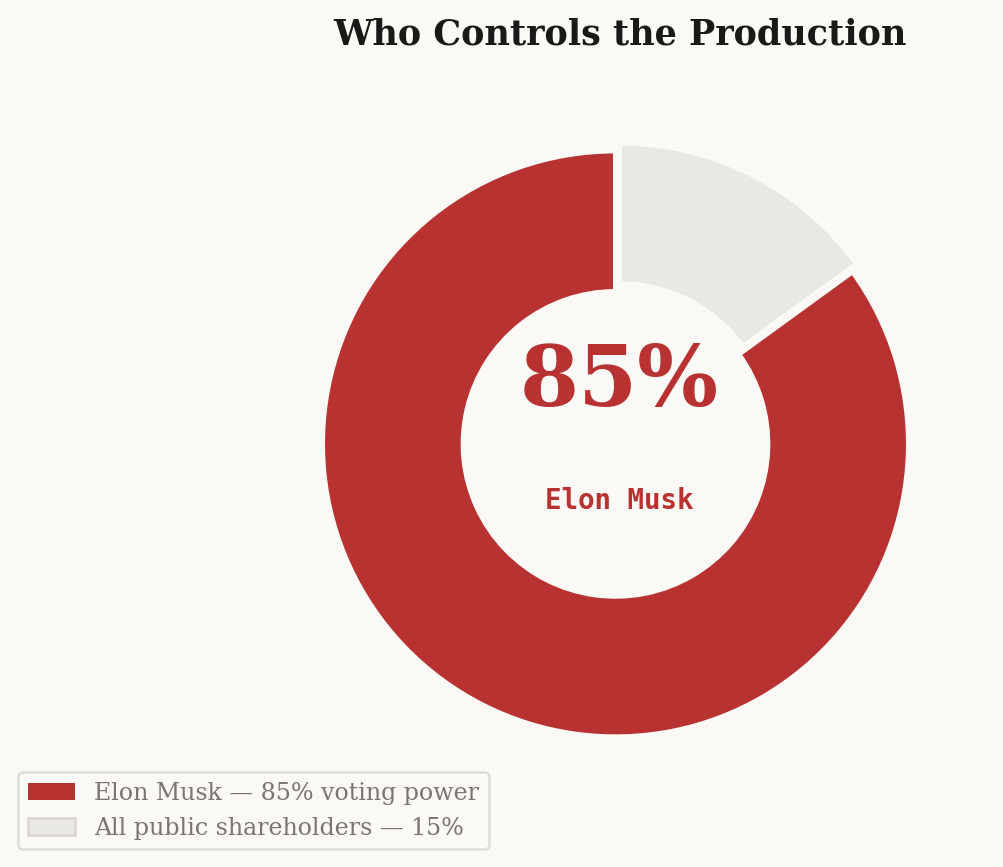

Then there is the governance question. I want to show this clearly, because it tends to get lost in the excitement about rockets and Mars colonies.

If Musk wants SpaceX to lean harder into AI infrastructure, Mars, Starlink, Grok, or some future project none of us has heard of yet, public shareholders will not be sitting around the table with a meaningful vote. They will own a piece of the production, but not the stage directions.

If he wakes up one morning and decides SpaceX should acquire X again, he can. You would own a piece of the production and have no say in the casting, the venue, or the running time.

In any meaningful governance sense, you’re a ticket holder. The production company runs the show.

The Bit the Programme Leaves Out

Peter Lynch, who ran Fidelity’s Magellan Fund to a 29% average annual return over 13 years, had a test for every investment he considered:

“If you can’t explain to an 11-year-old in two minutes or less why you own the stock, you shouldn’t own it.”

Peter Lynch, former manager, Fidelity Magellan Fund

I want you to try explaining the SpaceX investment thesis to an 11-year-old.

“It’s a rocket company, but also a satellite internet company, and now partly an AI infrastructure company, and it has exposure to Grok and X, and it may be valued around $1.75 trillion even though it just lost more than $4 billion in a single quarter, and the founder controls about 85% of the votes, and he also runs Tesla, X, xAI and Neuralink...”

You might lose the kid at “satellite internet.” Lynch’s point was never about simplicity for its own sake. It was that if you can’t articulate the thesis clearly, you probably don’t understand it clearly. And the IPO process is specifically designed to make you feel like you understand something you don’t have the backstage information to properly evaluate.

Here is the part I want you to really absorb: the information gap in IPOs is structural and deliberate. The insiders, founders, early employees, and venture capitalists, have lived with this company for years. They know the actual revenue trajectory. The real customer churn rate. They know the competitive threats that didn’t make it into the programme.

Every one of them is selling to you. The banks advising the deal earn their fees from the company, not from you. The analysts covering the IPO work for those same banks.

You, sitting at home reading a prospectus that runs hundreds of pages, with a deadline, are being asked to out-analyse all of that in the two-week roadshow window before opening night.

“If you’ve been playing poker for half an hour and you still don’t know who the patsy is, you’re the patsy.”

Warren Buffett

In the IPO game, the patsy has a name. It’s the retail investor who buys on opening night, reads the rave reviews in the financial press, and assumes they’re getting the same deal as the institutions who got tickets six months ago.

So, What Will I Do?

I want to be clear: this article stops well short of calling these bad companies.

They could be extraordinary ones.

Starlink is a dominant business in low-earth-orbit satellite broadband, especially in places where terrestrial internet is weak, expensive or simply unavailable. Falcon 9 has an unmatched launch cadence. Anthropic is reportedly growing fast. OpenAI has more than 900 million weekly ChatGPT users and a product embedded in the workflows of students, developers, lawyers, founders, analysts and probably half the people pretending they are not using it.

These are remarkable performances.

The technology is real. The moats are real. The question I keep coming back to is the price at which you buy, and the moment at which you buy it.

Here is what I will do: grab some popcorn, read some Buffett and Munger, and wait for the reviews.

Every great production has a run that extends well past opening night. The lock-up expiration, often around 180 days after an IPO, is one of the first moments when early employees and investors may be allowed to sell more freely.

That does not guarantee a crash. Nothing in markets is that neat.

But it does change the supply of shares. It changes the cast of sellers. And it gives you something opening night does not: more information.

The first few earnings reports, stripped of the roadshow energy and the carefully rehearsed narrative, tell you what the business actually looks like when the lights come up on a Tuesday afternoon in a half-empty theatre.

The Show Will Go On

We are living through a genuinely remarkable season. The companies that may come public in this cycle, a rocket company trying to make Mars real, the laboratory that helped turn AI into a consumer product, and the teams building the language models now reshaping work, are the kind of productions that define eras.

I keep coming back to Netscape.

The Netscape IPO in 1995 helped launch the internet era. The stock exploded on opening day. The phrase “Netscape moment” became shorthand for the arrival of a new technological age.

And yet the lesson was never simply “buy the IPO.”

The internet changed everything. Netscape itself did not become the enduring winner. The show ran for thirty years and is still running, but the money was not made by blindly buying every opening night. It was made by understanding which parts of the new world would actually endure.

The companies are real. The technology is real. The performances will be extraordinary.

“The only question that matters is at what price you’re being asked to buy a seat.”

Right now, you’re being asked to believe in SpaceX at a valuation of roughly $1.75 trillion, while it is losing billions under GAAP accounting, in a production where the lead actor controls the stage directions and public shareholders have very little say in the script.

What I might do: wait for the reviews.

Let the opening-night energy settle. Let the first earnings reports arrive. Let the lock-up calendar do what lock-up calendars do. The show will still be on. The seats may be better value. And you’ll know, finally, whether the production is as good as the programme promises.

One more thing. Bruce Hornsby's 'The Show Goes On' has been on repeat in my house this week. Make of that what you will.

Disclaimer:

This is an opinion piece. It is not financial advice. Think of it as the kind of conversation a well-read friend would share over a beer, someone with no financial interest in your decision. Make your own choices. Read the S-1. Speak with a licensed financial adviser. And remember Munger’s Rule: if it comes with a 200-page programme and a large commission, the curtain may not rise the way they promised.

Great article Rob. We are on the same page here. These are 3 IPOs that I'll gladly grab the popcorn for in the cheap seats. Valuations are running way too hot on all of them. $CBRS was another one... very interesting company and product, but bad valuation for the intelligent investor, especially when factoring in the OpenAI risk.