Toast: A Deep Dive

A founder-led toll booth on the American restaurant, drowning in cash at last. So why do I own only a sliver?

This deep dive is perfect listening for your next walk. And also: drop it into NotebookLM and let it generate audio overviews, infographics, and summary reports from the analysis. It’s a great way to absorb the key ideas without staring at a screen. Enjoy!

I stumbled upon Toast the way I find a lot of names: out walking, with my headphones on.

Sean Barrett broke the company down on Business Breakdowns and made the bull case about as well as you will hear it: a restaurant that runs on Toast tends to stay, the share keeps moving its way, and after years of burning money, the cash has finally started to pile up. “A better company today than ever before”, he stated.

I came away genuinely interested, which does not happen as often as the size of my watchlist would suggest.

But interested is a looong way from invested.

A great story is where the work starts, and a good podcast, however persuasive, cannot answer the one question that decides everything for me: is the price low enough to give me a real margin of safety? So I ran home, pulled the filings, built the numbers myself, and went looking.

Here is what I found.

Note: I bought a sliver of Toast so it would have my attention (and to use that pun), because a name I own is a name I actually read. The position is tiny though, and that’s on purpose. I respect the business. So far I have refused to pay up for it.

If you’re in a rush

They sell restaurants the one system the whole place runs on: the till on the counter, the software for the floor and the kitchen, the card processing under every order, and a growing stack of add-ons like payroll, lending, and marketing. Most of the money comes from a small slice of every card payment, which is why processing is the engine.

The market loves them for taking share off Block and finally turning a real profit, and fears them as the next victim of the so-called SaaSpocalypse.

What governs the outcome is the price I pay for a destination that is probable but not yet locked.

The internal verdict is a ‘Yes’ with an asterisk, so the published label is Watchlist, owned at an attention-only weight.

I am paying close attention.

Pricing: The Atomic Moat

Premium members pay $199 per annum. With this membership, you will get access to all my curated watchlists and fat-pitch triggers, which will save you a lot of time and effort. You will also get access to my current portfolio, deep dives, and much more.

Three MIT engineers and a point-of-sale that ran on a DOS prompt

The idea came from a bad dinner. Steve Fredette, Aman Narang, and Jonathan Grimm, all MIT graduates who had met building search software at Endeca (a company Oracle swallowed in 2011), were eating in Kendall Square and watched the staff fight with a point-of-sale system that kept crashing and rebooting to an antiquated DOS prompt.

Narang’s phrase for it later was that these systems were old and scary for the people who had to use them.

So they built one. It started in Narang’s basement in 2011 as a humble consumer app for mobile payments and loyalty, then became the thing the restaurant actually runs on. That pivot is the origin of the moat. They went deep on one trade. They talked to restaurateurs for hours and built features a generalist would skip: real-time messaging to the kitchen about a dish that just sold out, software shaped around the rhythm of a Friday-night rush.

Chris Comparato ran the company as CEO from 2015 through the scaling years. On the first day of 2024, Narang, the co-founder, took the chair. Founder-led again, with the engineer who saw the crashing DOS prompt now allocating the capital.

The lesson the origin teaches, and the one I keep returning to, is that the vertical focus is the asset. A bear with a balance sheet could copy the software in a year. Copying fourteen years of restaurant-specific obsession is the part that breaks attackers.

What you are actually buying

Picture a busy operator on a Friday night. Tickets are flying to the kitchen, a server is splitting a check four ways, a delivery order pings in, payroll runs Monday, and the whole thing sits on one system from one vendor.

That is what Toast sells: the restaurant’s operating system. They make most of their money the way a toll booth does, by taking a thin slice of every dollar that passes through.

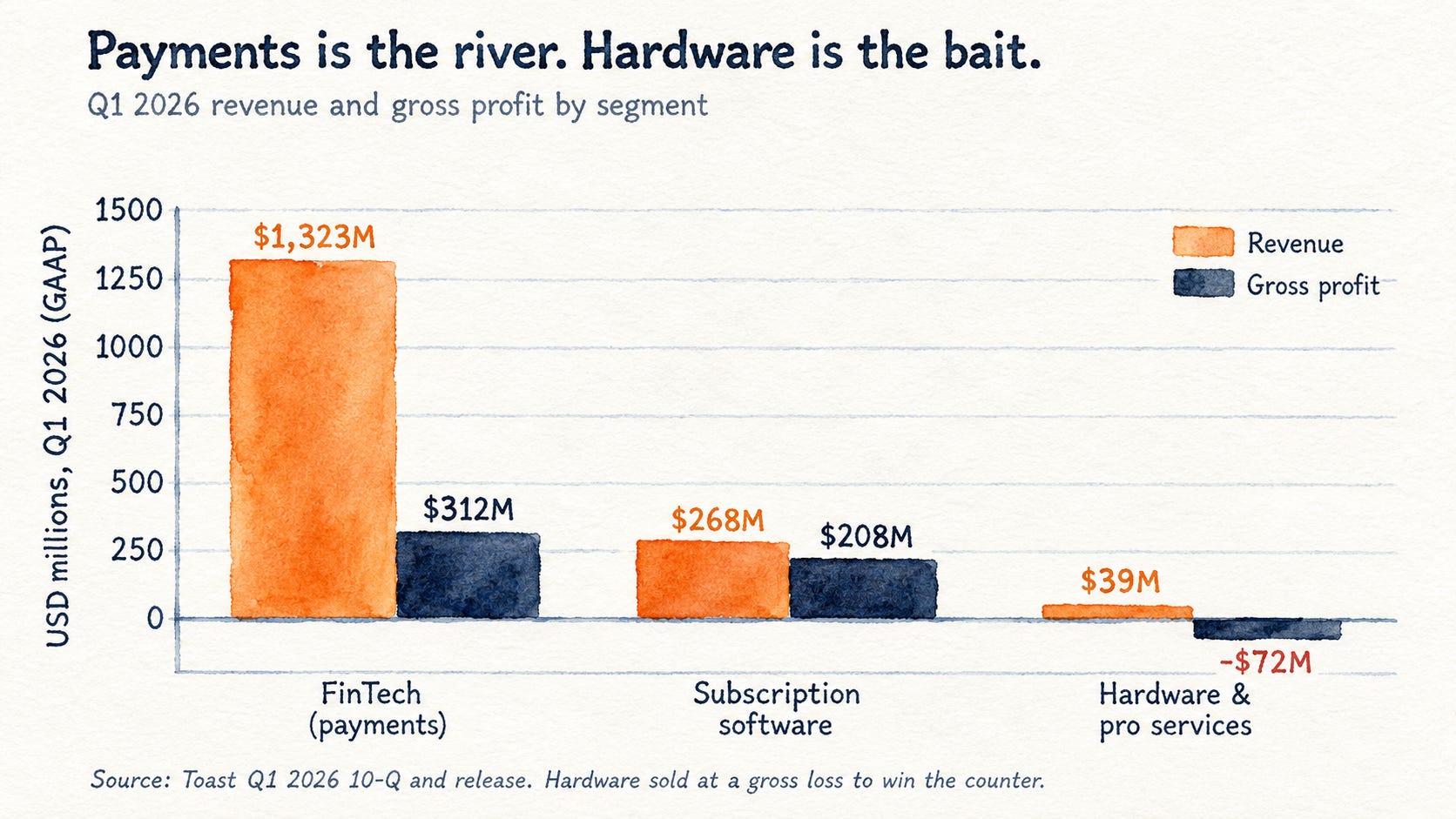

The slices are uneven. Of $1,630M of revenue in the first quarter of 2026 (Q1 2026, USD, GAAP, 10-Q), the financial-technology line, mostly card processing, was $1,323M.

Subscription software was $268M.

Hardware was just $39M, and here is a tell worth holding onto: hardware runs at a gross loss of roughly minus $72M for the quarter (Q1 2026, GAAP, release).

They sell the terminals cheaply to get the system onto the counter, because once it is there and running the business, it tends to stay.

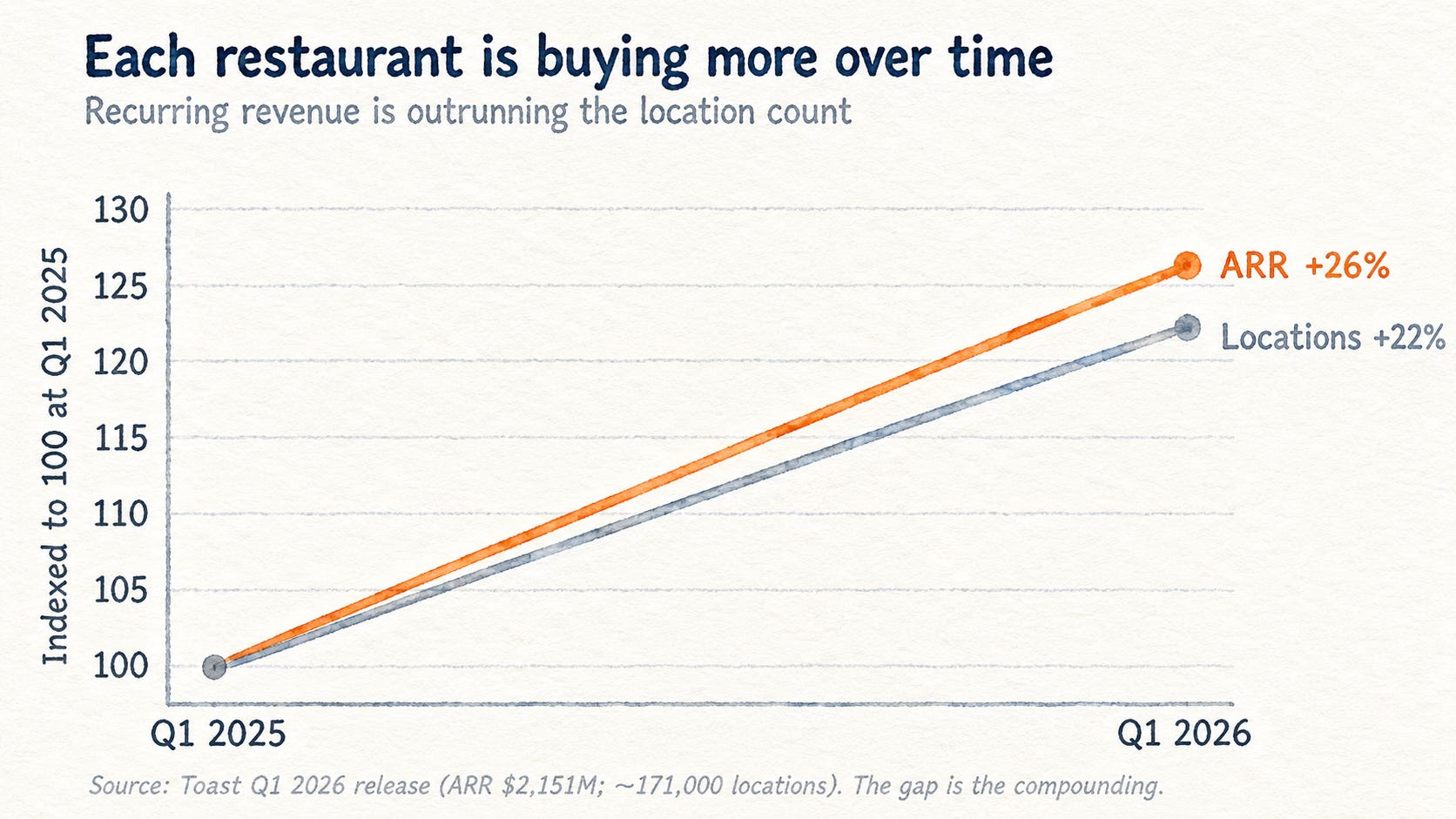

The interesting motion is underneath the headline. Annualized recurring run-rate grew 26 percent year over year to about $2.2 billion (as of March 31, 2026, company-defined non-GAAP, release), while locations grew 22 percent to roughly 171,000.

Recurring revenue is climbing faster than the location count, so each restaurant buys more over time: payroll, lending, marketing, and the new AI tools.

HYPOTHESIS: The attachment of fintech and software lifts revenue per location for years, because the system is sticky and the cross-sell is cheap.

MONITOR: ARR growth against location growth. While the first outruns the second, the engine is turning.

A crowded pond, and the edge I give up to fish in it

Toast is a $15 billion company on the New York Stock Exchange, followed by somewhere between fifteen and twenty-seven analysts depending on which estimate sheet you read.

Every line in the filing has been chewed over by professionals with better terminals than mine.

Owning Toast, I step into a ring with the most-resourced investors alive, on a name they all know cold. The too-big check, drift risk number two, fails outright: at this size, my position is a rounding error in daily volume, so the liquidity wall that usually guards my edge is absent.

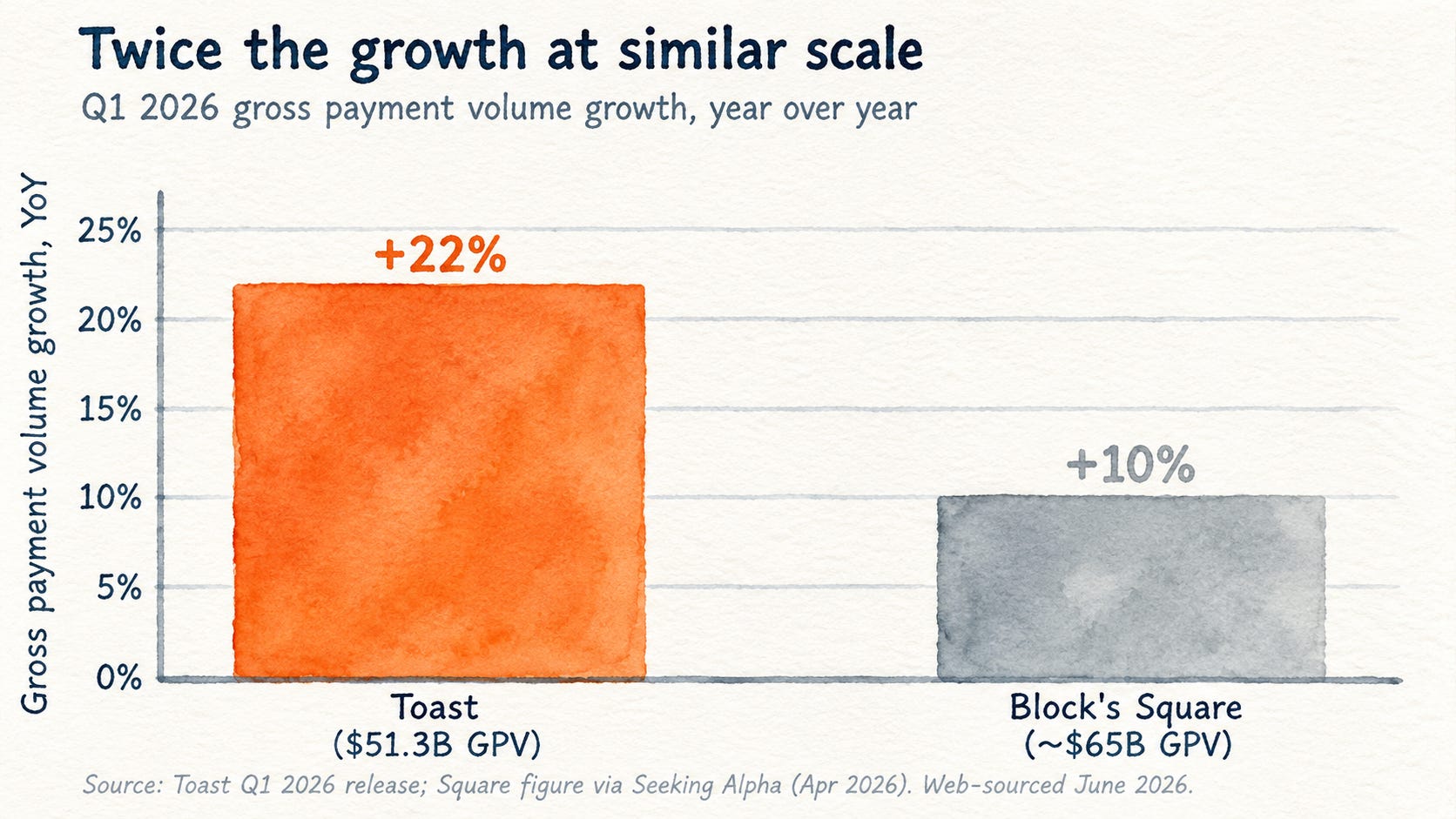

What the crowd has not settled is the competition. Toast is the shark in a fragmented tank. Its gross payment volume grew 22 percent year over year to $51.3 billion last quarter, while Block’s Square, at a similar scale, grew about 10 percent.

Management says Toast now powers around a fifth of US small and mid-market restaurants, double its share of three years ago. The rivals are real and well-funded: Fiserv’s Clover, SpotOn, the legacy Oracle Micros boxes, and a coming wave of AI-native entrants. Taking a share of Block while the others circle is the evidence that counts.

Atomic Take: I am fishing where I hold no structural advantage, so I had better get paid for it in the price.

Falsifier: net location adds decelerate while a named rival’s accelerate.

What stops a rich, clever rival from simply stealing these customers

Run the grizzly test first: Put a well-capitalized, intelligent competitor in the room and ask whether it is still likely to lose. Mostly, yes. Restaurants do not rip out the system that runs their floor on a whim, and when they do switch, they tend to switch toward Toast, which is why the share keeps moving its way.

Here is the Patterson sentence, the one specific barrier in a single line. A well-funded rival would find it prohibitively hard to take meaningful restaurant share within five years, because Toast’s hardware, software, and payments are fused into the daily running of the business, and switching means retraining staff and risking a service meltdown on the one system a restaurant cannot afford to have go dark.

The moat model, named plainly, is high switching costs that deepen with every product the restaurant attaches. I want to be careful with the prettier label. Scale economics shared is the Nomad whiteboard’s most powerful idea, the Costco move where saved pennies are visibly handed back to the customer and volume follows.

Toast does some of this, ploughing scale into more product, twenty-plus updates in the spring release, a drive-thru system, and an AI marketing agent. The payment take rate is the profit, and they keep it rather than cutting it to chase volume. So I will call scale-shared a secondary, emerging feature here and lean the thesis on switching costs, which stands on its own as a first-class moat. The idiot-proof test passes: the installed base would survive five years of mediocre management.

Now the mis-categorisation sentence, the heart of any re-rating case. The market prices Toast through the heuristic of AI-disruptable horizontal software, when the right lens is a payments-and-hardware-anchored vertical operating system, where the physical till and the switching costs blunt the disruption and AI feeds the business more than it threatens it.

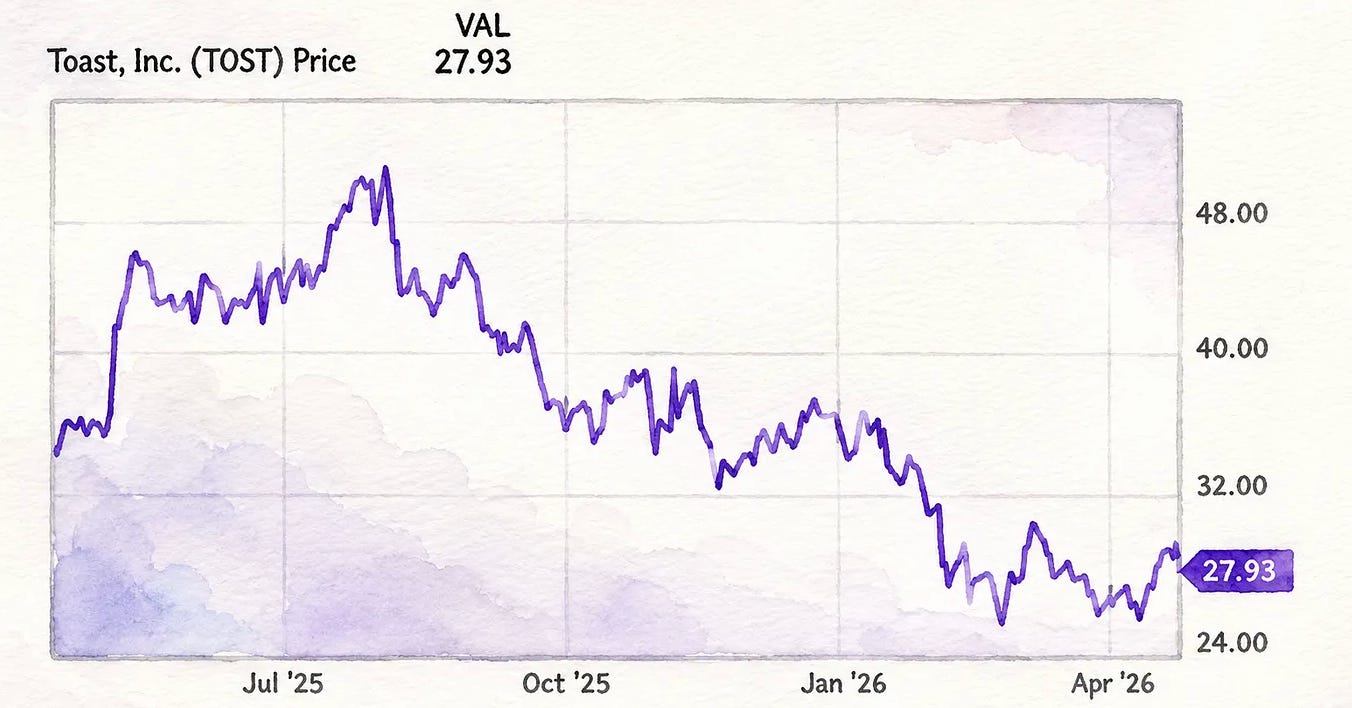

The Audit on that thesis: it is half-spent already. The stock fell from about $50 to about $26 on exactly this fear, so much of the re-rating I would be hoping for has either happened or been prepaid by the market’s panic. The spring is half-uncoiled.

Atomic Take: the moat is real and built from switching costs, and the cheap re-rating it once offered has largely been collected by the people who bought the panic.

Falsifier: blended payments take rate or net revenue retention falls for two consecutive quarters.

The river of cash, and where the taxman is about to step in

Follow the one river. Money comes in the door, $6,446M of it over the trailing twelve months (TTM to Q1 2026, USD, GAAP-derived, my spreadsheet). A lot is spent paying the card networks because the payments line is reported gross, which leaves gross profit of $1,694M.

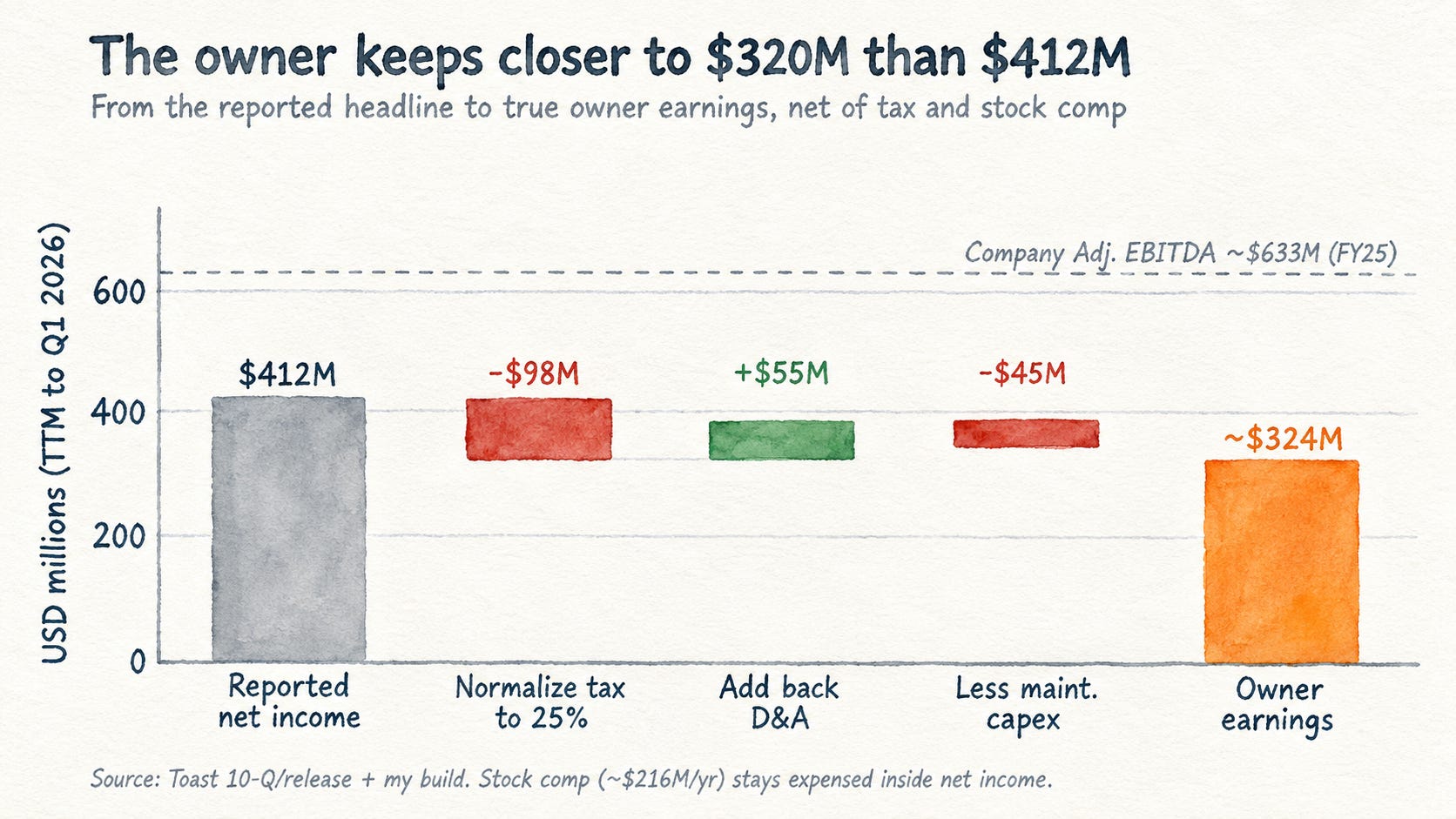

Then the sales force, the engineers, and the overhead take their share, leaving operating income of $364M (TTM, GAAP). The reported bottom line reads $412M of net income (TTM, GAAP), and here I slow down.

Two things flatter that number. First, the company has paid almost no tax, $5M on $131M of pretax income last quarter, because of a valuation allowance against past losses that the company itself says could be released within twelve months (Q1 2026, 10-Q). When it releases, a real tax bill arrives. Second, a chunk of pretax income is interest on the cash pile, which is real and recurring, and which is also not the operating business compounding.

Now the discipline. Munger’s instruction is to substitute the words “bullshit earnings” every time someone says EBITDA, and management does lean on an adjusted-EBITDA frame and a 40 percent long-term EBITDA margin target that steps around two real costs: stock-based compensation and tax. Stock comp ran about $54M in the quarter, roughly 3.4 percent of revenue (Q1 2026, 10-Q), and I expense it in full.

Do the honest build. Start from normalized net income with tax at 25 percent, about $314M, add back depreciation of about $55M, subtract a maintenance-capex estimate of about $45M (this is an asset-light software business, where depreciation is a fair proxy), and leave stock comp where it belongs, charged against the owner. Owner earnings land near $300M to $320M for the trailing year. On a $15 billion market value, that is an owner-earnings yield of about 2 percent.

Atomic Take: the business now genuinely drowns in cash, and the current owner yield is thin once you tax it properly and charge it for its stock comp.

Falsifier: stock-based compensation reaccelerates above 5 percent of revenue.

The Geiger test, the turbine, and the reactor

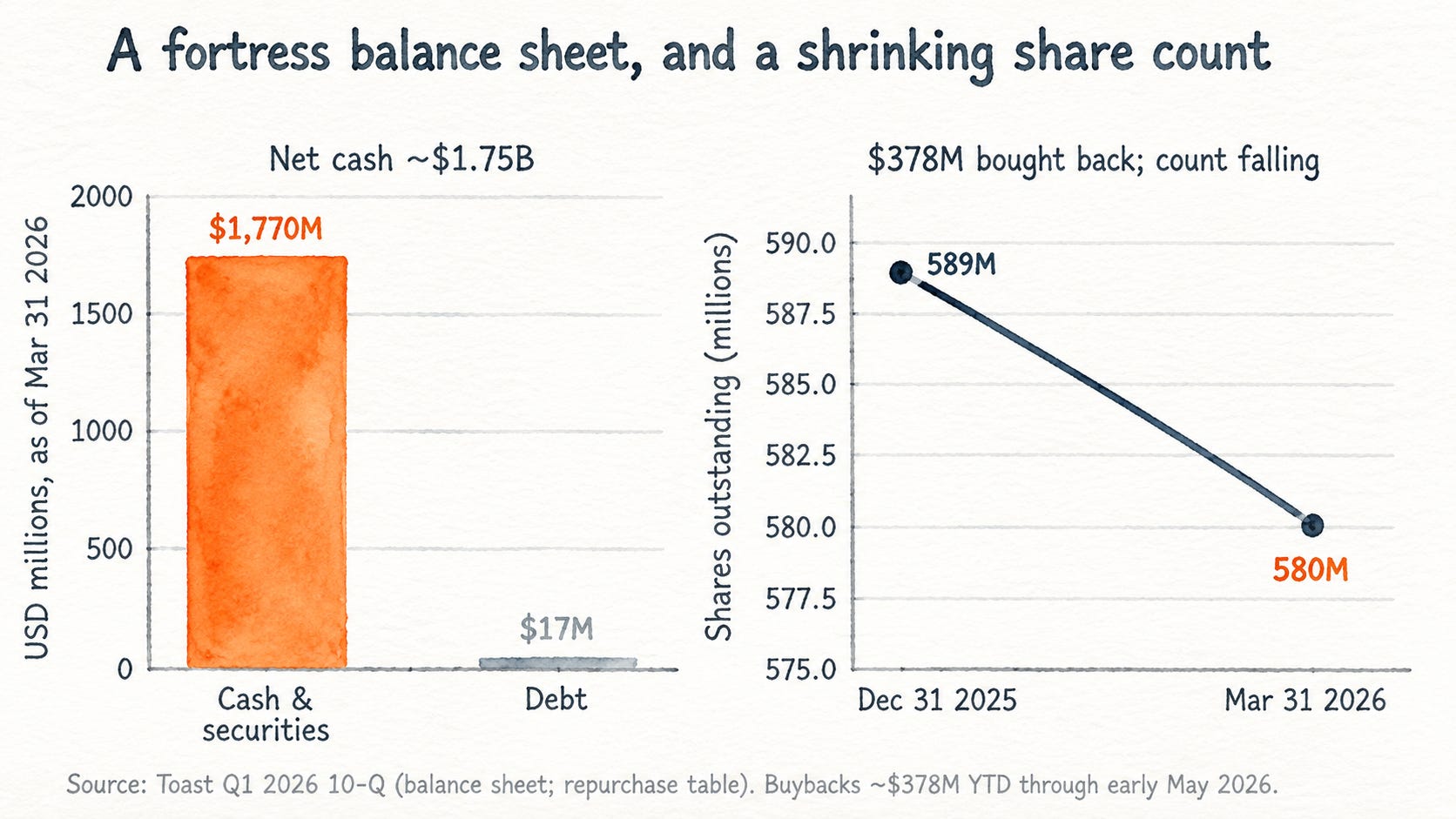

Take the balance sheet first, the Geiger counter for fragility. Cash and marketable securities of about $1.77 billion sit against roughly $17M of debt, so the company carries net cash of nearly $1.75 billion (as of March 31, 2026, USD, 10-Q). Return on equity of 20.7 percent and return on assets of 13.3 percent on a trailing basis (my spreadsheet), both flattered a touch by the tax holiday. Nothing here keeps me up at night.

The turbine is the cash flow. Free cash flow was $115M in the quarter on the company’s own measure (Q1 2026, company non-GAAP, release), and cash from operations covers reported profit comfortably. The capex-intensity flag stays green: this is a light business that does not spend heavily to stand still, so checks fourteen and fifteen of my eighteen both pass, and the BNSF detector, the warning that a business eats capital faster than it admits, stays quiet.

The reactor is the income statement, and this is where the one real distortion lives. Blended gross margin reads about 26 percent (TTM, GAAP), which fails my 40 percent screen.

That single fact, the choice to report payment volume as gross revenue, mechanically depresses gross margin, net margin, and the ratio of overhead to gross profit all at once. It is one structural artifact, and I charge it a single time. Strip it back, and the underlying software-and-payments gross profit is the number that matters, and it is growing fast.

The Audit on any optical cheapness: there is none to perform, because the stock is not optically cheap. It trades around 20 times forward earnings and 37 times trailing, with an owner yield near 2 percent. The statements are clean. The price is the problem, and I will get there.

Atomic Take: a strong balance sheet and an asset-light cash engine, where the only “failure” is a reporting artifact I refuse to double-count.

Falsifier: free-cash-flow-to-net-income falls below 0.7 on a clean basis.

The people allocating the capital

Founder-led, disciplined, and lately profitable. Aman Narang sits in the CEO chair he co-founded the company to fill, with super-voting Class B stock concentrating control, a governance fact I keep an eye on.

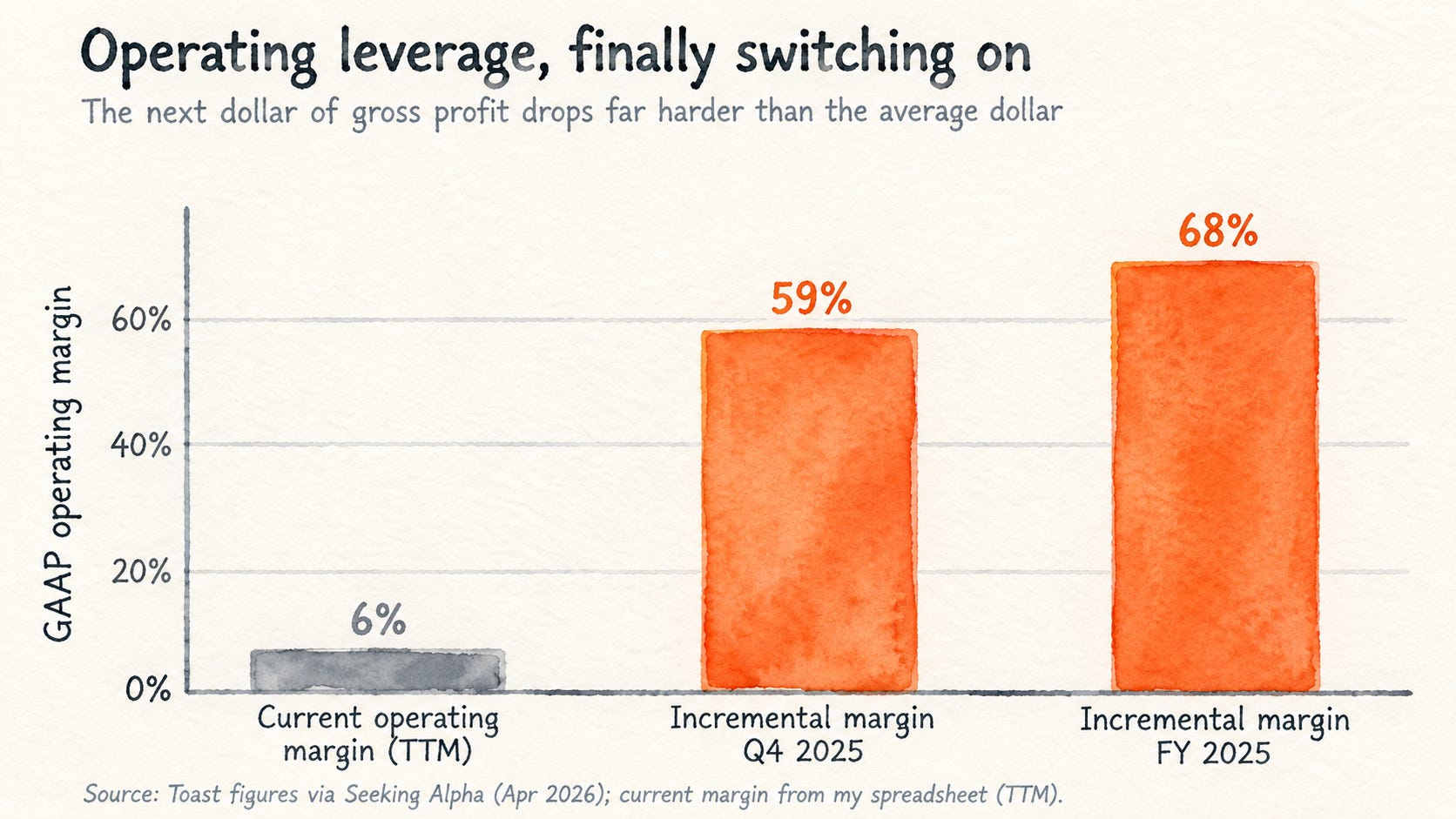

The retained-earnings test, which asks whether a dollar kept turns into more than a dollar of value, now works: incremental operating margins were reported around 59 percent in the fourth quarter and roughly 68 percent for the full year, so the next dollar of gross profit drops a large share to the operating line.

The capital-allocation behavior is mostly the kind I want to see. The share count fell, from 589 million to 580 million, as buybacks of $378M year to date through early May (company release) outran the stock handed to employees.

Shrinking the count while founder-led is the right instinct.

I hold one honest reservation, tagged. Handing back this much cash so soon, while the incremental returns are so juicy, hints that the highest-return internal runway is not infinite.

HYPOTHESIS: The buyback partly substitutes for a reinvestment opportunity.

MONITOR: the price they pay against my estimate of intrinsic value, because a buyback near or above fair value is housekeeping, and only a buyback below it builds per-share wealth.

At roughly $27 to $33 a share, against my central estimate near $23, those repurchases look fairly priced, so I credit them only mildly.

Atomic Take: the founder is back, the dilution has reversed, and the buyback is sensible without being a value gusher.

Falsifier: buybacks accelerate well above intrinsic, or stock-comp dilution resumes.

Where this goes by the early 2030s

The destination question decides everything, and Nick Sleep framed it best: do not ask what the business makes in year three, ask what it looks like as a mature franchise in fifteen to twenty years.

The runway is genuinely long, and it is the kind that widens as the company digs. Beyond more US restaurants, there are international, retail, enterprise, the roughly 140,000 US drive-thru locations they just built a product for, and the fintech and AI layers stacking on top. This is a company that can enlarge its own pond; the trait that kept Amazon from being capped at “online retail is tiny.”

Here is the discipline, though. The destination is large and probable. It is not yet secured. It leans on continued share gains, on margins expanding the way the bulls model, on the AI vector cutting for the company, and on no recession knocking the wind out of restaurant spending.

A probable-but-unsecured destination earns my full margin-of-safety bucket, and I hold that line in the next section.

Compound a fading growth rate, say 20 percent decaying toward 10 as the pond fills, off a roughly $7.5 billion revenue base, and you get something like three times the revenue by 2032. Layer on margin expansion, and earnings might grow three to five times. That places the intrinsic business in a 3-to-5x band at the optimistic end over six years. A clean 5-to-10x by 2032 sits above that, out at the bull-of-bull edge, and I will not size to an edge.

Atomic Take: the runway is long and self-widening, and the destination is probable while it is unsecured, which sets the price bar high.

Falsifier: two years of sub-12 percent revenue growth with no macro shock to blame.

What is it worth, and am I overpaying?

Price comes last, and price is the binding constraint. This is the section that explains where I believe the fat pitch for Toast is: