What Michael Burry Actually Teaches Us

Mastering the Drawdown: The Strategies and Mindset We Can Actually Steal from Wall Street’s Most Stubborn Investor.

I have a confession to make before we get started. I am a quality-compounder guy. I want businesses that earn high returns on capital and reinvest them for a decade. Michael Burry is almost the photo negative of that.

He buys ugly things. He shorts beautiful ones. He has spent most of his public life betting against the very mania that made everyone else feel like a genius.

And I admire him anyway.

I have no desire to trade like him. I never could. What I admire is the temperament. The patience. The willingness to sit alone in a position, be hated for it, and keep sitting there because the math says you are right.

That is rare. Most of us cannot do it for a single week. Burry has done it for years at a stretch, with real money, while the crowd laughed at him.

So let me walk you through how he became a legend. Then let me show you what is worth stealing from him, even if you never short a single stock in your life.

The kid who could not stop reading

Burry was born in 1971 in San Jose. At the age of two, he lost his left eye to a rare cancer called retinoblastoma, and he has worn a prosthetic eye ever since. He has said this shaped him into an observer. A loner. Years later, he recognized that he has Asperger’s after his own son was diagnosed first.

He once described himself with no varnish at all.

“My nature is not to have friends. I’m happy in my own head.”

Most people would probably never say it out loud. Burry says it the way you would report the weather.

He studied economics and pre-med at UCLA, then earned his MD at Vanderbilt. He started a residency at Stanford and never finished it. The reason is the whole man in miniature. He kept staying up at night doing something that had nothing to do with medicine. He was picking stocks.

He once worked so hard on both at the same time that he fell asleep standing up during a surgery.

In 1996, he started posting his investment ideas on a message board called Silicon Investor. The writing was good. Really good. He built a site called valuestocks.net that won a Best of the Web award from Forbes for stock picking, and won it twice. Vanguard noticed him. Joel Greenblatt noticed him. People with serious money started asking this anonymous surgeon-in-training to manage theirs.

That is the part I love. He did not network his way in, and he had no pedigree desk job at Goldman. He wrote clearly about businesses, year after year, and the work spoke for itself. The internet found him.

Scion, and a fantasy novel

In 2000, he quit medicine and started a hedge fund. He funded it with a small inheritance and loans from his family. His mother put in $20,000. Each of his three brothers put in ten.

He named the fund Scion Capital.

Michael is quite the fan of The Shannara Chronicles, and the name Scion specifically hails from The Scions of Shannara, a 1990 fantasy novel by Terry Brooks.

This is one of Burry’s favorite books. He was nineteen when it was published (The TV show arrived much later, in 2016, and draws from a different Shannara story entirely - although I personally think it was a shame that it got cancelled).

A scion is an heir. A descendant who carries a bloodline forward. In the novel, the scions are the last heirs of an ancient family, each one handed a quest that looks impossible, in a world where their kind of magic has been outlawed and blamed for everything going wrong.

I cannot tell you that Burry sat down and mapped that fable onto his career. I doubt he would claim it. But I read something into the choice anyway, and I think it is fair to. Here was a man who saw himself as an heir to a tradition.

The tradition of Graham and Dodd. Real value investing.

He took up a quest most people thought was foolish, inside a market that had effectively banned his kind of thinking and blamed it for missing the party. He named his life’s work after that idea.

That is what a name is for. It tells you who a person believes they are.

The years that made him

His investing style was old-fashioned and strict. He built the whole thing on one book, Graham and Dodd’s Security Analysis from 1934, and he has said his stock picking is “100% based on the concept of a margin of safety.” He read 10-Ks the way other people read novels. Alone, for hours, in a dark office, hunting for the number that tells you what is actually there underneath the story.

And it worked, fast.

In 2001, the S&P 500 fell almost 12%. Scion was up 55. In 2002, the market fell again, down 22%, and Scion was up 16%. In 2003, the market finally turned and rose nearly 29%, and Burry still beat it, up 50%.

By the end of 2004, he was managing 600 million dollars and turning new money away. A lot of those early gains came from shorting overpriced tech stocks while the dot-com bubble was deflating. He was already running his whole playbook. Buy hated value. Short the fantasy. Wait.

Then came the trade that put his name in a movie.

The Big Short, and the revolt

In 2005, he started pulling apart the subprime mortgage market. He read the actual loan documents stuffed inside the mortgage bonds. He saw loans handed to people with no income and no down payment, then packaged and rated as if they were safe. He concluded the whole structure would come apart once the teaser rates reset. So he did something almost nobody had done. He went to Goldman Sachs and others and asked them to create credit default swaps so he could bet against specific subprime deals.

His own investors tried to fire him.

They did not understand the bet. Housing kept rising. Burry was paying premiums every month on a short that was not working yet, and his clients were furious about it. Some demanded their money back. He had to gate the fund to stop them from yanking it out. Picture that for a second. You have done the work. You are right. And the people whose money you are protecting are screaming at you for protecting it.

He held.

By the middle of 2007, subprime began to collapse, exactly as he had said it would. Scion made 725 million dollars for its investors. Burry personally cleared around 100 million. From its start in late 2000 to the middle of 2008, the fund returned 489 percent net of fees. The S&P 500 returned roughly 3 percent over the same stretch.

Then he closed it. The backlash, the IRS audits, the sheer exhaustion of being right while everyone fought him. He was done managing other people’s money. For a while.

This is the part Keynes warned us about, and Burry actually lived. The market can stay irrational longer than you can stay solvent. Being early and being wrong look identical for a long time, and they only separate at the very end. Most investors never reach that end, because they get shaken out, or talked out, or simply bored out of the position first. His real edge had nothing to do with a secret formula. He could just sit in the discomfort longer than you can.

Cassandra in the wilderness

He reopened a fund in 2013 as Scion Asset Management. And then he spent the next decade building a second reputation, as the boy who cried crash.

I am going to be straight with you here, because this newsletter does not do hero worship.

A lot of Burry’s big public calls since 2008 have been wrong, or at the very least painfully early. In 2017, he warned of a global financial meltdown. The market rose. In 2019, he said index funds were the next CDOs, a bubble waiting to burst. They kept inflating and never burst the way he meant.

In June 2021, he warned of “the mother of all crashes.” Stocks rallied more than 50 percent from there. On January 31, 2023, he tweeted a single word. “Sell.” The market promptly ripped higher. Two months later, he tweeted, “I was wrong to say sell,” and went on to congratulate the buy-the-dip crowd for their nerve.

One writer tried to actually score his record and figured roughly 71 percent of his major bearish calls since the crisis were wrong on timing or size. The Financial Times described his performance since The Big Short as “distinctly ho-hum.” When he shorted Nvidia and Palantir in late 2025, Palantir’s CEO Alex Karp went on television and called the bet “bat-shit crazy.”

So yes. He gets mocked. Constantly. And harshly, if you ask me. Often by impatient people who treat every tweet as a date-stamped prophecy and then high-five each other when the market climbs the following week.

But look at what the mockers keep missing.

First, Burry picked his own nickname years ago. Cassandra. The priestess in the Greek myth who was cursed to see the future clearly and to never, ever be believed. He chose that name on purpose. It tells you, right on the label, that being disbelieved is the whole job.

The only thing he writes now, the project that has become his entire focus, is his Substack publication: Michael Burry .

Second, the scoreboard depends on what you actually measure. His macro timing calls have a poor hit rate. True.

His disclosed long positions, the real stocks he bought, were a completely different animal. One analysis found that simply copying Scion’s disclosed holdings returned around 56 percent a year from 2020 to 2023, against about 12 percent for the S&P 500 (source: CNN Business/Sure Dividend).

The man who “keeps getting it wrong” was a very good stock picker the entire time. The crash tweets just hogged the headlines.

Third, he said it better than I can when the Wall Street Journal labeled his early calls a failure. Being early and being wrong look identical in the short term and diverge completely over time. One reflects bad analysis. The other reflects the market refusing, for a stretch, to price reality.

I am not telling you Burry is always right. I am telling you the crowd’s way of grading him is lazy, and the man understood that before any of them did, and put it in the name on the door.

What he just told us

Which brings me to the thing that made me want to write this piece in the first place.

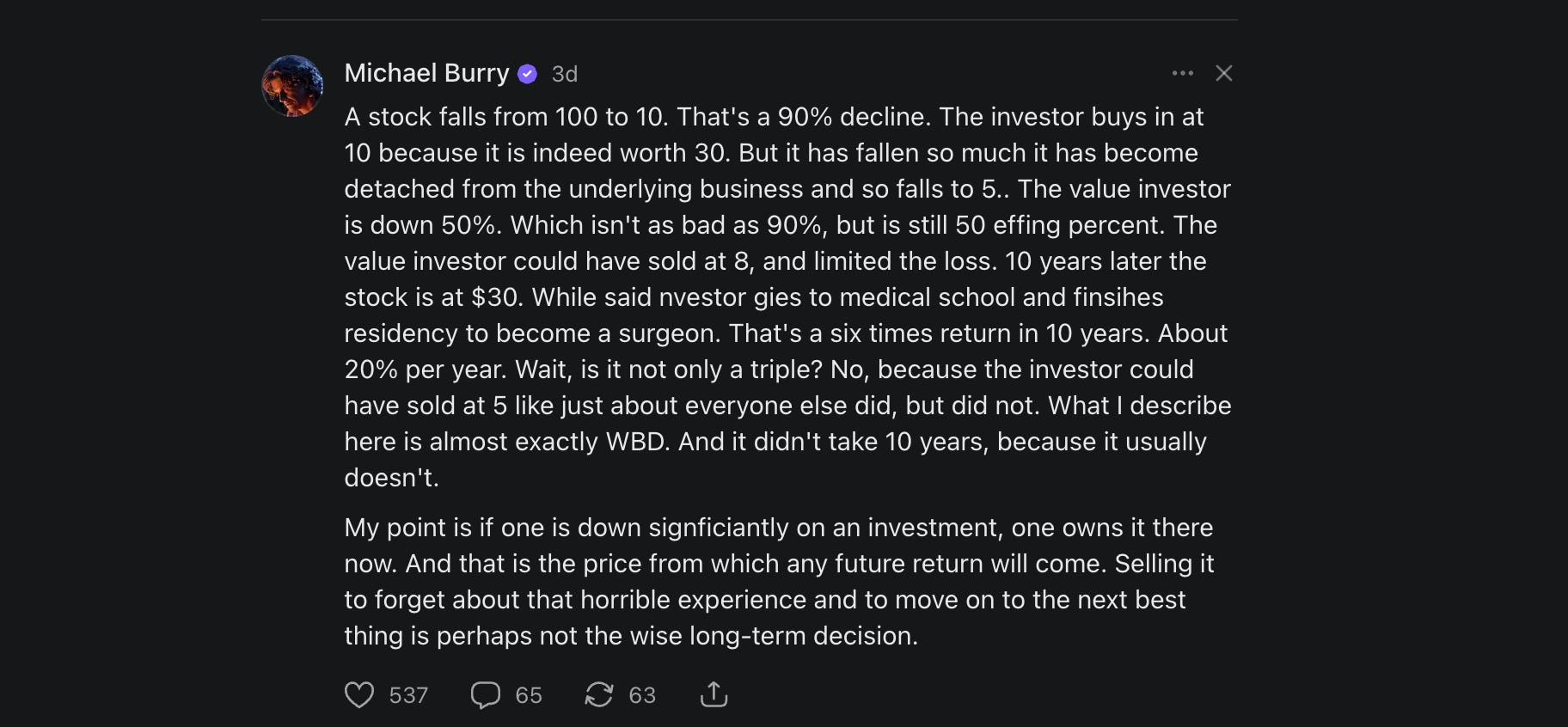

A few days ago, Burry published this note on Substack:

He laid out a simple story. A stock falls from 100 down to 10. That is a 90 percent wipeout. Ouch…

A value investor steps in at 10, because the business is honestly worth around 30.

Then the thing keeps sinking, all the way to 5, because a stock that has fallen that hard stops tracking the business underneath it.

Our investor is now down 50 percent on his buy. He could have bailed at 8 and capped the damage. He sits tight instead.

So, he goes off to medical school, finishes his residency, becomes a surgeon, and a decade later, the stock trades at 30. From the bottom, that is a six-fold return. Roughly 20 percent a year. He says this maps almost perfectly onto Warner Bros. Discovery, and he points out that it usually does not even take the full ten years.

Then comes the line I keep rereading.

If you are sitting on a deep loss, you own that position at today’s price, full stop. Whatever it is worth from here is the only return you will ever earn on it. Dumping it just to make the bad feeling go away, to erase the memory and chase the next shiny idea, is usually the wrong long-term move.

Sit with that one. It dismantles one of the most common mistakes any of us make.

We anchor to what we paid.

We feel the loss in our chest. We sell to make the feeling stop, right at the point of maximum pain, which is often right before the recovery. The market has no idea what you paid and would not care if it did. Your cost basis lives in your head. The company does not know it exists. The only question that matters is what the thing is worth from here.

I have a private name for my own version of this disease. The hot potato. The urge to sell a good business too early, to lock in some relief, to avoid sitting inside a drawdown. Reading Burry describe the same impulse in a stranger’s voice was uncomfortable in the way good advice usually is.

What to actually steal from him

So here is what I take from Michael Burry, as someone who will never run his strategy:

Do the work yourself, in primary documents, until you know the business better than the people talking about it on TV. Burry beat everyone because he read the actual loan files and the actual filings while his competitors read the summaries.

Anchor to something real. A margin of safety is a hard number. It is the gap between price and what is genuinely there. Find that number underneath the narrative and build from it.

Treat your portfolio as one book, not a pile of tickers. When the headlines screamed that Burry had a “$900 million” short against Palantir, the real premium he had at risk was closer to 9 million. Copying his ticker without understanding the size, the structure, and the duration would have flattened you. The headline is never the trade.

Be willing to be hated. The best setups are uncomfortable by design. If everyone already agrees with you, the upside has already been handed out. The money tends to hide wherever the discomfort is.

Separate being early from being wrong, then be honest with yourself about which one you are. Burry has been both. The thing I respect is that when he is wrong, he says so out loud, in public, with his name attached. “I was wrong to say sell.” Most gurus would have deleted the tweet and pretended it never existed.

And the big one. Once you are down, you own it from here. Stop grieving your cost basis. Ask only what the business is worth now, and let that answer, rather than your feelings, decide whether you hold.

That is the real Burry. Forget the doom tweet and forget the movie. The actual man is stubborn, solitary, and a lot would consider him a little different from the rest.

He reads everything. He trusts his own math over the mood of the crowd. He sizes his bets with care.

And he is perfectly comfortable being the only person in the room who thinks he is right.

Until next time,

— Rob H.

I keep this The Money Mind series free for everyone. The only thing I ask in return is that you share this post with one friend who would find it valuable.