Deep Dive: Baltic Classifieds Group (BCG.L)

Fourteen websites, six million people, and a moat that gets harder to attack every year. But I still sold my position. Let's find out why.

If you read the Thesis Brief, you know the business. You know the flywheel, you know the Estonian tax shock, you know that a 78% EBITDA margin on a classifieds portfolio is genuinely extraordinary. You know the thesis.

This piece goes underneath it.

I want to be upfront about something before we start. I bought a position in BCG after writing the Thesis Brief. But by the time I finished this Deep Dive, I had sold it.

Not because the business disappointed me. The business is everything the Brief said it was, and more. But going through every corner of a company sometimes teaches you something the headline numbers cannot.

It’s about what you are actually paying, and about what you are taking on that does not show up in any financial model.

Sometimes the most valuable thing a deep dive produces is not a position. It is a clearer sense of what you are looking for.

That lesson is in here, in this deep dive. It comes near the end. I think it is worth the walk to get there.

In this deep dive we are going to:

look at each of BCG’s four segments individually, not just the revenue number but what is actually driving it and whether it sustains.

look at the two people running this business and whether they have earned the trust their shareholders are placing in them.

examine the one acquisition BCG has made and what it says about their capital discipline.

build the valuation from scratch, assumption by assumption, rather than just quoting a range.

(Put this on listen. It is built for the walk, the commute, and the gym.)

Let’s get into it.

The four segments, one at a time

BCG reports four business lines:

Auto

Real Estate

Jobs and Services

Generalist

Together they produced €44.8m in revenue in the first half of BCG’s 2026 financial year — the six months to the end of October 2025.

But the aggregate number hides something interesting.

Three of the four segments are telling a story of genuine momentum. The fourth is telling a very different story, and understanding the difference is the key to understanding whether this thesis holds.

Real Estate

Let’s start with Real Estate, because Real Estate is where BCG is doing something that deserves more attention than it has received.

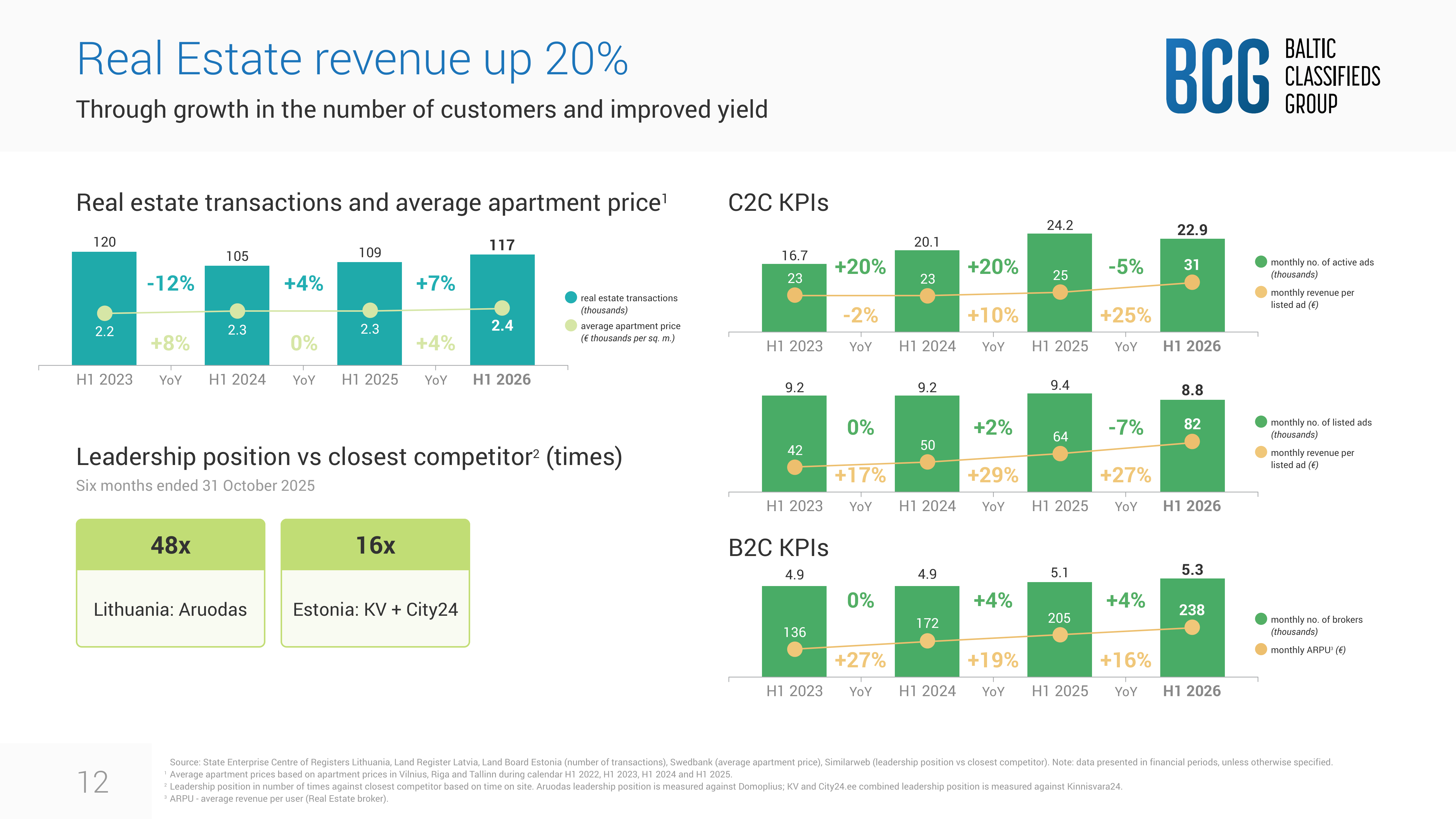

In the six months to October 2025, Real Estate revenue was €13.2m. That is up 20% from the year before. Twenty percent revenue growth from a business that already dominates its market. The interesting part is where that growth came from. It was not just price increases, though there were price increases.

The number of real estate brokers paying BCG a monthly subscription grew 4%. The monthly fee each broker pays (the ARPU) grew 16%. And on the consumer side, private sellers paying per listing saw their per-listing yield increase 27%.

Three levers pulling in the same direction at the same time. That does not happen by accident.

What is driving it is a combination of two things. The first is the Baltic real estate market itself, which is genuinely hot right now. Real estate transactions across Lithuania, Estonia, and Latvia grew 7% in the period. Average apartment prices in the three capital cities are up 4%.

When the underlying market is active, brokers are busier, developers are more willing to pay for visibility, and private sellers are more motivated to list at a premium tier because faster sales justify the cost. BCG benefits from a healthy market.

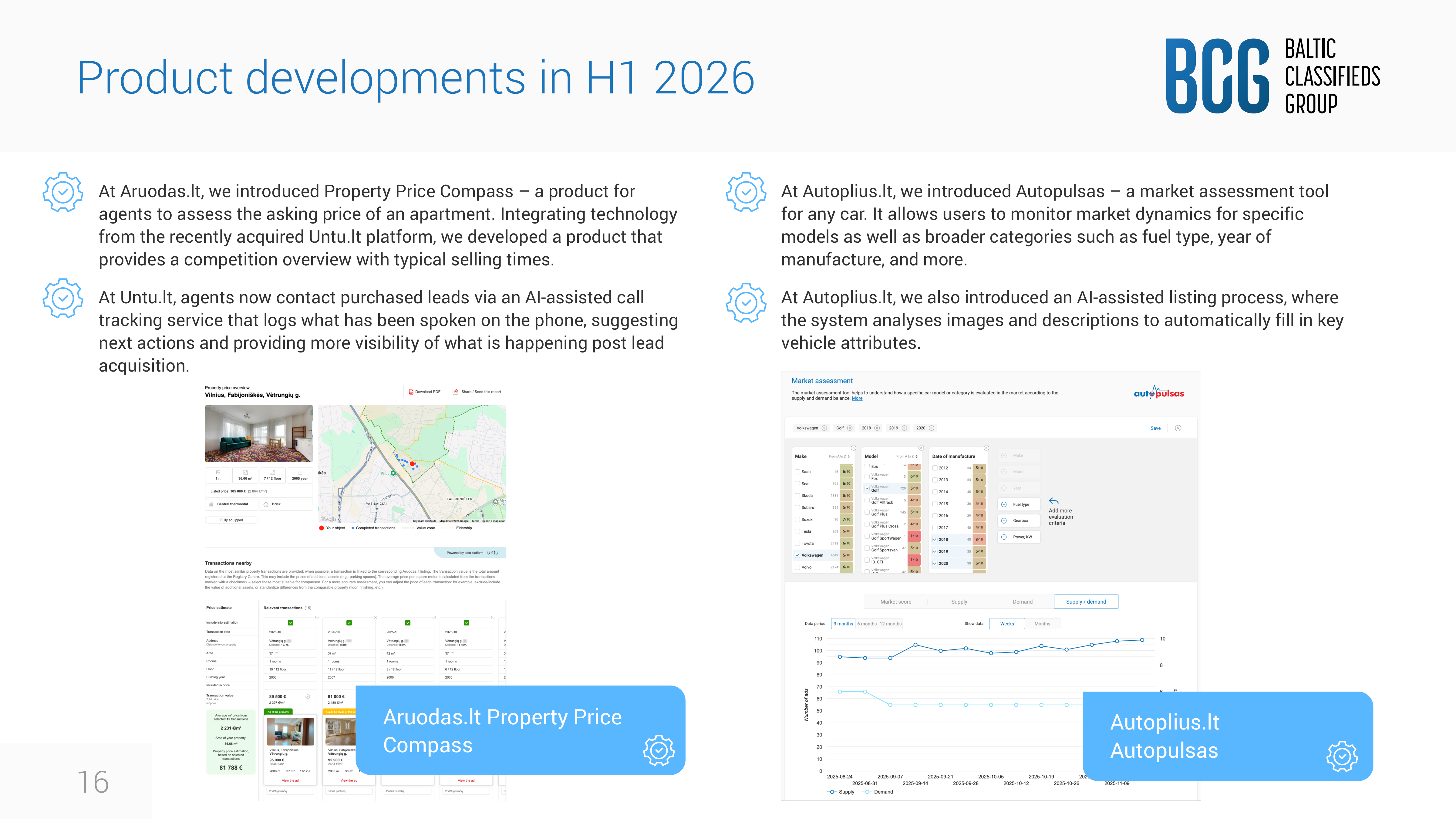

But the second driver is more interesting and more durable. BCG has been deepening the Real Estate product in ways that are changing the relationship between the platform and its professional users. Property Price Compass, the tool that integrates national land registry transaction data with listing history to produce a professional pricing report, was introduced at Aruodas.lt in Lithuania over the last two years.

It is now something broker clients expect. At Untu.lt, the recently acquired platform, agents are handling leads through an AI-assisted call tracking service that logs conversations, suggests follow-up actions, and gives brokers visibility into what happens after a lead is acquired.

These are not cosmetic features. They are workflow tools. And workflow tools create a completely different switching cost profile than listing services. A broker who uses Property Price Compass at every vendor meeting cannot easily switch to a competitor platform without losing the tool her clients have come to expect. BCG is not just the place where listings happen. It is becoming the software layer through which Baltic real estate professionals run their business.

The honest question to ask about Real Estate is whether this growth is repeatable.

The market tailwind (active transactions, rising prices) could cool. Interest rates in the Baltics have been falling, which has supported the market, but that tailwind is not permanent. And the ARPU expansion of 16% reflects pricing changes implemented in September and October 2024.

Those changes have now fully annualised. The next set of pricing changes was implemented in September and October 2025, and they have not yet fully fed through. So the near-term revenue picture for Real Estate looks strong. The medium-term picture depends on whether the Baltic real estate market stays active and whether BCG can continue deepening the product quickly enough to justify continued pricing power.

My read is that Real Estate is the segment carrying the thesis right now. It is growing at a rate that suggests the moat is widening rather than just holding.

Auto

Now Auto, which is the segment everyone has been focused on for the wrong reasons.

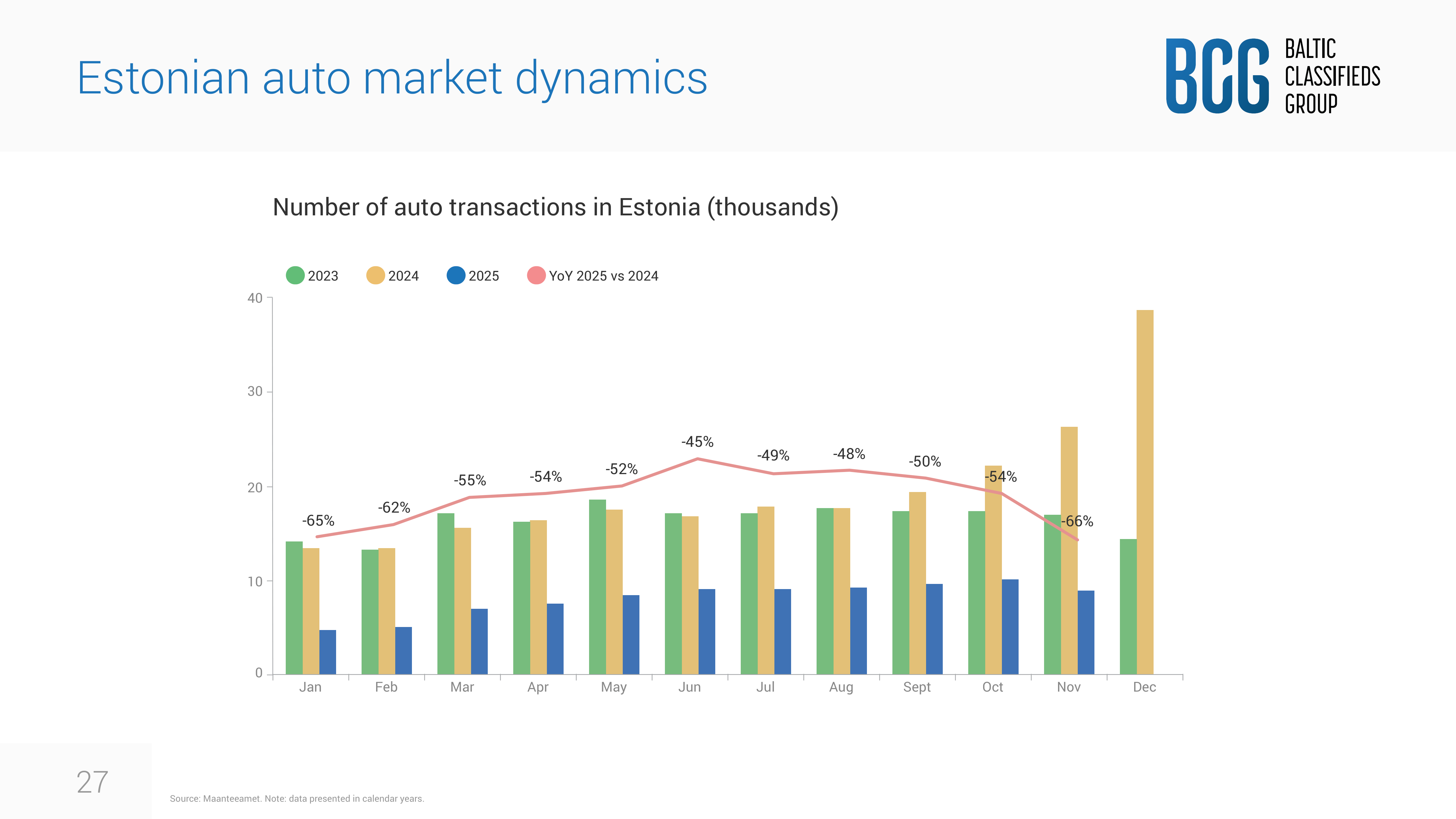

Auto produced €16.0m in revenue in the half. Exactly flat with the year before.

Not collapsing, not growing. Just flat.

The Brief explained why; the Estonian vehicle tax halved car transactions, listing volumes fell 29%, but dealer subscriptions held and per-listing prices rose enough to compensate.

What the Brief did not go into is what Auto actually looks like at the unit level, and the unit level picture is more interesting than the flat headline suggests.

On the B2C side (the professional dealer subscriptions) the number of dealers paying BCG fell by just 1% despite the Estonian market collapsing. One percent. In a country where car transactions were down between 45% and 66% every single month. Dealers stayed on the platform because where else were they going to advertise? And the monthly fee each dealer pays grew 13%. In Auto, in a terrible market, BCG still managed to raise prices and keep almost every dealer on the subscription.

On the C2C side (private sellers) the volume picture is ugly. Listed ads down 29%, active ads down 26%. That is the Estonian tax at work. But the per-listing yield grew 29%. The sellers who did list paid more. Again, because there is nowhere else to go.

Now here is the thing about Auto that makes me genuinely optimistic about H2. The terrible Estonian comparison base rolls off in January 2026. The tax was introduced in December 2024, so from January 2026 onwards you are comparing current Auto performance against already-collapsed prior-year numbers. The year-on-year percentage will flip from negative to positive almost mechanically. Management has confirmed this explicitly.

Lithuania, which is the larger Auto market for BCG, grew car transactions 8% in the same period. BCG’s Autoplusas platform in Lithuania leads the nearest competitor by 6 times on time spent on site. That market is healthy and BCG’s position in it is strong. Auto is not broken. One country implemented a severe tax that hurt one year’s results. The business underneath is intact.

Jobs and Services

Jobs and Services grew 7%, driven by a combination of more customers and better yields. The Jobs side, primarily CVbankas in Lithuania, grew both customer numbers and the monthly fee per customer. The unemployment rate in Lithuania ticked up slightly to 7.1%, which sounds like a headwind but actually reflects a growing labour force rather than a shrinking economy. Lithuanian wages grew 8.5% in the year. Companies are still hiring and still willing to pay for CVbankas’s recruitment tools, including the salary estimator that gives them a data advantage in setting competitive offers.

Services — the C2C classifieds for tradespeople and service providers — grew active ads 11%. More plumbers, cleaners, and builders are listing on BCG’s services portals. This is a steadily growing vertical that does not get much attention because it is modest in size but the trend is consistent.

Generalist

Generalist grew 4%, which looks unimpressive until you understand what it is.

Skelbiu.lt, BCG’s main generalist portal in Lithuania, is the sixth most visited website in the entire country. It competes partly with BCG’s own vertical platforms through cross-listing.

A private seller who lists a car on Skelbiu.lt may also get redirected to Autoplusas. The generalist portal is as much a traffic acquisition tool for the verticals as it is a standalone business. Growth of 4% driven by yield improvement, with active inventory holding steady, is the right outcome for this segment.

The synthesis is straightforward. Real Estate is carrying the thesis, growing at 20% with unit economics that suggest the moat is deepening. Auto is temporarily impaired by policy, structurally intact, and set to show positive year-on-year growth from January 2026 onwards. Jobs and Services is growing steadily with no signs of stress. Generalist is modest, useful, and not the point.

The people running this business

Munger’s question before any investment was always: do I trust the management? Not do I like them. Do I trust them.

BCG listed on the London Stock Exchange in July 2021. Justinas Šimkus has been CEO since before the IPO. Lina Mačienė is CFO.

They have been running this business together through the IPO, through the post-COVID normalisation, through the Estonian tax shock, and through a sustained period of annual price increases that have pushed ARPU and yields consistently higher across every segment.

The way to evaluate management is not to read their investor presentations. It is to compare what they said with what happened.

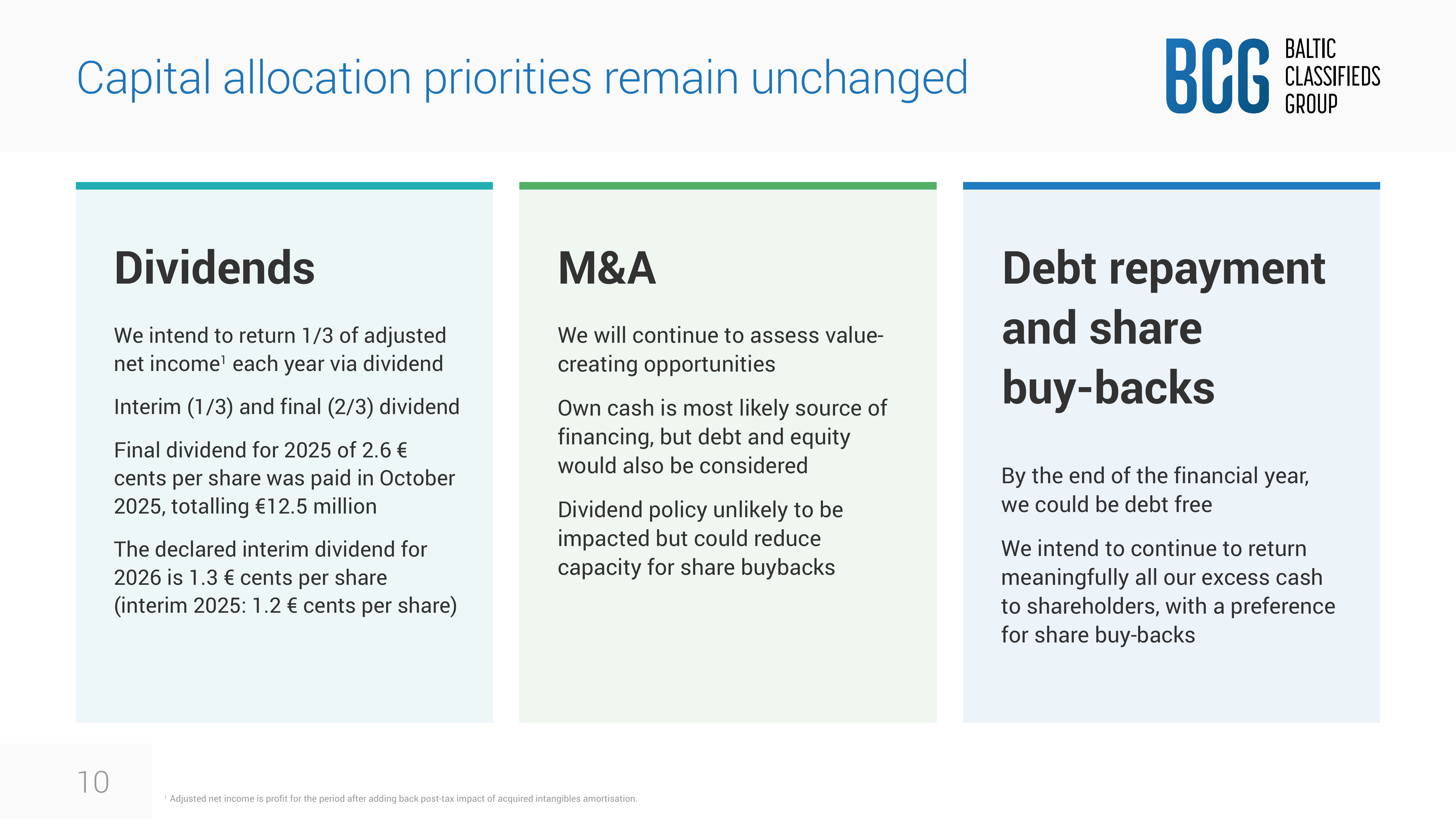

At the IPO, BCG’s stated capital allocation policy was to return one third of adjusted net income annually through dividends, with the preference for returning excess cash through share buybacks. Three and a half years later, that is exactly what they have done.

The dividend policy has been adhered to with mechanical consistency. Buybacks have continued through good periods and bad ones.

In the half-year to October 2025, with the Estonian situation creating uncertainty, they still bought back €6.4m of shares and paid a €12.5m dividend. They also voluntarily repaid €10m of debt, which was not required but was the right use of surplus cash.

The Estonian Auto situation is itself a management test. When the vehicle tax was introduced and it became clear that Estonian car transactions were going to collapse, there was a decision to be made about whether to adjust B2C pricing for Estonian car dealers.

BCG’s annual B2C pricing actions were implemented in September and October 2024 for most of its markets. For Estonian Auto dealers specifically, the pricing adjustments were postponed.

They made the right call.

Hitting Estonian dealers with a price increase at the same moment the tax was destroying their market would have been extractive and short-sighted. Instead they held pricing for that one market, kept almost all their dealer base, and positioned themselves for recovery when the comparisons normalise.

That is the Bloopers Test in action. A management team making obvious, decent decisions rather than clever ones.

The Bloopers Test

A Munger concept. The idea is simple: great businesses should not require brilliant management. They should require management that avoids doing stupid things.

When you apply it to a management team, you ask one question: are they making the obvious decent call, or are they trying to be clever? Clever is usually a warning sign. Obvious and decent, done consistently, is what you actually want.

The one area where I would want more information is on organic growth strategy beyond price increases.

BCG’s revenue growth has been driven primarily by yield expansion (charging existing users more) rather than by growing the user base materially. The number of real estate brokers grew 4% in the half. Auto dealers actually fell 1%. Jobs companies grew 1%. These are not large customer base expansions. The strategy is to extract more value from an already-dominant position rather than to expand the addressable market.

That is a legitimate and often excellent strategy. It is the strategy of a business that knows it has already won its market. But it does mean that the long-term growth trajectory is bounded by how far you can push yields before the customer pushes back. Management has not yet found that wall. Three consecutive years of pricing increases and no material customer loss suggests the wall is further away than bears assume. But it exists, and an honest assessment of management has to acknowledge it.

Overall: yes, I trust these people.

They have done what they said they would do, they have made sensible operational decisions under pressure, and they have not done anything that suggests they are optimising for personal benefit at the expense of shareholders.

The one acquisition

BCG has made one acquisition since listing: Untu.lt, a Lithuanian real estate technology platform, acquired in FY2025 for €1.0m.

One million euros. For context, BCG generates approximately €60m in operating cash annually. This was not a transformative deal. It was a targeted technology acquisition.

What Untu.lt brought was a set of AI-assisted real estate tools;

The property valuation technology that became Property Price Compass

The call tracking and lead management system now used by agents on the platform.

BCG acquired a technology capability that deepened their Real Estate moat rather than a revenue stream or a new market.

The price discipline is the notable thing.

€1.0m for a technology acquisition that is now embedded in the workflow of thousands of real estate brokers across the Baltics. That is not a trophy acquisition. That is a specific capability bought at a sensible price and integrated into the core product.

What it signals about BCG’s M&A appetite: they are not empire builders. They are not using their cash generation to buy adjacencies or to pay premium multiples for growth. The one acquisition they made was small, targeted, and directly additive to the moat they already have. That is the right behaviour for a dominant franchise in a small market.

Where the numbers came from; the history since listing

BCG listed in July 2021. Here is what has happened to the business since then:

When BCG listed, revenue for the financial year ending April 2021 was approximately €42m. This financial year, ending April 2026, the annualized run rate puts revenue somewhere around €87m. That is a doubling in five years, which implies a compound annual growth rate of roughly 16%.

The margin history tells an equally interesting story. In financial year 2021, the EBITDA margin was 76%. In 2022 it was closer to 47% , which was a significant step down driven by post-IPO operating cost increases and heavy amortization of acquired intangibles.

But that was a one-off. From 2023 onwards the margin has moved consistently upward: 75.6% in 2023, 76.9% in 2024, 78% in 2025. The business did not find efficiency after a period of inefficiency. It went through a brief post-IPO cost absorption period and then returned to its structural margin level, which has been improving gently ever since.

The capital return history is consistent with the stated policy. Dividends have been paid every year. Buybacks have been ongoing. The share count has been declining. A company that listed with approximately 489 million shares now has approximately 483 million in issue, and that number will continue to fall as buybacks continue.

The key question to ask about the historical picture is whether yield expansion is accelerating or slowing.

The data from H1 2026 suggests it is actually accelerating in some segments. Real Estate C2C per-listed-ad yield grew 27% in the half. Auto C2C per-listed-ad yield grew 29%. These are larger percentage increases than in prior periods.

That tells you one of two things:

either BCG has more pricing power than the market appreciates

or the base effects from low prior-year prices are temporarily flattering the percentages.

The truth is probably some of both. But the direction is right and the magnitude is not trivial.

Given everything that has happened since the IPO, is BCG better or worse than the prospectus implied? Better. Revenue has grown faster than the prospectus suggested. Margins have recovered to above the listing-period levels.

Capital returns have been disciplined and consistent. The Estonian shock is the first genuine operational headwind since listing, and the business absorbed it without a revenue decline. That is a better track record than most businesses produce in the same period.

Valuation

Start with what BCG actually earns for its owners, because reported profit and owner earnings are not the same thing for this business.

Net income for H1 2026 was €26.4m. That is the GAAP number. Three adjustments are needed to get to owner earnings.

First, add back the non-cash amortization of acquired intangibles — €3.7m in the half — because this is an accounting artefact of the 2020 acquisition of business client relationships, not a real economic cost. Those intangibles are now fully amortized, so this adjustment disappears going forward.

Second, subtract stock-based compensation of €0.5m. This is real dilution and must be treated as a cost regardless of how it is classified in the income statement.

Third, the maintenance capex is €0.4m against depreciation of €0.4m on non-acquired assets. These roughly cancel out.

The result: owner earnings of approximately €25.9m for the half, or €52m annualised.

Now the assumptions;

Revenue growth: Management has guided for H2 revenue growth above H1’s 7%, and double-digit growth for the full 2027 financial year. The B2C price increases implemented in September and October 2025 will fully annualise into H2 2026 revenue.

Estonian Auto comparables flip positive from January 2026. Real Estate is growing at 20% with a strong market backdrop. A 10% to 12% annualised revenue growth rate for the next three years is conservative relative to management guidance and recent trends.

Margin assumption: BCG has guided that EBITDA margins will remain in the mid-seventies even with investment in data and AI. The structural reason for this is simple: the cost base does not need to grow proportionally with revenue. More listings, higher yields, more broker customers — none of these require meaningful additional headcount or infrastructure. A 75% to 77% EBITDA margin assumption is conservative.

At 10% revenue growth and 76% margins, owner earnings grow from approximately €52m today to approximately €70m by year three. At 12% growth and 77% margins, the number is closer to €78m.

What multiple is warranted?

BCG operates in a market so small that it has essentially pre-empted competition. The moat is deepening through product development. The capital requirements are negligible.

The management team has a clean track record. For a business with these characteristics and this growth profile, a multiple of 22 to 25 times owner earnings is defensible.

At the lower end of the growth assumption and the lower end of the multiple range, the implied value is approximately €1.28bn. At the upper end of both, the implied value reaches €1.95bn.

The base case: €1.28bn, or approximately 220p per share.

The bear case: growth disappoints at 5%, margins compress to 74%, and the multiple contracts to 18 times. Implied value approximately €846m, or around 145p. The current price of 190p sits about 30% above the bear floor.

The bull case: growth runs at 14%, margins hold at 78%, and the multiple expands to 25 times as the debt-free capital return story gets priced in. Implied value approximately €1.95bn, or around 330p.

This is not a business trading at a severe discount to obvious value. It is a good business at a fair price, temporarily de-rated by a policy shock, with a specific catalyst — the Estonian comparison base — that is already reversing.

So, the case for owning it is not that it is obviously cheap. The case is that the de-rating was an overreaction to a temporary problem in a business that has now demonstrated it can absorb that problem without a revenue decline.

The distinction between what BCG earns on its own capital and what an investor earns at today’s price is worth dwelling on. BCG’s return on tangible capital is essentially infinite — the platform requires almost no tangible capital to operate.

But the investor buying at 190p and an enterprise value of approximately €1.05bn is paying for that extraordinary capital efficiency at a 4.9% owner earnings yield. The business earns extraordinary returns. The investor earns fair returns. These are different numbers, and conflating them is one of the most common errors in quality growth investing.

BCG is a wonderful business at a fair price. Not a fair business at a wonderful price.

The balance sheet

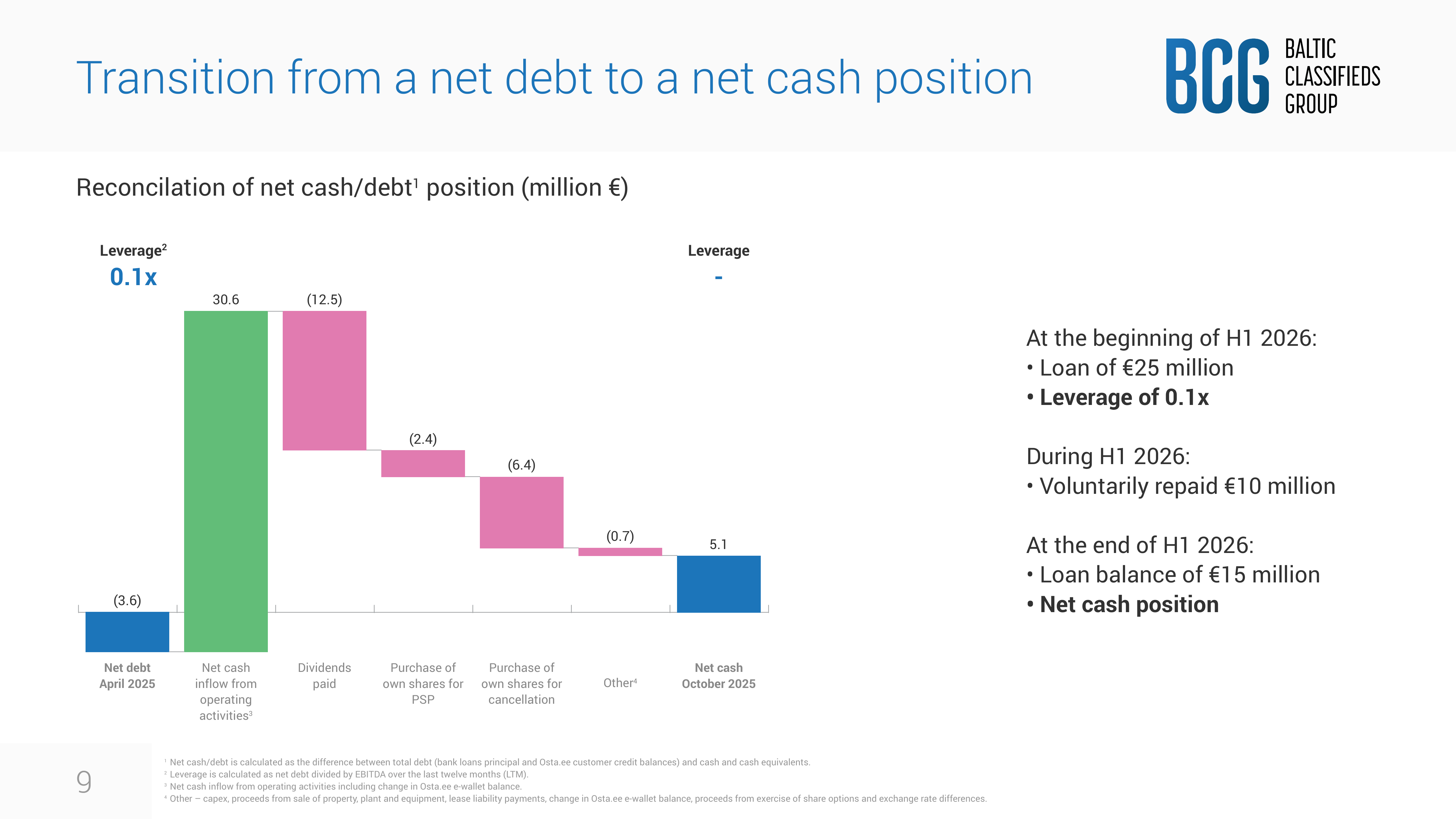

BCG ended October 2025 with net cash of €5.1m. Six months earlier it had net debt of €3.6m. The transition happened because BCG generated €30.6m in operating cash in the half, used €12.5m to pay the final dividend, bought back €6.4m of shares, and voluntarily repaid €10m of the bank loan.

The remaining loan balance is €15m, maturing in July 2026. This is trivial against the cash generation rate.

BCG generates the equivalent of the entire loan balance in operating cash every six months. Watch the refinancing terms when the facility matures, not because there is a solvency concern but because the interest rate will likely improve if they choose to maintain any debt capacity.

Management has said the company could be debt-free by the end of the current financial year; April 2026. When that happens, the full approximately €60m of annual operating cash flow becomes available for buybacks and dividends.

At the current market capitalisation of £880m, that is a total cash return yield of around 7%, growing at double digits. That is what the capital return conversation will look like in a few months.

The item on the balance sheet that looks alarming until you understand it is the goodwill. BCG’s balance sheet shows €330m of goodwill out of €386m of total assets. That is 85% of total assets in a single line item. For most businesses that would be a serious red flag.

For BCG it reflects the structure of how the business was assembled. Before the IPO, private equity assembled the portfolio of Baltic classifieds portals through a series of acquisitions. The goodwill represents the premium paid for those businesses above their book value. The assets underlying the goodwill are not tangible — they are the brand relationships, the audience, the network effects, the professional workflows. These are real assets.

They generate €60m of operating cash per year. They have never required impairment. BCG has not paid too much for businesses that subsequently disappointed. The goodwill is the price of buying dominant market positions and those positions have produced exactly what was paid for.

The risks

Let’s go through the risks, because there are things we need to be aware of with Baltic Classifieds.

The first is the free-listing attack.

If a platform with existing Baltic user trust (Facebook Marketplace for example) decided to offer free listings at scale across all three Baltic states, the consumer C2C side of BCG’s business would come under genuine pressure.

Private sellers deciding whether to pay €42 to list their car or €0 to list it on Facebook will choose free. The question is what percentage of BCG’s economics depends on private seller behaviour versus professional subscriber behaviour.

On the Auto segment, B2C dealer subscriptions represent the majority of revenue. Dealers will not stop paying for Autoplusas because Facebook offers free listings — they need the professional tools and they need the inventory depth that comes from a dominant platform.

On Real Estate, professional broker subscriptions and the workflow tools like Property Price Compass represent the core economics. A free-listing generalist platform does not threaten that. The vulnerable segment is generalist C2C, which is 15% of group revenue and where the competitive moat is weakest.

The early warning signal for this risk is BCG’s Auto and Real Estate C2C active ad volumes. If those numbers start declining for multiple consecutive quarters without a named policy explanation, it is the signal that inventory depth — the foundation of the flywheel — is eroding. Track those numbers every half-year.

The second mechanism is regulatory.

BCG raises prices every year on customers who have no practical alternative. That is the definition of a business that attracts antitrust scrutiny.

The Estonian Competition Authority has active enquiries open. BCG’s directors have assessed the likelihood of a material outflow from those enquiries as remote. I give that assessment weight because BCG’s market, while dominant, is also small. The harm from BCG raising annual prices on Lithuanian real estate brokers is genuinely minimal in the context of the national economy. The antitrust case is harder to make when the affected market is modest in size.

But the risk is real and observable. Any formal announcement from the Lithuanian or Estonian competition authorities opening an investigation specifically into BCG’s B2C pricing practices would change the valuation materially. The primary driver of BCG’s revenue growth is yield expansion. A cap on that expansion is a cap on the growth thesis.

And we can’t leave out macro/geopolitical risk.

I rarely include macro in my analysis, but in this case, we must address the elephant in the room.

Lithuania, Latvia, and Estonia sit at the eastern edge of NATO, sharing borders with Russia and Belarus. Estonia and Latvia border Russia directly.

Lithuania borders the Kaliningrad exclave and Belarus. These are not abstract geographic observations. The three Baltic states have lived under Soviet occupation within living memory, they understand the threat more clearly than most of their NATO allies, and they have responded to it seriously. All three now exceed NATO’s 2% of GDP defence spending commitment, with Estonia leading European allies at roughly 3.4%. NATO has substantially increased its forward presence in the region since 2022, with multinational battle groups deployed in each country.

None of this eliminates the risk. A significant escalation in the wider conflict or a direct threat to Baltic territory would affect consumer confidence, transaction volumes, and the attractiveness of Baltic equities to foreign investors in ways that BCG’s moat cannot insulate against. Small open economies with active property and labour markets are sensitive to geopolitical uncertainty in a way that larger, more diversified economies are not.

The Baltics have been pricing in proximity to Russia for thirty years. Their institutions are strong, their NATO integration is deep, and their populations have not needed recent events to remind them what is at stake. BCG’s business has compounded through every period of elevated tension since 1999. That does not make the risk theoretical. It means the risk is understood and priced locally in a way that external investors sometimes overreact to.

Of the risks in this piece, geopolitics is the one I think about least in terms of the day-to-day thesis and most in terms of position sizing. It is not a reason to avoid BCG. It is a reason not to make it the only thing you own.

The verdict

After going through all of this, here is where I land.

Going through the segment data, the management track record, the acquisition history, and the full financial picture has not weakened the case to me since writing the thesis brief. Real Estate is the strongest it has ever been. Auto is temporarily impaired in a way that is already reversing.

Management has done exactly what it said it would do since listing. The balance sheet is about to become debt-free. The capital return story is getting more interesting by the half-year.

What the Deep Dive added that the Brief could not cover: Real Estate is not just growing, it is growing in a way that suggests the moat is widening through product depth rather than just market share. Management has earned trust specifically by making the right call on Estonian Auto pricing during a difficult market. The valuation is fair but not compelling on a pure earnings yield basis. The case rests on the combination of quality, growth, and the specific catalyst of Estonian comps normalising.

If I had to name one thing that would most change my view, it would be evidence that the professional workflow integration is not as sticky as the product narrative suggests.

If broker churn on Aruodas.lt were rising, or if dealer retention on Autoplusas were declining, or if the ARPU growth started requiring unusual commercial concessions to maintain, any of those would suggest the moat is less embedded than it appears. None of those signals are present in the current data.

The verdict

After going through all of this, here is where I land, and it is not where I expected to when I started:

First, the business is excellent. The moat is real and deepening. Management has earned trust. The Estonian shock is temporary and the comparables will flip. None of that has changed in my mind after going through every corner of this company.

What has changed is my view on the price and what I am being paid to own it.

At 4.9% owner earnings yield, BCG is fairly priced for what it is.

Not cheap. The base case gets you to around 220p, which is roughly 15% from current levels.

That is a reasonable return for a dominant franchise in a small market. But reasonable is doing a lot of work in that sentence. Fifteen percent upside, with a 4.9% starting yield, is not the kind of asymmetry that makes me want to concentrate capital.

The bull case requires things to go better than guided. The bear case, where regulation caps pricing or a free-listing platform gets traction, does not look remote enough to dismiss.

And then there is the… map.

I laid out the geopolitical picture honestly in the section above. The Baltics have strong institutions, deep NATO integration, and thirty years of experience pricing in proximity to Russia. I believe all of that.

But when I combine a valuation that requires things to go right with a geography that carries tail risk I cannot model, I find myself looking for a better combination elsewhere.

And not because BCG is a bad investment. Because my opportunity cost is real and the risk-adjusted return here does not clear my bar.

I bought a small starter position in BCG earlier. I have since sold it. Not because the thesis broke (it did not) but because the price never gave me enough margin of safety to sit comfortably with the geography.

A wonderful business at a fair price is still a fair price. I want wonderful businesses at prices that make the geopolitical risk feel adequately compensated.

If BCG trades down toward 145p to 155p, the conversation changes entirely. At that level the owner earnings yield moves above 7%, the bear case is closer to priced in, and the same geopolitical risk starts to feel adequately compensated. That is the price where I would consider to own this properly rather than tentatively.

Until then: thesis intact, position closed, watching carefully.

Sources and references

Baltic Classifieds Group PLC — Half Year Results for the Six Months Ended 31 October 2025. Published 4 December 2025. Available at balticclassifieds.com.

Baltic Classifieds Group PLC — Half Year Results Presentation, Six Months Ended 31 October 2025. Published 4 December 2025.

Baltic Classifieds Group PLC — Annual Report and Accounts 2025. Financial year ended 30 April 2025.

Maanteeamet (Estonian Road Administration) — Monthly vehicle registration and transaction data, calendar year 2025.

Similarweb — Time on site data, leadership position vs nearest competitor. Referenced via BCG H1 2026 results presentation.

Google Analytics — Baltic site visit data, averaged based on Baltic population statistics. Referenced via BCG H1 2026 results presentation.

Skandinaviska Enskilda Banken (SEB) — Nordic Outlook Update, November 2025. GDP, inflation, unemployment, and wage growth forecasts for Baltic states.

Eurostat — Real GDP per capita CAGR, 2000–2024.

Swedbank — Average apartment prices in Vilnius, Riga, and Tallinn, calendar H1 2025.

State Enterprise Centre of Registers Lithuania, Land Register Latvia, Land Board Estonia — Real estate transaction volumes.

Euromonitor — E-commerce market growth, Lithuania and Estonia, 2019–2028.

Börsdata — Financial data export, Baltic Classifieds Group PLC, historical annual and quarterly figures.

Disclaimer

This Deep Dive is an educational breakdown of a public company based on information available in the materials provided (e.g., annual/quarterly reports, investor presentations, earnings transcripts) and my interpretation of that information. It is designed to be a “bolt-on” intelligence layer to your own due diligence — not a replacement for it.

Independence: I do not accept compensation of any kind from the companies discussed. My research is driven solely by my personal search for high-quality compounders.

Skin in the Game: Unless otherwise stated, assume the author may hold a long position in securities mentioned. Any position creates bias — treat this as commentary, not gospel.

Not Financial Advice: Nothing here is investment advice, a recommendation, or a solicitation. I am not a financial advisor. You are responsible for your own decisions. The stars rating is not a buy recommendation, but meant as a guide to understand the quality of the financial statement of the respective companies.

Error & Update Risk: Financial statements change, companies restate, guidance evolves, and I can be wrong. Verify key figures in the primary filings and consider reading the footnotes before deploying capital.