The Costco Trick: 6 Small Cap Companies That Could 10x by Giving the Money Back

A friendly tour of “Scale Economies Shared” — the most powerful flywheel in business — and the small, founder-run companies trying to ride it.

Dislcaimer: None of this is investment advice, every figure here is rough and from spring 2026 (markets move — check the latest before you act), and you should absolutely do your own homework before putting a single dollar, or peso to work. I’m a guy on the internet with opinions, not your financial adviser.

Okay, settle in. I want to tell you about my favorite kind of business, and then introduce you to six small, mostly-unknown companies trying to become it.

Here’s the weird part: the thing that makes these businesses great is that they refuse to get greedy.

Let me explain.

Pricing: The Atomic Moat

Premium members pay $199 per annum. With this membership, you will get access to all my curated watchlists and fat-pitch triggers, which will save you a lot of time and effort. You will also get access to my current portfolio, deep dives, and much more.

The flywheel that runs backwards

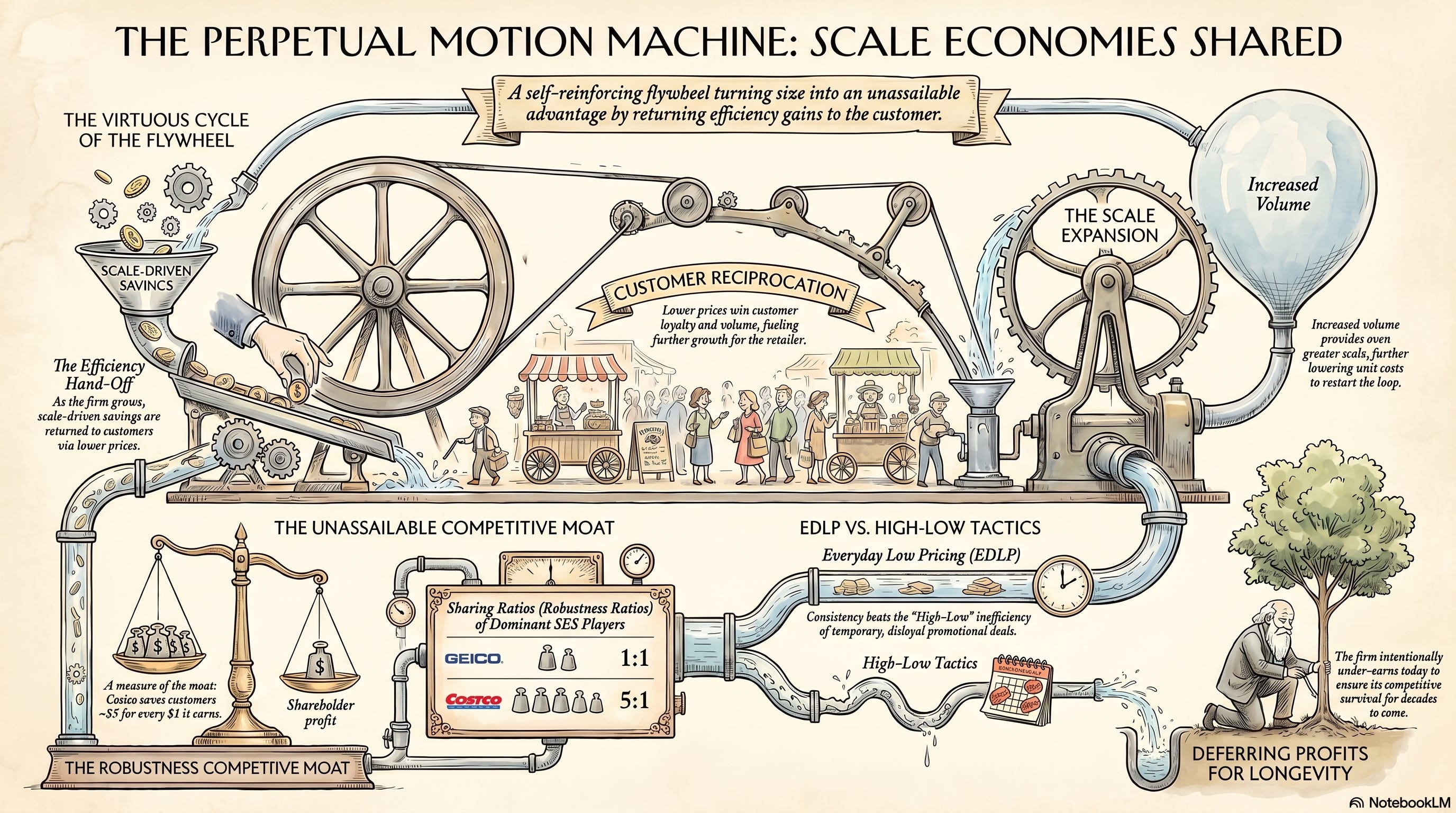

Most companies, when they get bigger, do the obvious thing. They use their new size to squeeze better deals out of suppliers, and then they keep the savings. Bigger scale, fatter margins, happier shareholders. Makes sense.

A rare breed does the opposite. They get bigger, their costs fall, and then they hand the savings straight back to the customer as lower prices. They deliberately stay thin on margin. On purpose. Forever.

Why would anyone do that? Because it sets off a loop:

Lower prices → customers buy more and tell their friends → you get bigger → your costs fall again → you cut prices again → and round and round it goes.

The investor Nick Sleep gave this loop a name: Scale Economies Shared.

His favorite examples were Costco and early Amazon; companies that treated every efficiency gain as something to give away rather than pocket.

Costco could jack up its prices tomorrow and mint a fortune this quarter. It doesn’t. It caps its markups by policy, makes most of its actual profit on membership fees, and uses its monstrous buying power to simply be the cheapest game in town.

The payoff is a customer base so loyal it’s almost spooky. And a moat that gets wider every single year, because every new member makes the whole machine a little bigger, a little cheaper, and a little harder to compete with.

That’s the magic.

Most moats erode over time, but this kind compounds.

The one test that separates the real thing from the fakes

Here’s how you tell a genuine Scale-Economies-Shared business from a pretender, and it’s almost embarrassingly simple:

Watch the margin line.

If a company is getting bigger and its profit margins are flat or even drifting down? That’s the tell.

It’s sharing the gains. (Costco’s gross margin has barely moved in decades. By design.)

If margins are climbing as it scales, then it’s pocketing the savings, not sharing them. That might be a perfectly lovely business, but it isn’t this one. Keep that test in your back pocket; we’ll use it at the end to bounce a couple of imposters off the list.

Why I hunt for the tiny ones

Costco is wonderful. Costco is also worth roughly a third of a trillion dollars. I think it is too much to expect that this is going to 10x from here very soon.

So I go looking for the small versions.

These are companies running this exact playbook but still valued in the hundreds of millions or low billions, in markets where the flywheel has barely started spinning. A $1.5 billion company that nails this can plausibly become a $15 billion one. A $300 billion one cannot make this move that easily.

Two more things I want before I’m interested:

A founder still at the wheel, ideally owning a big slug of the stock. Giving margin away is a decade-long act of discipline, and salaried managers cycling through on three-year bonus plans almost never have the stomach for it. Founders with their net worth riding on it do.

It is important to note that a price moat is not a lock-in moat. Nobody is stuck shopping at a discount store the way a company is stuck with the software it runs on, in comparison.

I have also written an article about switching costs that you can read here

The defense here is cheapness and trust, not switching costs. But this could make these businesses more fragile than they look.

With all that out of the way; here are six companies that follow the scale economies shared playbook and that could do a 10X from here, if they keep doing what they do:

1. BBB Foods — the one I’d start with

BBB Foods, which runs the Tiendas 3B hard-discount chain in Mexico, is the cleanest example on the list.

Picture a small, no-frills shop stocked with around 800 mostly own-brand products at rock-bottom, everyday-low prices. The scale crushes the cost of goods, and the savings go right back onto the price tag, which pulls in more shoppers, which builds more scale. Classic flywheel.

The runway is the exciting part: hard-discount is only about 3% of Mexican grocery spending, versus 24–38% in mature markets, so there’s a long way to grow into. Revenue has been compounding somewhere around 34% a year, and the founder still controls a big chunk of the votes.

The honest risks: it’s burning cash to open stores at speed, it leases every location (which flatters some of the headline numbers), Walmart’s Bodega and FEMSA’s Bara are competing hard, and the founder is in his sixties, so succession is a real question. But if you want to see the model in its purest, fastest-growing form, start here.

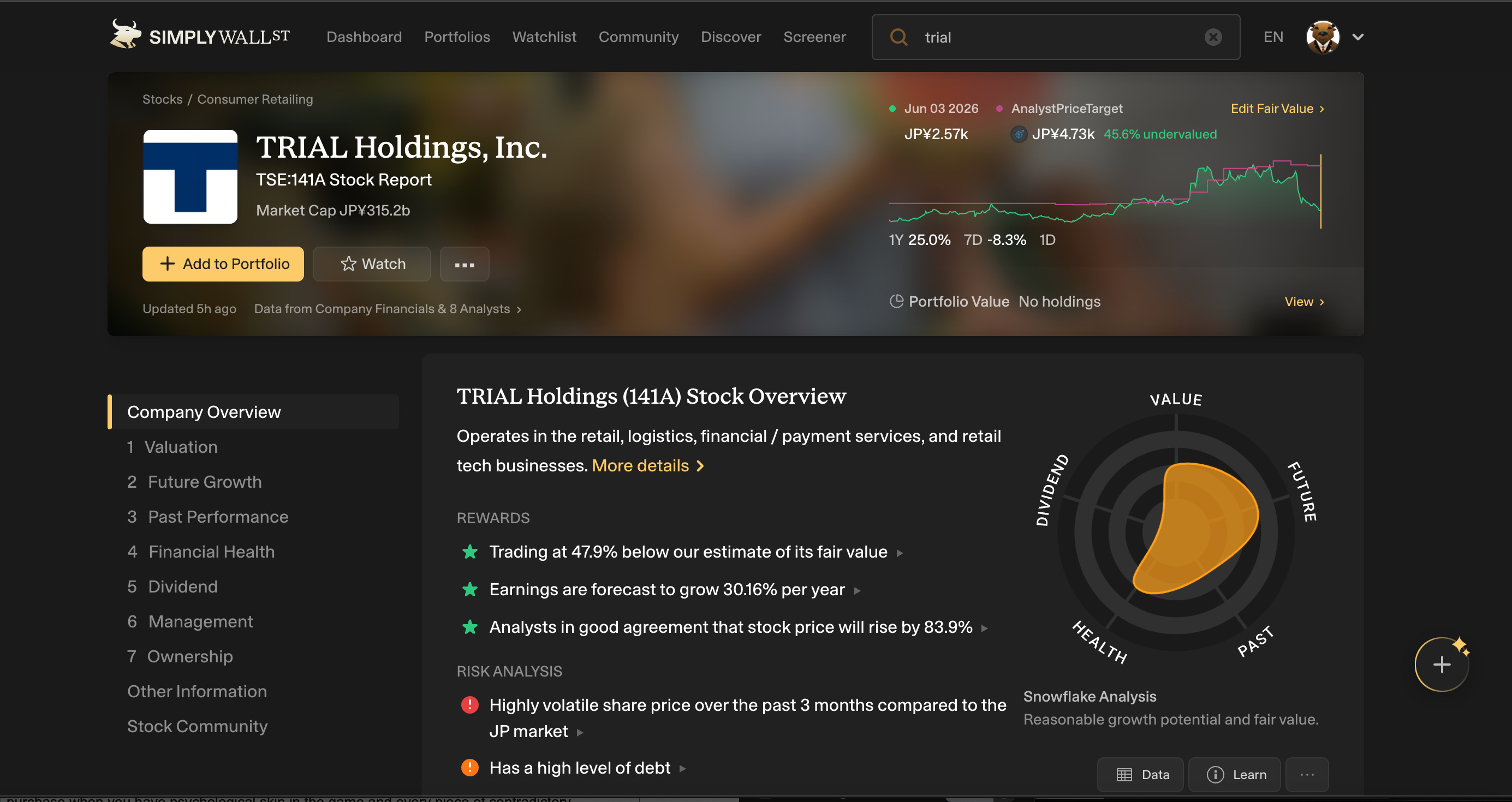

2. Trial Holdings — the clever one

Trial Holdings runs everyday-low-price discount supercenters in Japan, but with a twist that most discounters can only dream about: it bolts a “Retail-AI” layer on top — smart shopping carts, in-store digital advertising, and a river of shopper data.

That data-and-advertising income effectively subsidizes lower shelf prices, which gives the flywheel an extra turbo.

It’s the most technologically interesting business here, and the founder is still steering.

The company is listed in Japan, which makes it tricky for a lot of foreign investors to actually buy, and it’s busy digesting a very large supermarket acquisition (Seiyu). Big integrations are exactly where retailers tend to trip.

Now let’s move on to one of the most attractive on the list, one the numbers: