The Money Mind: Arnold Van Den Berg's Art of the Double Victory

How to conquer the two greatest enemies of the investor: The madness of the market, and the fear in your own mind.

If you look at the returns, Arnold Van Den Berg is a legend. Over a 38-year period, he averaged 14.2% annually, beating the market and most billionaires.

But if you look at his start in life, he should be dead.

Van Den Berg is not your typical Ivy League financier. He is a Holocaust survivor who ate plants to survive starvation in a Nazi-occupied orphanage. He barely graduated high school. He has no formal business degree.

Yet, he built a fortune and a world-class track record not by being the smartest man in the room, but by hacking the one thing most investors ignore: his own subconscious.

He didn’t just survive the Nazis; he survived the Madness of Crowds. This is how he did it.

The Origin Story: The Boy Who Ate Plants

In 1939, Arnold Van Den Berg was born in Amsterdam, on the same street as Anne Frank. When the Nazis invaded, his parents were walled up in a secret closet, and Arnold was smuggled into a Christian orphanage.

He spent his childhood in a state of terror and starvation. Conditions were so dire that, at age six, he was eating grass and plants in the fields just to stay alive. When his father finally retrieved him after the war, he was afraid to hug the boy for fear of breaking his protruding bones.

The family moved to East Los Angeles, but the trauma followed him. He was a skinny, weak Jewish kid in a rough neighborhood. He was “prey.”

Did You Know?

The Anne Frank Connection: Arnold lived at 823 Prinsengracht in Amsterdam. Just down the street, at number 267, lived Anne Frank. While Anne tragically did not survive, Arnold was smuggled out just in time.

The Rope Climber: Despite being malnourished as a child, Van Den Berg transformed himself into an elite athlete. He set a league record by climbing a 20-foot rope in 3.5 seconds—a feat that placed him 9th in the nation against college seniors.

The Catalyst: The First Punch

The defining moment of his life wasn’t a stock trade; it was a fistfight. A high school bully cornered him in the bicycle yard. Van Den Berg was terrified, convinced he would be destroyed.

The bully beat him. But as Van Den Berg washed the blood off his face later, he had an epiphany:

“My God! I’ve been so afraid of this, and this is not that bad... Just think if I would have fought back.”

He realized that the fear of the event is always greater than the event itself.

He learned to box. He learned to climb ropes. He realized that if he could reprogram his mind to ignore fear, he could do anything. He carried this realization into the stock market, where panic is the primary currency.

The Spark: The $3,000 Empire

Van Den Berg didn’t start on Wall Street with a trust fund. His father made him pay for his own food and clothes starting at age 13. He hustled his way through adolescence mowing lawns, pumping gas, and working on garbage trucks.

His first real “business” lesson came at 16, selling flowers on street corners. But his entry into finance was rocky. He worked as a door-to-door insurance salesman and then sold mutual funds.

The Ethical Breakpoint

He didn’t launch his own firm because of greed. He launched it because of disgust. While working at a financial services firm, he watched a colleague who was known to be dishonest get honored as “Man of the Month.”

Van Den Berg couldn’t stomach it. He quit immediately.

In September 1974, at 35 years old, he launched Century Management.

The Timing: He started in the middle of a brutal bear market.

The Capital: He had just $3,000 to his name (about $18,000 today).

The Goal: He didn’t want a yacht. He wanted to save $250,000 so he could be financially independent and “not take any shit off anybody”*.

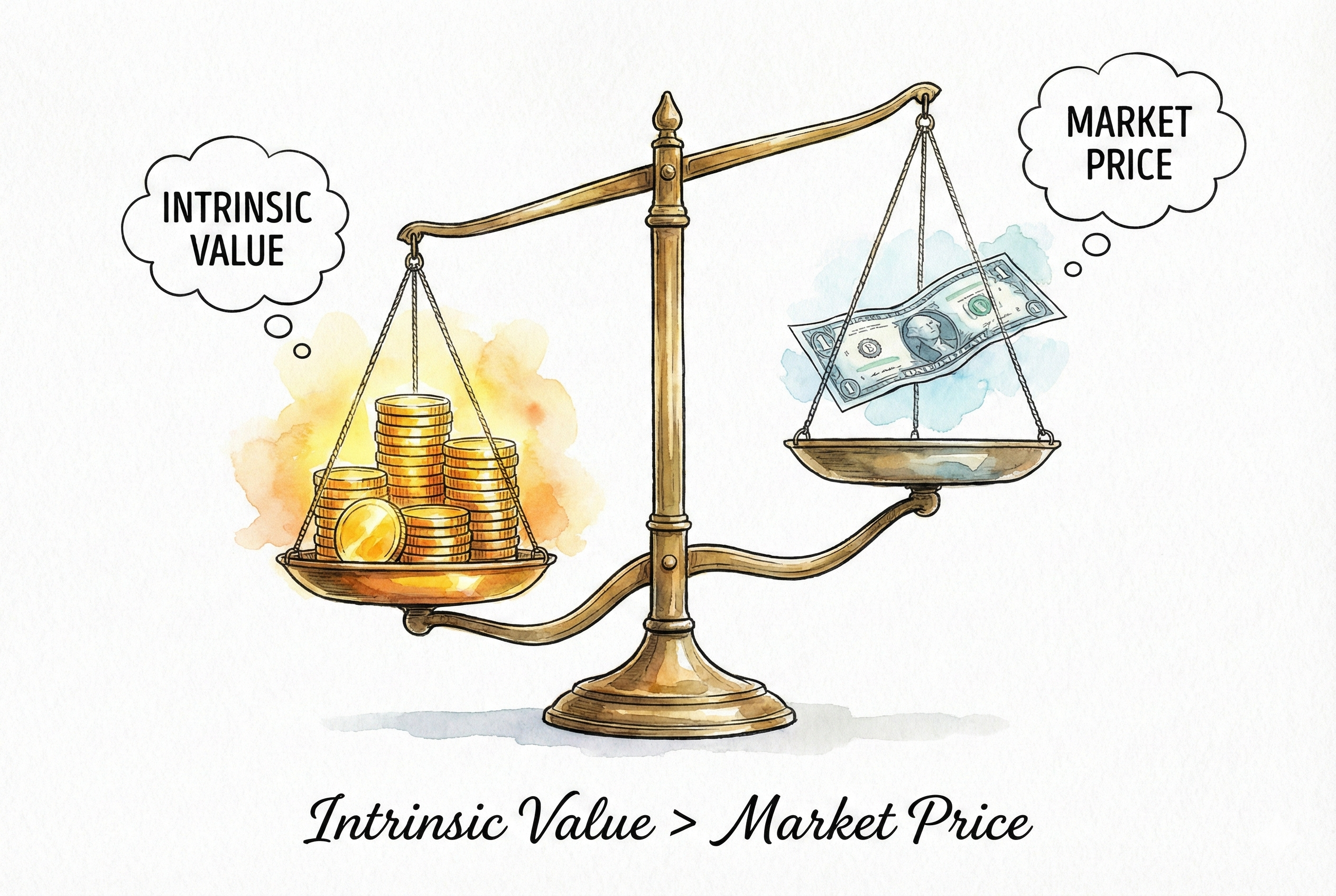

How Did He Do It? The “Private Market” Protocol

Van Den Berg’s investment philosophy is a direct extension of his survival instinct. His mother, who survived Auschwitz by trading goods, taught him a simple rule: Never pay retail.

He formalized this into a rigid mathematical system. While other investors looked at P/E ratios or growth charts, Van Den Berg built a proprietary system based on Private Market Value (PMV).

Here is the exact 3-step mechanic he used to turn $3,000 into an empire:

1. The “Private Buyer” Calculation

He ignores the stock price. Instead, he asks: “If I walked into this company today and bought the whole thing—every truck, building, and patent—what would I pay?”

He studies Mergers & Acquisitions (M&A) in that specific industry to see what real businessmen are paying for similar companies.

The Validation: In the 1974 crash, stocks were trading at 5x earnings. But Arnold saw that private companies were being bought out at 13.6x earnings. He knew the market was wrong by more than 50%. He bought, and the market eventually corrected.

2. The 5-to-1 Ratio

He doesn’t just want “upside.” He demands a mathematical edge.

The Rule: He looks for a 5-to-1 Reward-to-Risk ratio.

If a stock has $5 of potential upside and only $1 of potential downside, he buys. If the ratio drops to 2-to-1 or 3-to-1, he passes. He is looking for “bets” where the math is overwhelmingly in his favor.

3. The “Tangible Book” Guardrail

How does he know when to buy and sell? He uses Tangible Book Value (the value of the company’s hard assets minus liabilities and goodwill).

The Buy Zone: He buys when a stock is trading at 1.0x to 1.5x its Tangible Book Value.

The Sell Zone: He automatically sells when it hits 3.0x to 4.0x Tangible Book Value.

The PMV Rule: Generally, he buys at 50% of Private Market Value and sells at 80-100%

The Graveyard: The Loneliness of 1987

The “Graveyard” for Van Den Berg wasn’t a loss of capital; it was the risk of losing his career to maintain his discipline.

In 1987, the stock market was in a euphoria bubble. Prices were skyrocketing.

But Van Den Berg’s “50-Cent Dollar” system was flashing red. Stocks were no longer cheap. They were trading at or above his PMV estimates.

The Discipline: He didn’t bend the rules. He sold. He moved 50% of his clients’ money into cash.

The Pain: For months, the market kept going up. His clients were furious. They were missing out on the party. They called him an idiot. They threatened to fire him. He sat in his office, watching the market rise, repeating to himself:

“You’re doing the right thing... You may go out of business, but you’re doing the right thing.”

Then came Black Monday. The market crashed 22.6% in a single day.

While the rest of Wall Street was jumping out of windows, Van Den Berg was “like a kid in a candy store.” He had cash. He had discipline. He stepped into the wreckage and bought the best companies in America for pennies on the dollar.

Steal Their Brain: The Subconscious Algorithm

Van Den Berg admits he isn’t a genius. He barely passed high school. His edge is Subconscious Reprogramming. He treats his mind like software code.

Here is how you can install his operating system:

1. The “Hypnosis” Technique

Van Den Berg believes that your subconscious dictates your reality. If you believe you are weak, you will be poor.

The Action: He practiced self-hypnosis and affirmations daily. He would tell himself, “I am a loving person” or “I am a successful investor.”

The Rule: Don’t just read about investing. actively reprogram your belief system. If you panic during a downturn, it’s a software bug in your mind. Fix the code.

2. The “Private Buyer” Lens

Stop looking at stock charts. They are noise.

The Action: When you look at a stock, ask: “If I walked into this company’s headquarters today and offered to buy the keys to the building, the inventory, and the cash register, what would I pay?”

The Rule: If the stock market price isn’t 50% lower than that number, walk away.

3. The James Allen Method

Van Den Berg’s bible isn’t The Intelligent Investor; it is From Poverty to Power by James Allen (1901).

The Action: Take total responsibility for your mental state. Forgive everyone (Van Den Berg forgave the Nazis to release his own anger).

The Rule: “The soul that is impure... is gravitating toward misfortune.” Anger clouds judgment. To be a great investor, you must first clear your emotional debts.

Arnold’s 'Double Victory' isn't just about market returns—it is the psychological prerequisite for mastering The Art of Doing Nothing: Our Manifesto for 'Sit-On-Your-Ass' Investing.

The Human Factor: The Monk of Austin

Despite managing hundreds of millions of dollars, Van Den Berg lives like a monk.

The Car: For years, he drove a Nissan Maxima because it was “the best value.” When his wife forced him to upgrade to a Lexus, he was embarrassed to be seen in it.

The Diet: He is a vegetarian and a teetotaler (no alcohol). He practices yoga daily.

The Wealth: He claims to be “The Richest Guy in the World,” but not because of money.

In his office, tucked away in filing cabinets, is his true treasure: a collection of letters from people he has helped.

“I could lose all my money, and I could still go to these files and say... ‘Look at the people whose lives I’ve changed.’ That’s my bank account.”

The Verdict

Arnold Van Den Berg is the antidote to the “Wolf of Wall Street” culture. He proves that you don’t need to be aggressive, greedy, or morally bankrupt to win.

Copy this style if:

You are disciplined: You can hold cash for years while others get rich, waiting for your pitch.

You value sleep: You want a portfolio that doesn’t rely on hype or “greater fools.”

You believe in mindset: You are willing to work on your psychology as much as your spreadsheet.

Run away if:

You have FOMO: If you can’t stand seeing your neighbor make money on a trendy tech stock while you hold boring value stocks, this system will break you.

You need status: If you need a yacht to feel successful, you will hate the Van Den Berg lifestyle.

Van Den Berg teaches us that the market is a mirror of our own minds. If we are fearful, we sell at the bottom. If we are greedy, we buy at the top. The first investment you must make is not in a stock, but in yourself.

The 5-to-1 ratio is a fascinating constraint. I am curious about the specific methodology used to quantify that floor. Is it strictly tangible book value, or does he factor in the probability of permanent impairment?