The Quality Investor’s Glossary: 50 Terms Every Rational Investor Needs

Here are 50 terms you need to know as an investor.

Tip: Click the ❤️ heart or add this to your bookmarks to save this for your next research session.

I. The Architecture of Moats (Structural Advantage)

1. Economic Moat: A durable structural advantage that protects a company’s profits from competitors, allowing it to sustain high returns on capital over long periods.

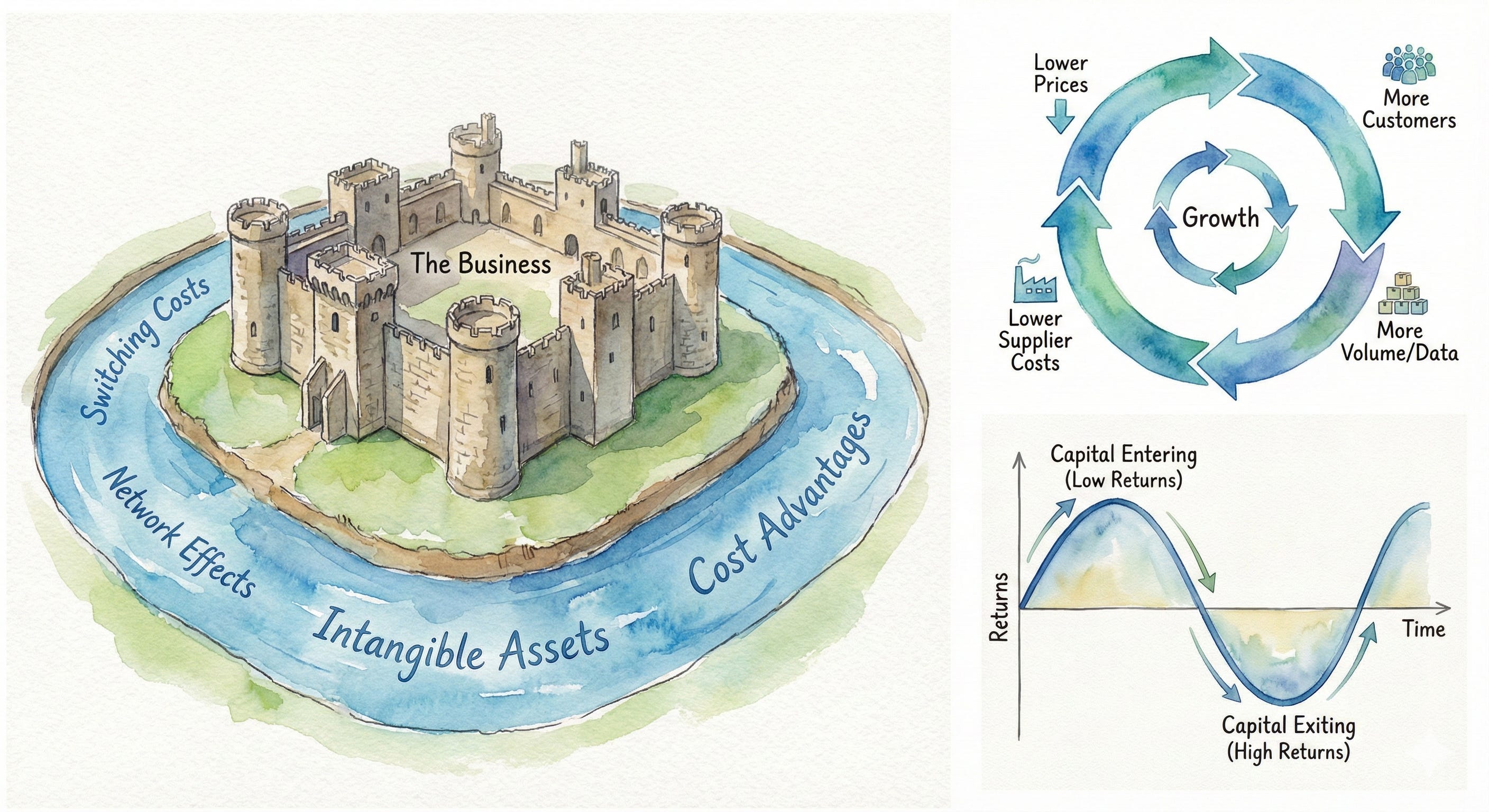

2. Scale Economics Shared (SES): A business model where a company (like Costco or Amazon) shares the benefits of its scale with customers through lower prices, widening its competitive moat daily.

3. Network Effects: A dynamic where a service becomes more valuable as more people use it. (e.g., Meta, Visa, Duolingo).

4. Switching Costs: The pain—financial, procedural, or psychological—a customer experiences when changing providers. The “stickiest” moat (e.g., Adobe, Salesforce).

Also read: Pain & Profit: Why Switching Costs are the King of Moats

5. Intangible Assets: Non-physical barriers to entry such as patents, government licenses, or brand loyalty that legally or psychologically block competition.

Also read: The Money Mind: Dr. Herbie Wertheim

6. Low-Cost Producer: A company that can produce goods or services at a lower cost than anyone else, often due to scale, geography, or unique process efficiency.

7. Counter-Positioning: A strategy where a newcomer adopts a business model that incumbents cannot copy without destroying their existing business (e.g., Netflix vs. Blockbuster).

8. Pricing Power: The ability to raise prices without losing customers. Warren Buffett calls this the single most important decision in evaluating a business.

9. The Flywheel Effect: A self-reinforcing loop where each part of the business accelerates the others. (e.g., MercadoLibre’s logistics feeding its fintech, which feeds its e-commerce).

Also read: Deep Dive: MercadoLibre ($MELI)

10. Toll Bridge: A company with a monopoly on a specific niche where you must pay them to cross. (e.g., Verisign, Moody’s, or dLocal in emerging markets).

Also read: The Titan Test: Would Dev Kantesaria Buy dLocal ($DLO)?

II. The Financial Scout (FINS Metrics)

11. ROIC (Return on Invested Capital): The “God Metric.” It measures how effective a company is at turning capital into profit. Calculation: (NOPAT / Invested Capital).

Also read: Deep Dive: Evolution AB

12. Free Cash Flow (FCF): The cash left over after a company pays for its operating expenses and capital expenditures. This is the “real” owner’s profit.

13. Operating Leverage: When revenue grows faster than costs. A company with high operating leverage adds profit directly to the bottom line as it scales.

14. Gross Margin: The percentage of revenue retained after direct costs of goods sold. High gross margins often indicate a premium product or pricing power.

15. Negative Working Capital: A situation where a company gets paid by customers before it has to pay suppliers. This acts as an interest-free loan from the market.

16. Cash Conversion Cycle: The number of days it takes to convert inventory into cash. A negative cycle (like Amazon’s) is a powerful compounding engine.

17. Owner Earnings: Net Income + Depreciation/Amortization - Maintenance CapEx. The figure Warren Buffett uses to determine true valuation.

18. Maintenance CapEx: The money a company must spend just to keep the lights on and maintain its current competitive position.

19. Growth CapEx: Money spent to expand the business. Rational investors distinguish between “maintenance” (bad) and “growth” (good) spending.

20. Rule of 40: A SaaS metric stating that a software company’s Growth Rate + Profit Margin should exceed 40%.

III. Capital Allocation (The CEO’s Job)

21. Capital Allocation: The process of deciding how to deploy a company’s resources: Reinvestment, M&A, Dividends, Buybacks, or Debt Repayment.

22. The Outsider CEO: A leader who ignores peer pressure and conventional wisdom, focusing solely on per-share value creation (e.g., Henry Singleton, William Thorndike).

23. Share Cannibal: A company that aggressively buys back its own stock, reducing the share count and increasing the remaining shareholders’ ownership stake.

24. Return on Incremental Invested Capital (ROIIC): The return a company earns on the new dollar it invests today. This predicts future growth better than historical ROIC.

25. Skin in the Game: When management holds a significant amount of their own personal wealth in the company stock.

Also read: Simple Truth: Evolution AB ($EVO)

26. The Conglomerate Discount: The market’s tendency to undervalue complex multi-business companies. Smart capital allocators (like Fairfax Financial) exploit this.

27. Float: Money held by an insurance company (from premiums) that can be invested for profit before claims are paid. Free leverage.

Also read: The Money Mind: Shelby Cullom Davis

28. Dividend Aristocrat: A company that has consistently increased its dividend for 25+ years. Often a sign of stability, but sometimes a sign of low growth.

29. Value Trap: A stock that looks cheap by traditional metrics (low P/E) but is cheap because the business is structurally dying.

30. Accretive vs. Dilutive: Whether a financial action (like an acquisition or buyback) increases (accretive) or decreases (dilutive) Earnings Per Share.

IV. Market Philosophy & Psychology

31. Margin of Safety: Buying a stock at a significant discount to its intrinsic value to protect against errors in judgment or bad luck.

32. Mr. Market: Ben Graham’s allegory for the stock market—a manic-depressive partner who offers you prices every day. You are free to ignore him.

33. Circle of Competence: The specific area where an investor has an edge. Staying inside this circle is key to avoiding disaster.

34. The Ick Factor: High-quality businesses that are ignored because they are boring, ugly, or controversial (e.g., waste management, debt collection, funeral services).

Also read: Rumbu Holdings: The Ick Factor Compounder

35. Time Arbitrage: The edge gained by having a longer time horizon than the average market participant (who focuses on quarterly results).

36. Coffee Can Portfolio: The strategy of buying high-quality stocks and never selling them, letting them sit for decades like valuable papers in a coffee can.

37. Second-Level Thinking: Howard Marks’ concept of thinking deeper than the consensus. (Level 1: “Outlook is bad, sell.” Level 2: “Outlook is bad, but less bad than priced in, buy.”)

Also read: The Art of Going Against The Crowd

38. The Red Queen Effect: Running fast just to stay in the same place. Describes businesses with no moat that must constantly reinvest just to survive.

39. Lollapalooza Effect: Charlie Munger’s term for when multiple biases or factors act together to drive an extreme outcome.

40. Sit-On-Your-Ass Investing: The discipline of inactivity. Recognizing that the big money is made in the waiting, not the trading.

Also read: The Art of Doing Nothing

V. The Atomic Framework (Advanced Concepts)

41. The Davis Double: The powerful compounding effect of Earnings Growth + P/E Multiple Expansion happening simultaneously.

42. Capital Cycle Theory: A framework by Marathon Asset Management. It posits that high returns attract capital (competition), lowering returns, while capital flight leads to future opportunity.

Also read: Why You Need To Know About The Capital Cycle Theory

43. The Sleep Index: Our collection of companies that share scale economies to dominate their industries (inspired by Nick Sleep).

44. The Lynch Index: Our collection of “Fast Growers” and “Stalwarts” that fit Peter Lynch’s 10-bagger criteria.

45. The Nomad Index: Our collection of companies run by “Outsider” capital allocators (inspired by the Nomad Partnership letters).

46. Spawner: A company with the DNA to constantly launch new, unrelated business lines from within (e.g., Sea Ltd spawning Shopee from Garena).

47. Hidden Champion: A small, obscure market leader (often in B2B) that dominates a niche global market.

Also read: FINS Analysis: Norbit ASA

48. Unit Economics: The direct revenues and costs associated with a single unit of business (e.g., one user, one subscriber). If this doesn’t work, scale won’t fix it.

49. Total Addressable Market (TAM): The total revenue opportunity available for a product or service. A “limitless” TAM is key for multibaggers.

50. The Atomic Moat: A competitive advantage so deep and structural that it can survive bad management, macro downturns, and technological shifts.

Also read: START HERE: The Atomic Moat Ecosystem